There is a stark contrast that’s developing between Am Law 100 and Midsize firms as Am Law 100 firms increase rates and invest the gains back in infrastructure, while Midsize firms see steady demand but flagging rates that make it a struggle to handle historically high expenses

Key takeaways:

-

-

-

Falling behind on worked rates — Midsize firms grew worked rates by just 5.3% in Q1 2026, roughly half the Am Law 100’s 9.8% growth — a structural gap that has widened with every passing quarter.

-

Underinvesting in the tools that will define tomorrow — Midsize firms also invested 6.2% more in tech and knowledge management in the quarter — the lowest of any segment — leaving them at risk falling behind as larger peers accelerate their investment.

-

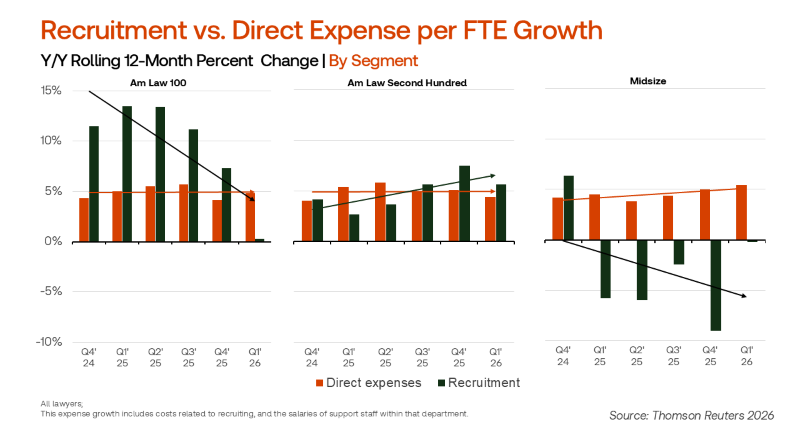

Sitting out the talent race — With recruiting expense growth at -0.2%, Midsize firms are virtually absent from the lateral market while their closest competitors saw 5.6% growth in their investment.

-

-

In Q1 2026, demand growth across all segments landed at 2.7% year-over-year, with Midsize firms coming in at 2.6%, essentially in line with the market average and comfortably ahead of the Am Law 100’s 1.2%, according to the Thomson Reuters Institute’s recent Q1 2026 Law Firm Financial Index (LFFI).

Based on this metric, Midsize firms are not underperforming, as they are capturing work at a pace that outstrips the elite tier; however, a deeper look shows a more nuanced story. The Am Law Second Hundred led all segments with demand growth of 3.9%, posting a notable advantage over the Midsize segment. That growth was enough to make up the ground ceded by the Am Law 100 that the Am Law 200 as a whole still managed to outstrip the Midsize segment in terms of demand growth.

That makes the demand story a very mixed one for Midsize firms. While they are holding their own against the very largest firms, the Am Law Second Hundred — Midsize’s most direct competitive set — is pulling significantly ahead on volume. If that gap persists, it could further shut the gates to demand gains. Of course, that would be made all the more impactful because of how rising demand influences firms’ ability to raise rates.

Rates are the most consequential gap in the data

If demand tells a moderately positive story for Midsize, worked rate growth is the point at which the data turns slightly more negative for the segment. In Q1 2026, Am Law 100 firms posted worked rate growth of 9.8%, the highest of any segment by a significant margin. The Am Law Second Hundred recorded 6.9% growth, while the overall market average was 7.0%. Midsize firms, meanwhile, came in at 5.3%.

That is a gap of more than 4.5 percentage points between Midsize and Am Law 100 firms, a magnitude outstripping the entirety of the Midsize segment’s demand gains.

What makes this especially significant is that the gap is not new — one year ago, in Q1 2025, the same hierarchy held, with Am Law 100 firms seeing worked rates grow at 9.4%, Second Hundred firms at 7.1%, and Midsize firms at 5.9%. In other words, the rate divergence between Midsize firms and the rest of the market has been consistent and is widening even further. The end result of this is stark: Midsize firms are growing revenue per hour of work at a pace roughly half that of their Am Law 100 counterparts, and that differential compounds over time into a meaningful profitability disadvantage.

Expenses diverge in the wrong direction

On the expense side of the ledger, the pattern reverses in a way that creates a genuine squeeze for Midsize firms. Looking at direct expenses — the costs most closely tied to delivering client work — Midsize firms recorded growth of 5.4% in Q1 2026, the highest of all three segments. This compares to 4.8% for the Am Law 100 and just 4.4% for the Am Law Second Hundred. That means that Midsize firms are generating the slowest rate growth while simultaneously growing their client-delivery costs the fastest. That combination reflects a textbook margin compression dynamic.

Overhead expenses per FTE tell a different story. Here, Midsize firms showed lower growth at 4.0%, well below the Am Law 100’s 6.7% and the Second Hundred’s 5.8%. On the surface this looks like cost discipline, but it is worth reading carefully: lower overhead investment, especially when coupled with the market’s high tech and talent expenditure pressures may actually reflect forced underinvestment rather than efficiency. Midsize firms may simply have less capacity to expand their infrastructure spending, not less need for it.

Making an opposite bet on talent

Indeed, one of the sharpest contrasts in the “Q1 2026 LFFI ” data involves recruitment expenses. The Am Law Second Hundred is investing heavily in lateral talent, seeing recruitment expense growth of 5.6%. The Am Law 100 has sharply pulled back, growing recruitment costs at just 0.3% — a signal that the largest law firms may be consolidating their existing talent base rather than expanding it aggressively. Midsize firms sit at the opposite extreme, with recruitment expense growth of -0.2%, essentially flat to slightly negative.

This difference is notable because the Am Law 100 and Midsize segments are pursuing fundamentally different headcount strategies. As Am Law firms focus on leaner headcount powered by rates, Midsize firms have finding much more of their revenue growth comes from growing aggregate hours worked by hiring more lawyers. Midsize firms’ decision not to leverage as much investment in this area could signal a shift in strategy, simple cost pressures, or perhaps a greater focus on which areas they spend their recruiting money. Whichever the driver, it’s a sizeable shift across a segment that’s already feeling pressure across multiple facets of their business.

The compound effect of this divergence

The “Q1 2026 LFFI” data highlights several reinforcing challenges facing Midsize firms: slowing demand and lagging rate growth, the highest direct expense growth but the lowest technology investment, and minimal lateral recruitment investment. While no single factor is critical, together these divergences show a widening gap between earnings and costs.

Of course, this is not to say that Midsize firms are going bankrupt — far from it. Midsize firms’ profitability, on average, is growing at a solid pace as demand and rates continue to power them forward, even as expenses weigh on their numbers.

What may be more concerning is what this means for the future potential of Midsize firms, especially as the market bifurcation grows and the Am Law firms increasingly pull away. As this continues, it’ll become harder and harder for Midsize firms to break into those ranks, compete for talent, and compete for the kind of bet the company work that is some of the most profitable in the legal industry. Reversing this course isn’t about Midsize firms’ 2026 results; rather, it’s about what they can achieve in 2030, 2040, and beyond.

You can download a full copy of the Thomson Reuters Institute’s Q1 2026 Law Firm Financial Index here