Subpart F Calculations and Section 960(C) Reductions of Deemed Paid Taxes For Tax Years 2011 and Later

The

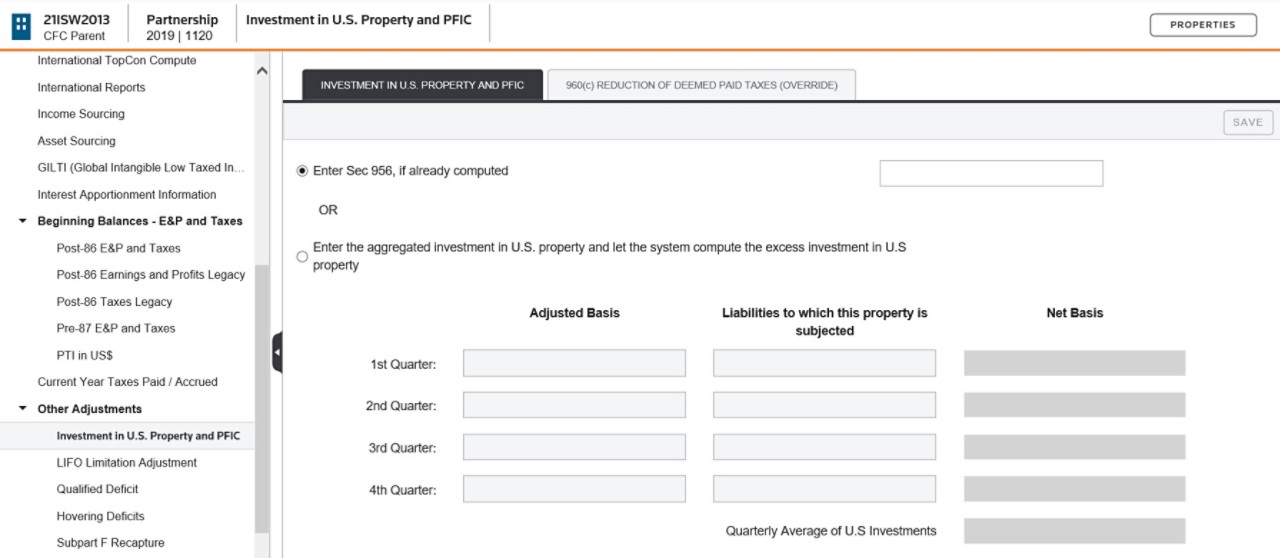

Section 960(c) Reduction of Deemed Paid Taxes (Override)

tab is available in a foreign entity's Investment in U.S. Property and PFIC

screen for tax years 2011 and later to record any decrease to deemed paid credits on Section 956 (Investment in US Property) inclusions.During the International Transfer process of a TAS Compute:

- The tax credits on the Deemed Paid Credit Report, transferred to Form 1118 Schedules C, D, and E, and transferred to the Deemed Paid Taxes column of theForeign Income Taxes > Deemed Paid Taxesscreen are unaffected by any 960(c) reduction input.

- The 960(c) reduction entered on the Investment in U.S. Property and PFIC screen are transferred to the 960(c) Reduction of Taxes column of theForeign Income Taxes > Adjustmentsscreen.

- The deemed paid credit net of 960(c) reduction is depleted from the foreign entity's Post-86 Tax Pool and reflected in the Gross-up on IUSP on the Foreign Income Inclusion Report and related amounts transferred to the tax adjustments of the U.S. owners.

Subpart F Data Entry

A

Section 960(c) Reduction of Deemed Paid Taxes (Override)

tab is available in a foreign entity's Investment in U.S. Property and PFIC

screen to record decreases to deemed paid credits on Section 956 (Investment in US Property) inclusions for Subpart F computes for tax years 2011 and later.

This override screen is available in income tax binders with an International Filing Type of

Foreign Entity

and an entity type of Parent, Subsidiary, Corporate Single Entity, or Divisional Consolidation. You can choose by foreign entity to override and reduce the Section 956 deemed paid credit calculated by ONESOURCE Income Tax.- Section 960(c) Deemed Paid Taxes (DPT) Reduction amounts entered at the Foreign Entity level will be used to automatically update the foreign entity's tax pools and related reports during Subpart F computes. TheSection 960(c) DPT Reduction transfers to the Adjustmentstab in theFTC owner's Foreign Income Taxscreen during the International Transfer process of TAS Compute in the FTC Entity.

- If you select theUse Override Valuesbox at the top of theSection 960(c) Reduction of Deemed Paid Taxes (Override)tab, the amounts you enter in the Amounts in U.S. Dollars column will be used during Subpart F computes for that foreign entity. If you do not check the box, the system ignores any amounts entered in the960(c) Overridesscreen.

- The override screen displays each FTC Basket (user and system defined) in that tax year'sSource Code Definitionscreen. We recommend that you enter any reduction to the system calculated deemed paid credit on Section 956 inclusions as a positive amount in the Amount in U.S. Dollars column. (Zero amounts will not be displayed.)

- During calculations, if you have selected theUse Override Valuescheckbox, blank data entry fields will be treated as a zero reduction to the allowable DPT.

Subpart F Compute

Amounts entered in the

Section 960(c) Reduction of Deemed Paid Taxes (Override)

tab are automatically limited during Subart F computes to the lesser of the amount entered in the Amount in U.S. Dollars column for an FTC basket or the Tax Deemed Paid by SH (US$) amount for that basket on Subpart F - Deemed Paid Tax Report.Important: Amounts in any Pre-87 Tax Layer are currently excluded from the Section 960(c) reduction calculation.

The Section 956 (Investment in U.S. Property) inclusion on the E&P Pools Report and the tax credit by U.S. shareholder amounts on the Deemed Paid Tax Report are not impacted by the Section 960(c) DPT reduction. These values continue to transfer to the Form 1118 Schedules C, D, and E. However, we modified the Post'86 Income Taxes Pools Report (and related Detail report) to deplete and display the Deemed Paid Tax to Shareholders - Section 956 amounts net of any applicable 960(c) DPT reduction.

We inserted the 960(c) Reductions of Taxes line in the

Deemed Paid Tax Credits (US$)

section of the Subpart F -Summary Reports for U.S. Shareholders directly below the Investments in U.S. Property line. Use the 960(c) Reductions of Taxes line to verify the reduction calculated during Subpart F computes.note

The Investment in U.S. Property amount is the deemed paid credit before Section 960(c) reduction.

The Subpart F - Income Inclusion Reports also display the Gross-Up on IUSP amounts net of any applicable 960(c) Deemed Paid Tax Reduction.