2024 Tax code to form 1042-S income code mapping

Overview of 2024 changes for form 1042-S

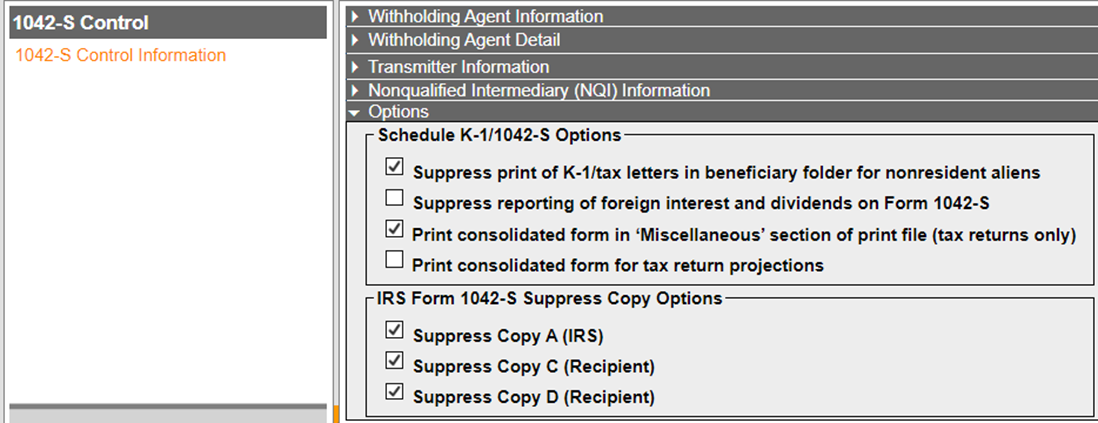

For 2024, you need to report bank deposits for nonresident alien individuals in Ecuador. The IRS has eliminated Form 1042-S, Copy E (Withholding Agent) for tax year 2024. We have modified the

2024 1042-S Control

screen as a result:

- In the Schedule K-1/1042-S Options frame, we have revised thePrint consolidated form for Copy E (Withholding Agent)checkbox to readPrint consolidated form in ‘Miscellaneoussection of the print file (tax returns only).

- In the ‘IRS Form 1042-S Suppress Copy Options’ frame, we have removed theSuppress Copy E (Withholding Agent)checkbox.

Map ONESOURCE Trust Tax income codes to form 1042-S income codes

Use this table to map ONESOURCE Trust Tax income codes to from 1042-S income codes.

1042-S income code | Description | ONESOURCE Trust Tax code | Chapter 3 tax rate | Chapter 3 exemption code | Chapter 4 exemption code |

|---|---|---|---|---|---|

01 Interest paid by U.S. obligors-general | Tax-exempt interest | 11, 83, 85, 121, 123, 124, 136, 137, 447, 448, 497, 498 | N/A | 2-Exempt under IRC | 15-Payee not subject to chapter 4 withholding See Note 5 (page 7) for link. |

01 Interest paid by U.S. obligors-general | Domestic non-portfolio interest | 7, 8, 9, 13, 55, 86, 92, 107, 183, 184, 185, 186, 215, 216, 217, 218, 226, 228, 493, 494, 496 where the Asset Non-portfolio interest income flag was set | Rate determined from tax treaty table 1, Income Code Number 1 column. See Note 4 (page 7) for link. | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

01 Interest paid by U.S. obligors-general | Domestic portfolio interest See Note 1 (page 7). | 7, 8, 9, 13, 55, 86, 92, 107, 183, 184, 185, 186, 215, 216, 217, 218, 226, 228, 493, 494, 496 where the Asset Non-portfolio interest income flag was not set | N/A | 5-Portfolio interest exempt under IRC | 15-Payee not subject to chapter 4 withholding |

02 Interest paid on real property mortgages | Excess inclusion income | 84 | Rate is 30% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

04 Interest paid by foreign corporations | Foreign interest See Note 2 (page 7). | 10, 227, 495 | N/A | 3-Income is not from U.S. sources | 15-Payee not subject to chapter 4 withholding |

06 Dividends paid by U.S. corporations-general | U.S. Corporation dividends See Note 1 (page 7). | 1, 5, 6, 114, 132, 500, 502, 503, 599, 163 | Rate determined from tax treaty table 1, Income Code Number 6 column. See Note 4 (page 7) for link. | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

06 Dividends paid by U.S. corporations-general | U.S. Corporation dividends from foreign source | 2, 520 | N/A | 3-Income is not from U.S. sources | 15-Payee not subject to chapter 4 withholding |

06 Dividends paid by U.S. corporations-general | Dividends from 80/20 companies | 98 | N/A | 2-Exempt under IRC | 15-Payee not subject to chapter 4 withholding See Note 5 (page 7) for link. |

06 Dividends paid by U.S. corporations-general | Section 897 Capital Gains | 164 | Rate is 30% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

08 Dividends paid by foreign corporations | Foreign dividends See Note 2 (page 7). | 3, 501 | N/A | 3-Income is not from U.S. sources | 15-Payee not subject to chapter 4 withholding |

09 Capital gains | Distributed capital gains | System default is to populate only if the Include capital gains on Form 1042-S Compute-Federal option is selected. This includes all distributed capital gains (excluding those related to tax codes 99 and 157). | Rate is 30% | No Exemption Code | 15-Payee not subject to chapter 4 See Note 5 for link. |

09 Capital gains | 302 Merger Delivery vs. Payment | 99 (if distributed) | N/A | 2-Exempt under IRC | 15-Payee not subject to chapter 4 withholding |

14 Real property income and natural resources royalties | Real property income and natural resources royalties | Passive rental/royalty income. Rental/royalty income with material participation may or may not be included depending on Compute-Federal option selection. | Rate is 30% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

23 Other income | Other income | 44, 60, 89, 90, 472, 473 plus state overpayment applied. Also, any portfolio ordinary gain would be included in this amount. | Rate is 30% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

27 Publicly traded partnership distributions subject to IRC section 1446 | Partnership income | Ordinary income from a publicly traded partnership. See Note 6 for link. | Rate is 37% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

29 Deposit interest | Deposit interest See Note 3. | 51 | N/A | 2-Exempt under IRC | 15-Payee not subject to chapter 4 withholding |

30 Original issue discount (OID) | Original issue discount | 169, 192, 193, 196, 197, 506 | N/A | 5-Portfolio interest exempt under IRC | 15-Payee not subject to chapter 4 withholding |

33 Substitute payment-interest | Substitute payment-interest | 95 | Rate/exemption same as for portfolio interest | N/A | 15-Payee not subject to chapter 4 withholding |

34 Substitute payment-dividends | Substitute payment-dividends | 96 | Rate determined from tax treaty table 1, Income Code Number 6 column. See Note 4 for link. | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

35 Substitute payment-other | Substitute payment-other | 97 | Rate is 30% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

36 Capital gains distributions | Capital gain not subject to NRA Withholding | 156, 157 (if distributed) | N/A | 2-Exempt under IRC | 15-Payee not subject to chapter 4 withholding See Note 5 for link. |

37 Return of capital | Nondividend distributions | 4 | N/A | 2-Exempt under IRC | 15-Payee not subject to chapter 4 withholding See Note 5 for link. |

40 Other dividend equivalents under IRC section 871(m) (formerly 871(l)) | 871M dividend | 134 | Rate determined from tax treaty table 1, Income Code Number 6 column. | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

57 Amount realized under IRC section 1446(f) | §1446(f) proceeds subject to withholding | 526, 527 See Note 6 for link. | Rate is 10% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

57 Amount realized under IRC section 1446(f) | §1446(f) proceeds not subject to withholding | 528, 529 See Note 6 for link. | N/A | Exemption code based on recipient Chapter 3 status | 15-Payee not subject to chapter 4 withholding |

57 Amount realized under IRC section 1446(f) | Additional excess of cumulative net income (ECNI) | 530 If simple/complex trust or estate, selection §1446(f) checkbox on sales screen may also be used. See Note 6 for link. | Rate is 10% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

58 Publicly traded partnership distributions – undetermined | Publicly traded partnership distributions – undetermined | 139 See Note 6 for link. | Rate is 37% | No Exemption Code | 15-Payee not subject to chapter 4 withholding |

Note 1

Include interest and dividend amounts from your Schedule K-1s.

Note 2

You won't report interest paid by foreign corporations (income code 04) and dividends paid by foreign corporations (income code 08) on Form 1042-S if you selected the

Suppress reporting of foreign interest and dividends

option in the 1042-S Control settings.Note 3

You must report bank deposit interest to any nonresident alien individual who resides in a country with which the United States has agreed to exchange tax information under an income tax treaty, other convention, or bilateral agreement.

ONESOURCE Trust Tax automatically reports bank deposit interest on Form 1042-S for nonresident individuals whose country of residence meets these requirements. The list of countries is included in Revenue Procedure 2023-36.

To report bank deposit interest for all nonresident alien individuals, regardless of their country of residence, select the

Report bank deposit interest paid to nonresident individuals on Form 1042-S even if reporting is not required based on country of residence

Compute-Federal option. note

If you set the recipient Chapter 4 status code to

15-Nonparticipating FFI

and mark the Documentation not available or invalid

check box, the system automatically reports the bank deposit interest (subject to 30% withholding under Chapter 4) regardless of the recipient's residence.Note 4

The "Tax Treaties" section of IRS Publication 515 includes the following link to the tax treaty tables: https://www.irs.gov/individuals/international-taxpayers/tax-treaty-tables.

Note 5

You can set the Chapter 4 exemption code for these income types to 21 (Other payment not subject to chapter 4 withholding). See the following

Chapter 4 status code

for additional information.Note 6

You'll receive a separate Form 1042-S for each type of reportable income associated with a given publicly traded partnership (PTP). The system uses information from the PTP asset record (name, EIN, etc.) to populate box 16 (Payer information) of each Form 1042-S generated. We do not make any assumptions about the payer Chapter 3 and 4 status. The system does not automatically assume the Chapter 3 status for a payer is 38.

Example: If you receive $100 of partnership income (tax code 12) and $20 of PTP distributions – undetermined (tax code #139) from PTP A, and you also receive $400 of partnership income (tax code 12) from PTP B, the system generates three Form 1042-S for you as follows:

- 1st 1042-S – Income code 27 with gross income of $100, withholding at 37%.

- 2nd 1042-S – Income code 58 with gross income of $20, withholding at 37%.

- 3rd 1042-S – Income code 27 with gross income of $400, withholding at 37%.

Tax rate comments

- The system applies a Chapter 3 tax rate of 30% to all reportable income not subject to an exemption, including portfolio interest, when you mark theDocumentation not available or invalidcheck box for the recipient, as instructed in IRS Publication 515 (see Presumption Rules). This action takes precedence over the recipient Chapter 3 status code checks. Refer to theChapter 4 commentswhen you set the recipient Chapter 4 status code to15-Nonparticipating FFI.

- The system applies a Chapter 3 tax rate of 30% to all income otherwise subject to treaty rates when you mark theNo election made to receive treaty ratescheck box for the recipient.

- The system applies Chapter 3 exemption code 04 (Exempt under tax treaty) with no withholding required, resulting in a 0% dividend withholding rate, when you select theRecipient eligible for special treaty dividends benefitscheck box and when U.S. corporate dividends is subject to reduced treaty rates based on the recipient country.

- The system doesn't add a tax rate when you set the recipient Chapter 3 status code to 19 (International Organization), 20 (Tax-exempt organization (Section 501(c) entities), 36 (Foreign Government-Integral Part), or 37 (Foreign Government-Controlled Entity).

- The system applies a Chapter 3 tax rate of 4% when you set the recipient Chapter 3 status code to 18 (Private Foundation).

- The system applies a default tax rate of 30% when none of the above exceptions are met and the recipient country is not listed in the Publication 515 table.

Exemption logic exceptions

- The Chapter 3 exemption code is set to 24 (Exempt under section 892) when the recipient Chapter 3 status code is set to 19 (International Organization), 36 (Foreign Government-Integral Part), or 37 (Foreign Government-Controlled Entity).

- The Chapter 3 exemption code is set to 2 (Exempt under IRC) when the recipient Chapter 3 status code is 20 (Tax-exempt organization (Section 501(c) entities)).

- The Chapter 3 exemption code is set to 7 (WFP or WFT) when the recipient Chapter 3 status code is 09 (Withholding Foreign Partnership) or 11 (Withholding Foreign Trust).

Box 3

According to the Form 1042-S Instructions, you must enter either 3 or 4 (but not both) on each Form 1042-S. If you don't report amounts in boxes 7 through 9, you should enter 3 in this box as per IRS guidelines.

Chapter 4

The system subjects all income to Chapter 4 reporting and applies a Chapter 4 tax rate of 30% when the recipient Chapter 4 status code is set to

15-Nonparticipating FFI

and the Documentation not available or invalid

" check box is marked. This includes bank deposit interest, and the recipient's country situs doesn't impact reporting for Chapter 4 purposes. The Chapter 3 exemption is set to 12 (Payee subjected to Chapter 4 withholding). The system assumes all income to be subject to Chapter 3 if no Chapter 4 information (rate or exemption code) for a given income code is entered. In this case, either a Chapter 3 tax rate or exemption is applied. When the income is subject to Chapter 3 (the system default), 15 (Payee not subject to Chapter 4 withholding) is printed in Box 4a, and 00.00 is printed in Box 4b, unless otherwise indicated in Note 5.

The system prints 12 (Payee subjected to Chapter 4 withholding) in Box 3a and 00.00 in Box 3b if either a Chapter 4 tax rate or exemption code is entered.

Income codes 51, 52, 53, and 54

Use income codes 51, 52, 53, and/or 54 if you paid income (interest or dividends) and claim a reduced rate of withholding under an income tax treaty, but the recipient does not provide a U.S. or foreign TIN.

If the recipient doesn't have a TIN and you apply a Chapter 3 tax rate reduced to less than 30% under an income tax treaty, or if you use Chapter 3 exemption code 04 (Exempt under tax treaty), ONESOURCE Trust Tax will revise the income codes as follows:

- Changes interest described by income code 01 (Interest paid by U.S. obligors-general) to income code 51.

- Changes dividends described by income code 06 (Dividends paid by U.S. corporation-general) to income code 52.

- Changes dividends described by income code 34 (Substitute payment-dividends) to income code 53.

- Changes interest described by income code 33 (Substitute payment-interest) to income code 54.

note

ONESOURCE Trust Tax doesn't make these changes when a Chapter 3 exemption applies (unless the Chapter 3 exemption code is 04) or if the withholding rate is 30%.

For example, if a recipient from China has a U.S. TIN of FORM1042S and you do not specify a foreign TIN, and you pay $1,000 in dividends from a U.S. corporation to this recipient, you apply a 10% withholding rate on dividend income according to Table 1 of IRS Publication 515.

Since the recipient's U.S. TIN is not valid and the withholding rate on the dividend income is less than 30%, you should use income code 52 (Dividends paid on certain actively traded or publicly offered securities) instead of income code 06 (Dividends paid by U.S. corporations-general).

note

Income code revisions don't occur if you enter the income code in the 1042-S Additional Income collapsible section at the recipient level. For instance, if you entered income code 06 in this section, ONESOURCE Trust Tax would not change it to income code 52, even if the withholding rate is less than 30% and no recipient TIN is provided.

Rounding

IRS Form 1042-S Instructions indicate "You must round off cents to whole dollars." All amounts reported on the actual Form 1042-S and consolidated Form 1042-S (if generated as a withholding agent copy or part of a projection) are rounded to whole dollars. Amounts filed with the IRS are rounded as well and are the same as those reported on the printed output. For example:

- Asset A generates Dividends paid by U.S. corporations-general (income code 06) of $4.20.

- Asset B generates Dividends paid by U.S. corporations-general (income code 06) of $6.40.

- The recipient receives 100% of income. All dividends noted above are subject to 30% withholding. Asset-level detail for income is generated when the account is processed.

When the Compute-Federal option is set to prepare the return with dollars, the 1042-S form/filing indicates $10 of gross income (the dividend from each asset is rounded so that there is $4 for Asset A and $6 for Asset B). Withholding is then computed. The result is $3 (30% of $10).

When the Compute-Federal option is set to prepare the return with cents, the 1042-S form/filing indicates $11 of gross income (the total amount of $10.60 is rounded to $11). Withholding is then computed. The result is $3 (30% of $11, or $3.33 rounded to the nearest dollar).

Unique form identifier

The IRS requires withholding agents to assign a 10-digit numeric unique identifying number to each Form 1042-S they file, as stated in the Form 1042-S instructions. ONESOURCE Trust Tax automatically generates this unique number for each Form 1042-S. This number is printed on both the IRS substitute Form 1042-S and the consolidated Form 1042-S output (if generated), and it is included with the information filed with the IRS.

Form 1042-S output

Publication 1179 instructs that you can't include multiple income types for the same recipient on Copies A, B, C, and D of Form 1042-S.

According to the IRS, you can only submit 1 Form 1042-S per page, regardless of orientation. Therefore, the substitute form includes only one Form 1042-S per page, rather than 2, and it generates in portrait orientation.

You can't generate or include the consolidated Form 1042-S format in the beneficiary packet when you process a tax return.

- Copy A (for the IRS) automatically generates unless you suppress it by selecting the Suppress Copy A (IRS) 1042-S Control option. You should select the option to suppress Copy A unless you plan to paper file the form with the IRS. If you generate it, the form is included in the Miscellaneous section of the print file.

- Copy B (for the recipient) always generates and is included in the Beneficiary section of the print file.

- Copy C (for the recipient to attach to the federal tax return) automatically generates unless you suppress it by selecting the Suppress Copy C (Recipient) 1042-S Control option. If you generate it, the form is included in the Beneficiary section of the print file.

- Copy D (for the recipient to attach to the state tax return) automatically generates unless you suppress it by selecting the Suppress Copy D (Recipient) 1042-S Control option. If you generate it, the form is included in the Beneficiary section of the print file.

- Form 1042-S recipient instructions is in the Beneficiary section for each recipient for whom you generated a Form 1042-S.

note

- Since you include Copies B, C, and D in the Beneficiary section of the print file, they, along with the Form 1042-S Instructions, are available for Mail Service.

- If you select thePrint consolidated form for tax return projections1042-S Control option, then include the consolidated version of the 1042-S in the Beneficiary section of the print file. Don't include it in the Miscellaneous section.

Corrections print

Form 1042-S AMENDED box

The

AMENDED

box on Form 1042-S is marked when:

- TheType of 1042-S (for printed form only)drop-down list is set toAmended. This drop-down list is in theForm 1042-S Recipient Informationcollapsible section on theRecipient Detailpage.

- An amendment number is indicated in theAMENDMENT NO.box on Form 1042-S.

note

The system marks the

AMENDED

box even though the Form 1042-S is electronically filed. Unique form identifier and amendment no. fields

The IRS requires you to assign a 10-digit Unique Form Identifier (UFI) to each Form 1042-S return that you file. The UFI is necessary for both original and amended Form 1042-S returns. When you file an amended Form 1042-S, it must have the same UFI as the original Form 1042-S you are amending. ONESOURCE Trust Tax automatically generates the UFI during processing.

The IRS also requires you to include an amendment number for any amended Form 1042-S you file. For corrections print, ONESOURCE Trust Tax determines the UFI and amendment number based on the following criteria:

- No change: If there are no changes to an originally filed Form 1042-S then the UFI is the same as the originally filed Form 1042-S. The Form 1042-S AMENDMENT NO. box is blank.

- Change to an originally filed Form 102-S: If there's a change to an originally filed Form 1042-S, then the 1042-S return generated in the corrections keeps the same UFI as the original. A ‘1’ prints in the Form 1042-S AMENDMENT NO. box.

- ONESOURCE Trust Tax defines the following as a change to an originally filed Form 1042-S:

- Only amounts (gross income and/or withholding) have changed from the original filing.

- Only the income code has changed from the original filing.

- The income code and gross income are the same as the original filing.

- New Form 1042-S: If there is a new Form 1042-S that wasn't originally filed then the new Form 1042-S generated in the corrections print has a different UFI. The AMENDMENT NO. box for the new Form 1042-S is blank. Any Form 1042-S generated during corrections print that doesn't meet the criteria included in the two bullet items preceding is considered a new Form 1042-S.

Printing corrected form 1042-S with no gross income

A corrected or revised form 1042-S with no gross income reportable for a given income code can be generated by selecting the Force 1042-S with No Gross Income (Corrections Only) check box, which is available under the 1042-S Income Overrides and 1042-S Additional Income collapsible sections on the Recipient Detail page.

You can generate a corrected or revised Form 1042-S with no gross income reportable for a given income code when you mark the

Force 1042-S with No Gross Income (Corrections Only)

check box. This option is available under the 1042-S Income Overrides

and 1042-S Additional Income

sections on the Recipient Detail

page.