A new report shows a law firm market with exceptionally strong pricing and demand inputs; however, rising costs, slipping productivity, widening segment gaps, and geopolitical uncertainty are quietly flattening what should be a standout performance

Key takeaways

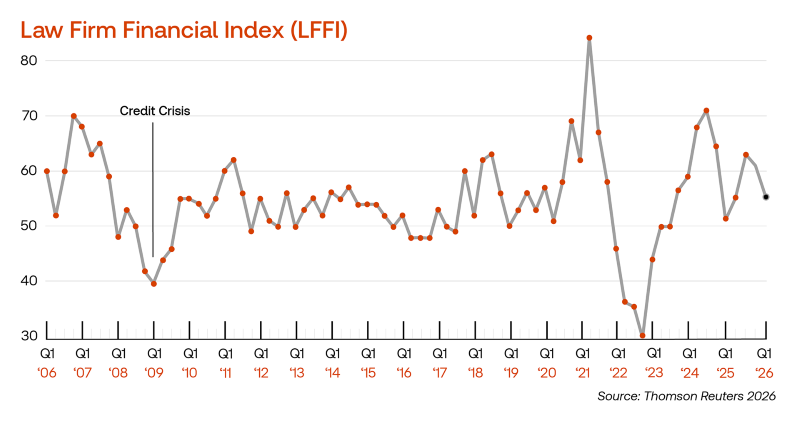

- Despite worked rate growth reaching above 12% for the largest of the Am Law 100 firms and demand growth hitting almost three-times its historical average, the LFFI landed at a flat 55, its own long‑run historical average.

- Overhead expenses climbed, productivity slipped back into contraction, and a widening performance gap between large firms and the rest dragged on overall results; meanwhile, the Iran war appears to be dampening demand on the edges of both transactional and counter-cyclical work.

- Am Law 100 firms continue to drive pricing power and lead technology investment, while Midsize firms have seen rate growth slow, demand lag, and costs rise faster than revenue, all reinforcing an increasingly scale‑driven competitive divide.

The Thomson Reuters Institute’s Law Firm Financial Index (LFFI) for the first quarter of 2026 landed at 55, exactly matching the long‑run historical average since the Index began tracking the market in 2006. On its face, that may sound unremarkable; but dig one layer deeper, and Q1 2026 becomes one of the more puzzling quarters we’ve seen in years.

Let’s start with the inputs. Am Law 100 firms pushed worked rate growth to almost 10%, building on an already record‑setting 2025 and marking one of the strongest pricing environments in recent memory — and at the very top of the market, the largest law firms cleared 12%-plus rate growth. Meanwhile, demand clocked in at 2.7%, nearly triple the industry’s long‑run average.

Clearly, these are not average conditions by any stretch. And yet, the LFFI score — a composite output of law firm financial performance — remained stubbornly ordinary.

So, what’s eating the gains? It turns out that the answer is multifold. For example, the report cites climbing overhead expenses, productivity that has slipped back into contraction after six months of gains, and a growing performance gap between the largest firms and everyone else — all joined forces to drag down the LFFI score.

On top of that, a new geopolitical variable — the ongoing war in Iran — weighs heavily, darkening the storm clouds further. Early indicators suggest the conflict is blunting both sides of demand at once, the report notes, freezing both the transactional M&A work that thrives on confidence and the counter-cyclical restructuring work that thrives on distress. When both the upside and downside stall simultaneously, strange results likely will follow.

The segments’ strategy split

Indeed, one of the clearest stories of Q1 is how sharply law firm segments are splitting apart. After years of moving largely in lockstep, pricing strategies diverged in Q1. Am Law 100 firms, for example, leaned hard into rate growth, while Midsize firms slowed their rate growth, marking the first deceleration in rate growth for any segment since 2021. Meanwhile, the Second Hundred held steady, neatly threading the middle.

This nuance matters. Large firms continued raising standard rates faster than worked rates, accepting deeper discounts to move the prices clients paid higher. Midsize firms did the opposite — allowing standard rates to lag while negotiated rates rose — signaling restraint. Midsize firms’ strategy may have been to capture price‑sensitive demand migrating down‑market; but in practice, it hasn’t worked. Midsize firm demand growth now trails the Am Law 200 average, expenses are accelerating faster than revenue, and productivity per lawyer is declining. As a result, profit growth for the segment is running at roughly half the pace of its Am Law peers.

Rain in the forecast?

Demand, meanwhile, still remains above historical norms, even as a few raindrops are starting to fall. While several practice areas contributed meaningfully, the mix of transactional and counter‑cyclical practices are growing at nearly the same pace, signaling not balance, but simultaneous deceleration. Add in tough year‑over‑year comparisons against early‑2025’s demand surge, and the growth picture going forward becomes more stormy.

As the report makes clear, the takeaway from Q1 is not that the market is in trouble, but rather that momentum is slipping under the surface. A score of 55 isn’t a storm warning siren; it is, however, an odd resting point for a market with inputs this strong. The question for the legal market moving forward is simple: Is this just a passing sprinkle — or the first sign of a heavier storm?

You can access the Thomson Reuters Institute’s Law Firm Financial Index (LFFI) for the first quarter of 2026 here

Follow us on social

Topics

Have questions?

Featured Event

The 34th Annual Chief Marketing & Business Development Officer Forum