U.S. and Foreign Source Income Tracking for Tax Year 2013 and Later

Beginning with tax year 2013, ONESOURCE allows foreign entity earnings to be tracked separately between U.S. and foreign sources within a given foreign basket. When a deemed or actual distribution is made from a foreign corporation that is owned directly or indirectly 50% or more by Foreign Tax Credit (FTC) entities, ONESOURCE will determine the percentage of the subpart F, Section 956, and/or cash dividend that will be considered U.S. and/or foreign source income to the recipient under Section 904(h).

Creating U.S. and Foreign Source Codes

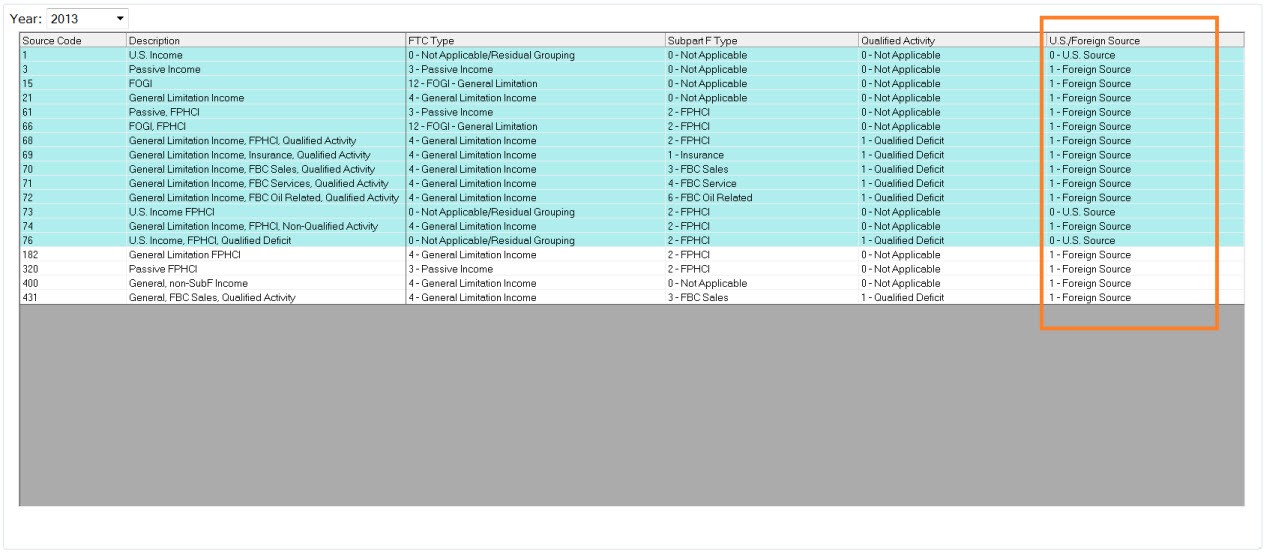

System and user defined source codes are listed in the

Source Code Definition

screen and are used to allocate and apportion account balances in the Income Sourcing Workpaper. Source codes differentiate income between Subpart F and non-Subpart F, Section 904(d) basket, passive income categories for high tax kick-out calculations, 863(b) income and, for tax year 2013 and later, U.S.and foreign source income for Section 904(h) calculations.We added a new

U.S./Foreign Source

column to the Source Code Definition

screen to identify income and expenses as either U.S. or foreign source within a given basket for use during the foreign entity calculations (E&P, Look Through and Subpart F). When importing source codes, each row should have either a 0 or 1 to represent the U.S./Foreign Source indicator setting.note

The U.S./Foreign Source indicator has no impact on the Foreign Tax Credit calculations (TIBS and FTC).

During rollover from 2012 to 2013 and as new source codes are created in tax year 2013 and later, ONESOURCE Income Tax - RS defaults the initial setting of the U.S./Foreign Source column based on the FTC Type as follows:

- 0 - U.S. Income / 0 - U.S. Source

- 3 - Passive Income / 1 - Foreign Source

- 4 - General Limitation Income / 1 - Foreign Source

- 12 - FOGI - General Limitation / 1 - Foreign Source

- User Defined Basket / 1 - Foreign Source

While source codes defined as passive, general limitation or user defined basket income can be either U.S. or foreign source income, you cannot change the U.S./Foreign indicator for source codes with an FTC Type of U.S. Income or FOGI. When source codes are rolled from 2013 to 2014 (and later), the U.S./Foreign indicator rolls over unchanged.

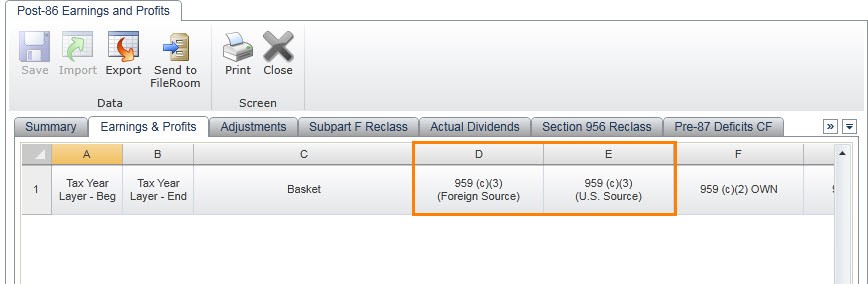

Identifying U.S. and Foreign Source Post-86 Earnings and Profits

The

Post-86 Earnings and Profits

screen is used to enter historical balances of E&P by tax year earned and Section 959(c) category. Any adjustment to, reclass within, or distribution from, the pool can be tracked in one of the many tabs in this screen. For tax years 2013 and later, we added separate 959(c)(3) (U.S. Source)

and 959(c)(3) (Foreign Source)

columns to the Post-86 Earnings and Profits

tabs and the related import templates.note

Pre-87 E&P layers cannot be separated into U.S. and foreign source earnings. Any actual or deemed distribution from Pre-87 will be considered foreign source in the hands of the recipient.

During rollover from 2012 to 2013, ONESOURCE Income Tax - RS rolls 959(c)(3) amounts in the Post-86 Earnings and Profits tabs to either the 959(c)(3) (U.S. Source) or 959(c)(3) (Foreign Source) column by basket as follows:

- 1 - U.S. Income / 0 - U.S. Source

- 3 - Passive Income / 1 - Foreign Source

- 21 - General Limitation Income / 1 - Foreign Source

- 15 - FOGI - General Limitation / 1 - Foreign Source

- User Defined Basket / 1 - Foreign Source

While amounts in the passive, general limitation and user defined basket can be either U.S. or foreign source, income in the U.S. and FOGI baskets can only be U.S. source and foreign source, respectively. After rollover to 2013, review and adjust the Post-86 959(c)(3) earnings as necessary. When E&P is rolled from 2013 to 2014 (and later), the allocation of earnings between the U.S. and foreign source earnings is retained.

Classifying Subpart F Recapture

The

Subpart F Recapture

screen is used to carry into the current year any excess Subpart F income due to a prior year limitation under Section 952(c)(1) for recharacterization in subsequent taxable years. For tax years 2013 and later, we added separate 959(c)(3) (U.S. Source)

and 959(c)(3) (Foreign Source)

columns to the screen and import template.

During rollover from 2012 to 2013, ONESOURCE rolls amounts in the Subpart F Recapture screen to either the Foreign Source Amount or U.S. Source Amount column by basket as follows:

- 1 - U.S. Income / 0 - U.S. Source

- 3 - Passive Income / 1 - Foreign Source

- 21 - General Limitation Income / 1 - Foreign Source

- 15 - FOGI - General Limitation / 1 - Foreign Source

- User Defined Basket / 1 - Foreign Source

While amounts in the passive, general limitation and user defined basket can be either U.S. or foreign source, income in the U.S. and FOGI baskets can only be U.S. source and foreign source, respectively. After rollover to 2013, review and adjust the Subpart F Recapture as necessary. When amounts are rolled from 2013 to 2014 (and later), the allocation of recapture between the U.S. and foreign source earnings will reflect the classification of the beginning amounts in the 2013 data entry screen and the impact of any calculated current year additions or reductions.

Subpart F Calculations

When a deemed or actual distribution is made from a foreign corporation that is owned directly or indirectly 50% or more by Foreign Tax Credit (FTC) entities, ONESOURCE Income Tax - RS determines the percentage of the subpart F, Section 956, and/or cash dividend that will be considered U.S. and/or foreign source income to the recipient under Section 904(h).

Current Year Earnings and Subpart F Inclusion

The current year earnings for a basket are broken into U.S./Foreign source components based on the attributes of the source code used for allocation and apportionment in the Income Sourcing Workpaper. The determination of subpart F income, including any reclassification between subpart F and non-subpart F source codes because of the deminimis, full inclusion and/or high tax election, retains the U.S./Foreign source attribute of the originating source code.

Any amount entered in the

PFIC / Tentative Boycott Income

field on the Investment in U.S. Property

screen is prorated between U.S. and foreign source within each basket using the following formula:U.S. (or Foreign) Source After Tax E&P excluding 959(b) dividends

Less: U.S. (or Foreign) Source Subpart F after Section 952(c) Recapture

Multiplied by:

- Total PFIC Tentative Boycott Income

- Divided by:

- Total After Tax E&P

- Less: Total Subpart F after Section 952(c)(2) Recapture

While Subpart F Recapture balances are now tracked by basket and U.S./Foreign Source indicator, the determination of the total subpart F income that can be recaptured has not changed. After the total Subpart F Recapture is calculated, it is prorated between U.S. and foreign source within each basket using the following formula:

Total Subpart F Recapture from the Data Entry Screen for a Given Basket U.S. (or Foreign) Source

Multiplied by:

- Total Subpart F Recapture the can be Used in the Current Year

- Divided by:

- Prior Year Excess Subpart F Income

If the foreign corporation's ownership by FTC entities is at least 50%, the portion of the subpart F inclusion that is U.S. source and the related Section 78 gross-up are reclassified to the U.S. basket on the Summary Report for U.S. Shareholders and the Foreign Income Inclusion Reports. During the International Transfer to the FTC parents, these amounts will be sourced to the U.S. basket. The part of the subpart F inclusion that is foreign source and the related Section 78 gross-up remain within the foreign basket for income inclusion purposes. If 904(h) does not apply (the foreign corporation is owned less than 50% by FTC entities), the subpart F income and Section 78 gross-up, regardless of the foreign or U.S. classification in the foreign entity, will be considered foreign source income to the FTC parent and transferred to the foreign basket during the International Transfer.

Dividend Income Depletion and Sourcing at the Recipient Level

The calculation of the total dividend from the 959(c)(3) earnings pool has not changed, nor has the allocation of that total to each basket. Once the total dividend amount has been determined for a basket, the amount is prorated between U.S. and foreign source based on the available amount of Post 86 959(c)(3) earnings in the basket for each classification (U.S./Foreign Source).

The ONESOURCE Income Tax classification of dividend income at the recipient level as either U.S. or foreign source depends on following:

Is the recipient a foreign or FTC entity?

Is the foreign corporation owned at least 50% by FTC entities?

Is at least 10% of the foreign entity's current year earnings* U.S. source?

note

* Current year earnings are calculated as After Tax E&P (excluding any return of capital and net 959(b) dividends) plus any amount in International Account Type 5170 (Interest - CFC Intercompany Payment).

FTC Recipient / At Least 50% FTC Ownership / At Least 10% U.S. Source Current Year Earnings

Distributions from previously taxed income are considered foreign source by ONESOURCE Income Tax and are reflected in the foreign basket columns on the income inclusion reports. The portion of the dividends distributed from U.S. source Post 86 959(c)(3) earnings and the related Section 78 gross-up are reclassified to the U.S. basket on the Summary Report for U.S. Shareholders and Foreign Income Inclusion Reports. During the International Transfer to the FTC parents, these amounts will be sourced to the U.S. basket. The part of the Post 86 959(c)(3) dividend that is foreign source and the related Section 78 gross-up remain within the foreign basket for income inclusion purposes.

FTC Recipient / At Least 50% FTC Ownership / Less Than 10% U.S. Source Current Year Earnings

OR

FTC Recipient / Less Than 50% FTC Ownership

Distributions from previously taxed income are considered foreign source by ONESOURCE Income Tax and are reflected in the foreign basket columns on the income inclusion reports. Since the foreign corporation is owned less than 50% by FTC entities, or is owned at least 50% but less than 10% of its current year earnings are U.S. source, the 904(h) exception applies. Dividends distributed from Post 86 959(c)(3) earnings and the related Section 78 gross-up, regardless of the foreign or U.S. categorization in the foreign entity, will be considered foreign source income to the FTC parent and transferred to the foreign basket during the International Transfer.

Foreign Recipient

Distributions from previously taxed income are considered foreign source and retain the same 959 categorization as they flow from the lower tier foreign corporation into upper tier entity within ONESOURCE Income Tax. Dividends distributed from 959(c)(3) earnings flow to the upper tier foreign entity's Post 86 E&P pools with the same U.S. or foreign source categorization of the payor.

Current Year Section 956 Inclusion

The calculation of the total Section 956 inclusion from the Post 86 959(c)(3) earnings pool has not changed, nor has the allocation of that total to each basket. Once the total Section 956 reclassification has been determined for a basket, the amount is prorated between U.S. and foreign source based on the available amount of 959(c)(3) earnings in the basket for each classification (U.S./Foreign Source).

If the foreign corporation's ownership by FTC entities is at least 50% and at least 10% of the foreign entity's current year earnings* are U.S. source, the portion of the 956 inclusion that is U.S. source and the related Section 78 gross-up are reclassified to the U.S. basket on the Summary Report for U.S. Shareholders and Foreign Income Inclusion Reports. During the International Transfer to the FTC parents, these amounts will be sourced to the U.S. basket. The part of the 956 inclusion that is foreign source and the related Section 78 gross-up remain within the foreign basket for income inclusion purposes.

note

* Current year earnings are calculated as After Tax E&P (excluding any return of capital and net 959(b) dividends) plus any amount in International Account Type 5170 (Interest - CFC Intercompany Payment).

If the foreign corporation is owned less than 50% by FTC entities, or is owned at least 50% but less than 10% of its current year earnings are U.S. source, the 904(h) exception applies. Under the 904(h) exception, ONESOURCE Income Tax will consider the 956 inclusion and Section 78 gross-up foreign source income to the FTC parent and allocate the amounts to the foreign basket during the International Transfer, regardless of the foreign or U.S. reclassification in the foreign entity.

Deficit Carryforward / Carryback

The conditions that trigger deficit carryforward and carryback, along with the amount of the deficit that moves in each basket, is unchanged. If ONESOURCE Income Tax determines that a Pre 87 deficit should be carried forward to the Post 86 pool, the amount flows to the foreign source column for all baskets other than the U.S. Basket (where it flows to the U.S. source column).

After ONESOURCE Income Tax determines the total Post 86 deficit to carryback to Pre 87 earnings in a basket, the total deficit carryback is allocated between U.S. Source and Foreign Source columns as follows:

If deficits are present in both the 959(c)(3) U.S. and foreign source categories, prorate the total carryback for the basket between them as:

- Total Deficit Carryback for the Basket

- Multiplied by:

- 959(c)(3) U.S. (or Foreign) Source Deficit for the Basket

- Divided by:

- Total 959(c)(3) Deficit for the Basket

If deficits for the basket are present in only one of the 959(c)(3) categories (U.S. or foreign source), allocate the total deficit carryback to the category with the deficit.

Hovering Deficit Utilization

The calculation of the total hovering deficit to be utilized by basket is the same as in prior years. However, after ONESOURCE Income Tax determines the total hovering deficit utilization for a basket, the amount is allocated between the basket's U.S. Source and Foreign Source columns on the E&P Pools Report as follows:

If available earnings to offset are present in both the 959(c)(3) U.S. and foreign source categories, prorate the total utilization between them as:

- Total Hovering Deficit Utilization for the Basket

- Multiplied by: 959(c)(3) U.S. (or Foreign) Source Available Earnings to Offset for the Basket

- Divided by: Total 959(c)(3) Available Earnings to Offset for the Basket

If available earnings to offset for the basket are present in only one of the 959(c)(3) categories (U.S. or foreign source), allocate the total utilization for the basket to the category with the available earnings.

Post 86 Tax Pool and Deemed Paid Credits

ONESOURCE Income Tax International does not track historical or current taxes by U.S. or foreign source, and the calculation of any deemed paid credit on a distribution is unchanged.