Near-record rate growth and above-average demand defined the start of 2026; yet the LFFI landed at 55, exactly in line with its long-run average, underscoring a disconnect between hours and value, and highlighting how firms are converting strong inputs into performance

Key takeaways:

-

-

-

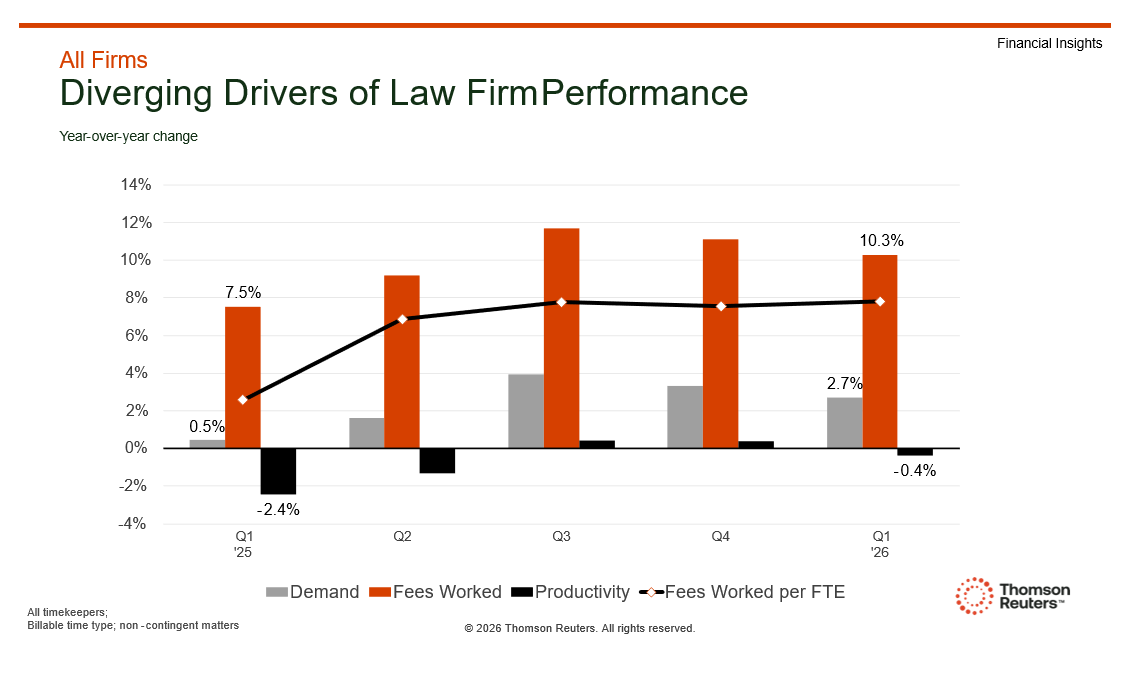

Productivity softened at an unexpected time — Productivity declined to -0.4% in Q1 2026, even as demand remained strong at 2.7% growth.

-

Value per lawyer provides the clearer signal — Fees worked per lawyer (or value per lawyer) continues to grow, reflecting the combined impact of hours and rates despite volatility in productivity.

-

Margin pressure is emerging unevenly — In the Midsize segment, value growth is trailing expense growth, creating early signs of compression.

-

-

The Q1 2026 results present an unusual combination. Demand grew by 2.7%, well above historical norms, and worked rate growth remained elevated, with Am Law 100 firms pushing toward double digits, according to the Thomson Reuters Institute’s recently released Q1 2026 Law Firm Financial Index. These inputs would typically support strong overall performance.

Yet productivity declined slightly, falling to -0.4% after six months of positive growth. On its own, that change is modest. In context, however, it reflects a more interesting shift in how performance is being generated.

The key is understanding what productivity measures and what it does not. Law firms’ traditional measure of productivity is hours worked per lawyer, which tracks the average number of hours logged by a firm’s lawyers to give an estimate of efficiency. However, that traditionally has not incorporated pricing mostly because, historically, law firms have focused more on the hourly output of lawyers as the mark of success. This means firms were often not concerning themselves with whether the pattern is profitable, let alone taking into account factors like demand elasticity or automation’s impact on the equation.

This is changing, however. As more and more revenue growth is being driven by rate increases rather than increases in demand or hours per lawyer, the disconnect is being magnified. And this distinction helps explain why strong inputs are producing a more muted output and why understanding that relationship is vital for firm leaders to get an accurate picture of how large law firm economics are evolving.

The divergence between hours and value

To see that situation more clearly, it is necessary to move from activity-based metrics to value-based ones — and fees worked per lawyer (or what we’re calling value per lawyer) provides that view. Fees worked is a pre-realization revenue proxy, representing the total value a firm produces before billing and collections take over, then averaging it across lawyer headcount. This method accounts for scale, giving a cleaner read on efficiency than looking at just raw hours. Because fees worked per lawyer folds rates and hours into a single measure, it captures the value that the traditional productivity metrics leave out.

As shown in the chart below, the industry is experiencing a widening gap between the hours lawyers work and the value that their work generates even as demand has remained consistently positive and rate-driven growth has stayed strong across recent quarters. As a result, productivity has been more volatile and recently turned negative. At the same time, fees worked per lawyer (or full time equivalent) has continued to trend upward, indicating that value per lawyer is still increasing rapidly despite what the old metric might have historically implied.

That means that law firms are producing far more value per lawyer even though hours per lawyer have softened slightly. The factor magnifies once you consider what period firms are measuring against. The first quarter of 2025 was exceptionally strong, creating a high baseline that can subdue the current level of growth — against a “normal” year, law firm performance would be even greater.

While this is a historically recent phenomenon, it’s not one unique to 2026. Strong rate growth has often offset weaker productivity for the last couple of years. What makes the first quarter of this year more unique is that it no longer seems uniformly true across the market.

Where performance is beginning to diverge

The Q1 2026 data shows a clear separation in how firms of different sizes are translating demand and rates into value per lawyer. Among Am Law 100 firms, for example, strong rate growth remains the primary driver of revenue performance, which is being supported by disciplined headcount management that’s kept efficiency high. These firms have continued to push pricing while maintaining selectivity in hiring, allowing value per lawyer to remain resilient even as productivity softens.

The Am Law Second Hundred has embraced a different strategy. Firms in this segment are continuing to pursue growth through lateral hiring and increased capacity. This supports overall revenue but can dilute per-lawyer metrics as new lawyers ramp up. The result is softer value per lawyer despite the segment’s continued headcount expansion.

The most consequential shift is occurring in the Midsize law firm segment. Rate growth has slowed for Midsize firms, while those in other segments have maintained or exceeded prior pacing. At the same time, expenses are accelerating and are now outpacing overall fees worked growth. This creates a dynamic in which value per lawyer is still increasing, but it’s running closer to expenses.

What this all means for profitability

In the near term, there is no indication of a broad downturn. Value per lawyer continues to grow despite declines in hours per lawyer, and pricing remains strong, particularly at the top of the market. At the same time, however, the balance between value and cost is beginning to shift, most notably in the Midsize segment, where expenses are rising faster than revenue proxies.

Looking ahead, we will keep our eyes on value per lawyer, which is developing into a critical performance metric. If this metrics continues to strengthen as comparisons normalize, the softness in Q1 will likely prove temporary. If it remains constrained, particularly in segments already facing cost pressure, however, it may point to a more persistent challenge.

The broader takeaway reflected in the Q1 2026 LFFI data is that law firm performance is no longer defined primarily by the traditional measures such as hours per lawyer at the forefront without the context of rates. Indeed, this should no longer be given as much psychological weight as it was before the pandemic. In a market shaped increasingly by pricing power, the more important question for today’s law firm leaders is how much value each lawyer is generating and whether that value is keeping pace with the cost of delivering it.

You can download a full copy of the Thomson Reuters Institute’s Q1 2026 Law Firm Financial Index here