Version 10 - March 2025 (CUD release)

Content update information

The CUD Release focuses on the legislative content changes for the period ending December 2025.

- Financial Period Type: 12-Months (Annual)

- Target Industry Type: Manufacturing, Services, and Generic (excluding Financial Services)

IFRS legislative changes

- International Tax Reform - Pillar Two Model Rules – Amendments to IAS 12

- Classification of Liabilities as Current or Non-current and Non-current Liabilities with Covenants - Amendments to IAS 1

- Lease Liability in a Sale and Lease-back - Amendments to IFRS 16

- Disclosures: Supplier Finance Agreements - Amendments to IAS 7 and IFRS 7

- Lack of exchangeability - Amendments to IAS 21

- Sale or Contribution of Assets between an Investor and its Associate or Joint Venture - Amendments to IFRS 10 and IAS 28

- Classification and Measurement of Financial Instruments - Amendments to IFRS 9 and IFRS 7

- IFRS 18 - Presentation and Disclosure in Financial Statements

- IFRS 19 - Subsidiaries without Public Accountability: Disclosures

- Improvements to International Financial Reporting Standards

- Contracts Referencing Nature-dependent Electricity - Amendments to IFRS 9 and IFRS 7

Early adoption standards

- The amendments take effect immediately upon issuance, but certain disclosure requirements become effective later. The temporary exception from recognition and disclosure of information about deferred taxes, along with the requirement to disclose the application of the exception, applies immediately and retrospectively upon the issuance of the amendments.

- Entities must disclose the current tax expense related to Pillar Two income taxes and disclosures for periods before the legislation becomes effective for annual reporting periods beginning January 1, 2023. These disclosures are not required for any interim period ending December 31, 2023.

- The amendments apply to annual periods starting January 1, 2024. Entities must apply them retrospectively. Early application is permitted, and entities must disclose it. However, an entity that applies the year 2020 amendments early must also apply the year 2022 amendments, and vice versa.

- A seller-lessee applies the amendment to annual reporting periods beginning January 1, 2024. Earlier application is allowed, and entities must disclose this fact.

- A seller-lessee applies the amendment retrospectively in accordance with IAS 8 to sale and lease-back transactions entered into after the date of initial application. The amendment doesn’t apply to sale and lease-back transactions entered into before the date of initial application. The date of initial application is the beginning of the annual reporting period in which an entity first applied IFRS 16.

- The amendments become effective for the annual reporting periods starting January 1, 2024. Early adoption is permitted and must be disclosed. The amendments offer some transition relief regarding comparative and quantitative information at the beginning of the annual reporting period and interim disclosures.

- The amendments take effect for the annual reporting periods beginning January 1, 2025. Early adoption is allowed, but entities must disclose it. When applying the amendments, an entity can't restate comparative information.

- The Board issued Amendments to the Classification and Measurement of Financial Instruments (Amendments to IFRS 9 and IFRS 7) in May 2024. These amendments will be effective for the annual reporting periods beginning on January 1, 2026. Entities can early adopt the amendments related to the classification of financial assets and the related disclosures, while applying the other amendments later.

- IFRS 18 and amendments to other accounting standards become effective for the reporting periods starting January 1, 2027 and will be applied retrospectively. Early adoption is permitted and must be disclosed.

- IFRS 19 is effective for the reporting periods beginning January 1, 2027, and earlier adoption is permitted. An eligible entity that chooses to apply the standard earlier is required to disclose that fact.

- The Amendments to IFRS 9 and IFRS 7 become effective for the annual reporting periods starting on January 1, 2026. Early adoption is allowed and must be disclosed.

note

While the Final Good Group for 2025 is still in progress and the final scope will be defined later, it is likely that these changes will impact all entities. While International Tax Reform applies to Good Group, it was not in scope for this specific entity and was disclosed as such. A disclosure example will be included in the Appendix, as in the prior year.

- In December 2015, the IASB decided to defer the effective date of the amendments until it finalizes any amendments resulting from its research project on the equity method. Early application of the amendments is still permitted and must be disclosed. The amendments must be applied prospectively.noteThis change won't be in the scope of the Final Good Group for 2025.

- The IASB's Annual Improvements process addresses non-urgent but necessary clarifications and amendments to IFRS. In July 2024, the IASB issued Annual Improvements to IFRS Accounting Standards - Volume 11.noteThe amendments from the Annual Improvements to IFRS Accounting Standards—Volume 11 will be applied in the Final Good Group for 2025.

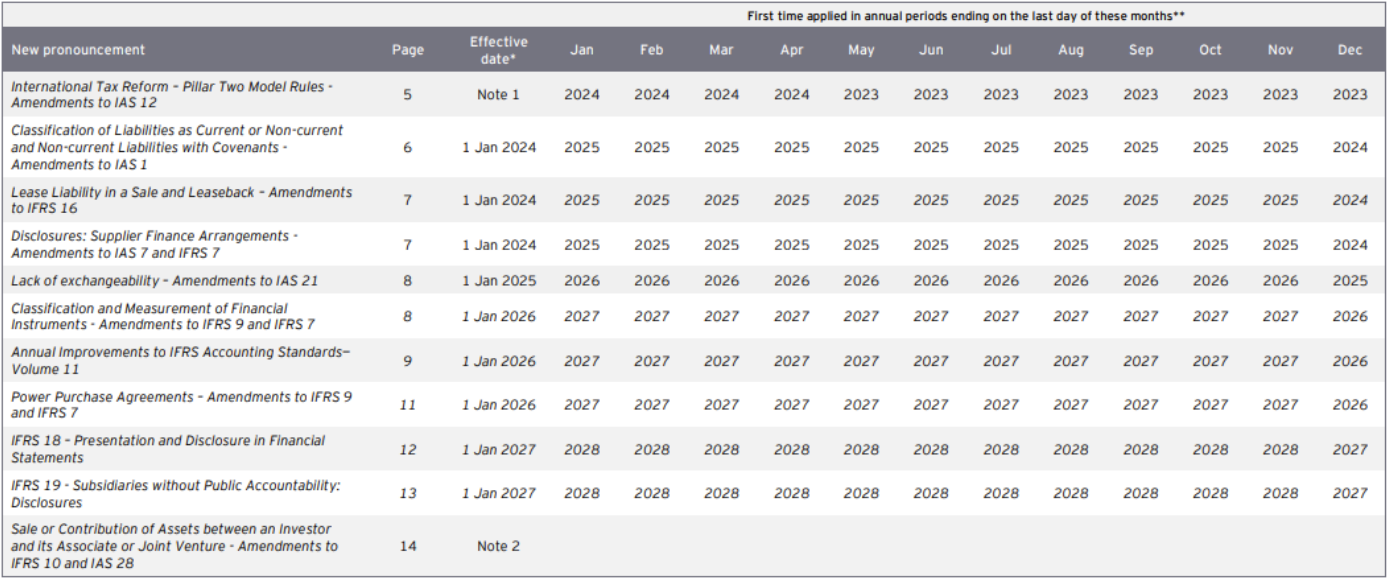

Table of mandatory application

*Effective for annual periods beginning on this date.

**Assuming that an entity hasn't adopted the pronouncement early according to specific provisions in the standard, interpretation, or amendment.

Note 1: The amendments are effective immediately upon issuance. The disclosure of the current tax expense related to Pillar Two income taxes. The disclosures in relation to periods before the legislation is effective are required for annual reporting periods beginning January 1, 2023. They aren't required for interim period ending on or before December 31, 2023.

Note 2: In December 2015, the IASB postponed the effective date of this amendment pending the outcome of its research project on the equity method of accounting.

Additional information

This overview covers year-end reporting until December 31, 2025. Therefore, it includes pronouncements with an effective date of January 1, 2025, as these must be applied for the 1st time for financial years ending, for example, on January 31, 2025.

If the

1st time applied in annual periods end on the last day of the month

is December 2025, this means a company with a year ending on December 31, 2024 would apply this standard for the annual period ending December 31, 2025. In other words, it is for the reporting period from January 1, 2025 until December 31, 2025.Related Content

-

IFRS

Format: Article

Article