Solutions

Law firms

Tax, audit & accounting firms

Success stories

-

A true competitive advantage

Law firm Zarwin Baum’s embrace of generative AI as the natural next step in the evolution of legal work and their adoption of CoCounsel Legal has helped them achieve remarkable efficiency gains and improved client relationships.

-

Workflow transformation drives impact

Brinks, a global leader in secure logistics and security solutions, used CoCounsel to reimagine what was possible with AI tools, turning legal challenges into a competitive advantage.

-

The forefront of audit tech

A better auditing workflow solution was the answer to multiple challenges faced by The Mercadien Group. Find out how they achieved greater efficiency by embracing Cloud Audit Suite.

Products

Legal

Trade & supply

Tax, audit & accounting

- 1040SCAN

- Audit Intelligence Analyze

- CoCounsel Audit

- CoCounsel Tax

- Ready to Advise

- Ready to Review

- View all

Corporate tax

Recommended products

-

CoCounsel Legal

Transform your work with the only AI legal solution uniting research, drafting, and document analysis in a single experience. Designed by legal experts and built on trusted content and advanced AI, CoCounsel Legal accelerates multistep work so you can better serve your clients and grow your business.

-

CoCounsel Tax

Transform your tax practice with CoCounsel Tax, an AI-powered assistant that combines trustworthy answers, automation, and firm knowledge into one seamless platform. Enhance efficiency, reduce risk, and improve client confidence with CoCounsel Tax.

-

CLEAR

Powerful software designed for law enforcement, compliance, risk, and fraud investigators. Conduct thorough investigations with ease using our intuitive online investigation software. Efficiently, prevent, detect, and solve crime.

Purchase

Buy solutions

Resources

Insights

Events

Product training

Product communities

Developers

Highlights

-

2026 SKILLS showcase

Join weekly sessions to experience in-depth demonstrations of the leading legal AI products while connecting with strategic law firm leaders in knowledge management, innovation, and AI.

-

Ghosts on the ledger

Payroll fraud is a major compliance risk. Learn how payroll analytics and AI-powered tools can help exorcise phantom employees and employers.

-

Future of professionals report 2025

The Thomson Reuters Future of Professionals Report 2025 reveals how AI continues to shape professional work — and what it takes to get ahead. This year’s report shows that increased efficiency, productivity, and cost savings top the list of benefits professionals attribute to AI, making it indispensable for organizations facing rapid change.

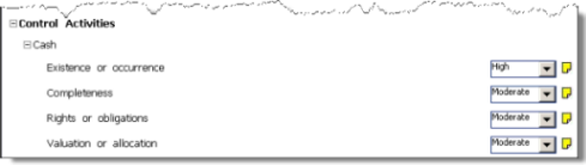

Assess Control Risk

Public Company Audit of Internal Control