Rent and Royalty Transactions

When a foreign divisional consolidation's

Intercompany Data Entry and Processing Level

is set to Division, intercompany payments and receipts are recorded in the member (division) binders rather than the foreign divisional consolidation binder.- The apportionment of the intercompany rent/royalty expense accounts in the payor divisions is used to determine the reallocation of the income at the recipient level.

- The intercompany rent/royalty income in the recipient divisions is reallocated to match the way the related expense is spread at the payor level.

- Any expenses in division recipients that use base codes 055, 056, 060, 065, 070 and 071 will be reapportioned using the results within that division binder.

- If an expense is apportioned on base codes 155, 156, 160, 165, 170 or 171, it will be spread using ratios determined at the divisional consolidation level.

Example:

CFC1 is a Controlled Foreign Corporation.

Entity Name | Type | Binder Properties Selection | Indicator |

|---|---|---|---|

DCA | Foreign Divisional Consolidation | International Data Completion Level | Division |

DCA | Foreign Divisional Consolidation | Intercompany Data Entry and Processing Level | Division |

Div 1 | Foreign Division | Intercompany Data Entry and Processing Level | member of DCA |

Div 2 | Foreign Division | Intercompany Data Entry and Processing Level | member of DCA |

Entity Name | Type | Binder Properties Selection | Indicator |

|---|---|---|---|

DCB | Foreign Divisional Consolidation | International Data Completion Level | Division |

DCB | Foreign Divisional Consolidation | Intercompany Data Entry and Processing Level | Division |

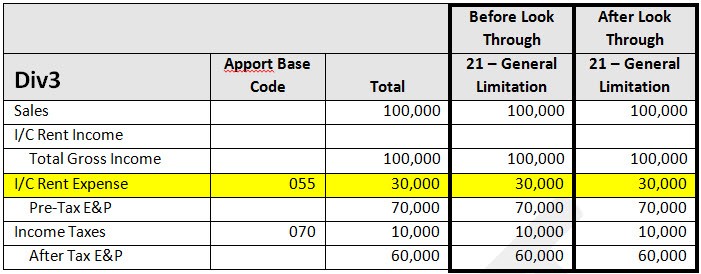

Div 3 | Foreign Division | Intercompany Data Entry and Processing Level | member of DCB |

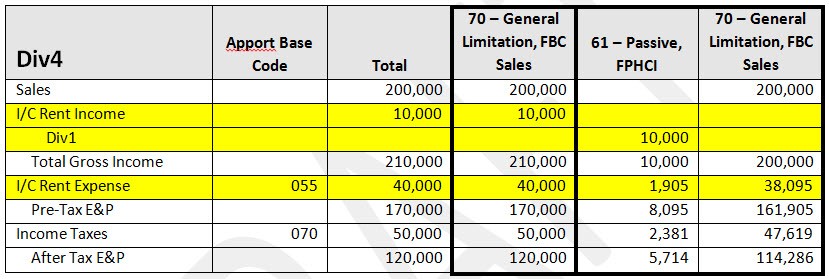

Div 4 | Foreign Division | Intercompany Data Entry and Processing Level | member of DCB |

CFC1, DCA and DCB have the same functional currency. Since ONESOURCE Income Tax International requires functional currency within the members of a division consolidation, Div1, Div2, Div3 and Div4 have the same functional currency.

The following intercompany rent transactions are recorded:

Payor | Recipient | FPHCI | Payor Amount | Recipient Amount |

|---|---|---|---|---|

Div1 | Div4 | 1 | 10,000 | 10,000 |

Div3 | CFC1 | 0 | 30,000 | 30,000 |

Div4 | CFC1 | 1 | 40,000 | 40,000 |

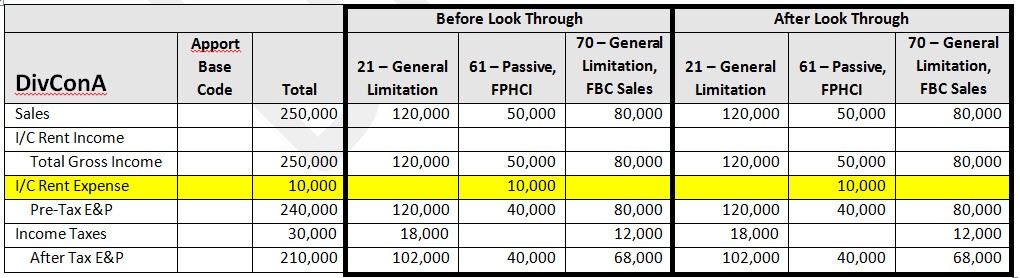

Divisional Consolidation A - Allocation and Apportionment

The results of look through calculations in the divisions are summarized to arrive at the divisional consolidation amounts.

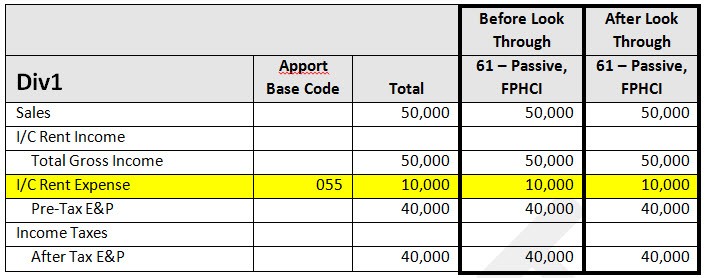

Division 1

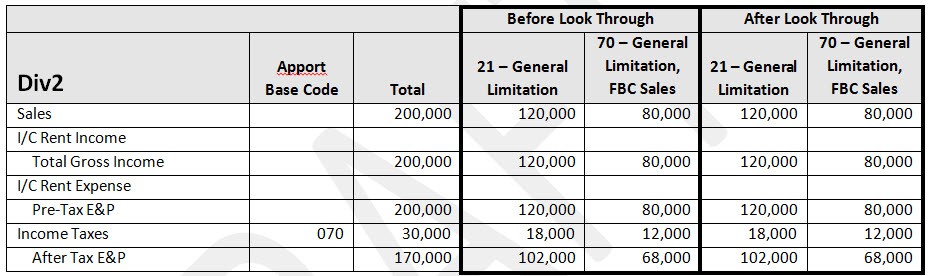

Division 2

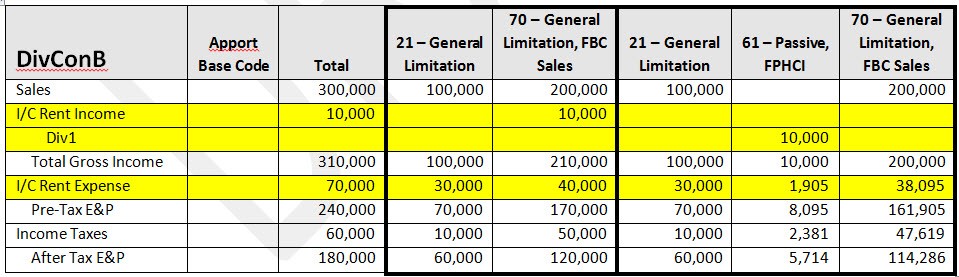

Divisional Consolidation B - Allocation and Apportionment

The results of look through calculations in the divisions are summarized to arrive at the divisional consolidation amounts.

Division 3

Division 4

Div4 is a member of a foreign divisional consolidation with an Intercompany Data Entry and Processing Level of Division and receives intercompany rent from Div1 (also a member of a divisional consolidation with an Intercompany Data Entry and Processing Level of Division). Div4's intercompany income is reallocated to match the apportionment of Div1's I/C rental expense.

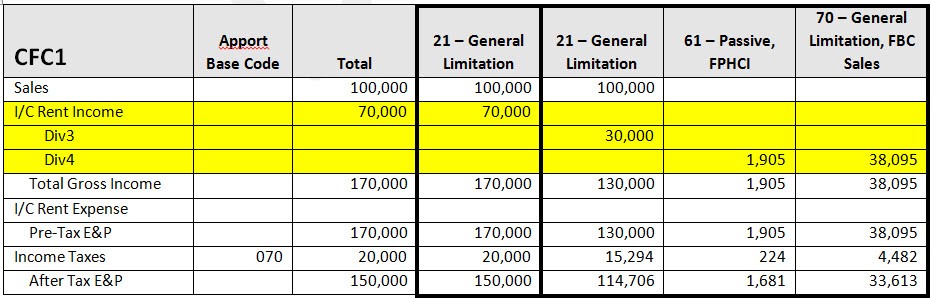

CFC 1 - Allocation and Apportionment

CFC1 receives intercompany rent from Div3 and Div4 (members of a divisional consolidation with an Intercompany Data Entry and Processing Level of Division). The portion of CFC1's intercompany income received from Div3 (30,000) is reallocated to source code 21 to match the apportionment of Div3's I/C rental expense. The portion of CFC1's intercompany rent received from Div4 (40,000) is reallocated to follow Div4's I/C rental expense and is spread between source codes 61 and 70.