Certainly, 2020 has been a year of a digital transformation and acceleration to meet the challenges of the COVID-19 pandemic. By necessity and by design, financial service firms have implemented the roll-out of technology, often at speed, to enable business activities to continue as countries went into lockdown.

The applications that are covered by the term fintech are fast becoming part of financial services firms’ identity. And in a marketplace that is still maturing, the question is whether corporate governance and the culture of financial services firms have kept up to pace with this new tech.

To shed further light on this, Thomson Reuters Regulatory Intelligence has published its fifth annual survey report, Fintech, Regtech & the Role of Compliance in 2021, to more deeply explore these issues. This year’s survey results represent the views and experiences of more than 400 compliance and risk practitioners.

The survey found the adoption and implementation of technology has taken a huge step forward during the pandemic, despite the continuing budget challenges that firms face. Sector growth is expected to accelerate over the coming months and years, despite a general slowdown in new start-ups during 2020 due to the pandemic. Financial services firms, and their customers, are realizing value from their use of a variety of fintech solutions.

You can download a full copy of Thomson Reuters Regulatory Intelligence’s fifth annual survey report, Fintech, Regtech & the Role of Compliance in 2021, here.

Firms must be careful to deploy solutions on solid foundations, and this means getting the corporate governance right, the survey suggested. Further, one-quarter of respondents reported that boards and risk and compliance functions needed to be more involved in fintech solutions — an perceived absence of appropriate skill sets may be one reason for this lack of involvement.

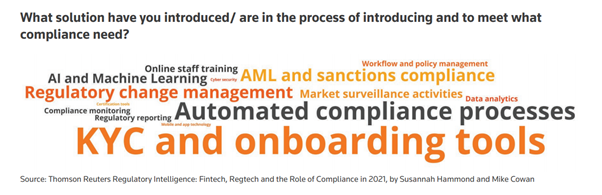

The area of fintech most relevant to compliance officers’ responsibilities is probably regtech. Regulatory processes are increasingly being managed through technology. The regtech marketplace can be split into a number of areas: risk and compliance management, identity management, regulatory reporting, fraud management, and regulatory intelligence. Regtech applications continue to provide popular, embedded solutions for firms in areas such as compliance monitoring, financial crime, AML/CTF, sanctions, and regulatory reporting. Budgets were predicted to increase, with a mix of in-house and external solutions being the most frequent option selected by respondents.

Fintech presents extensive opportunities for firms in future. The presence of bigtech and the potential of artificial intelligence (AI) will enable firms to increase customer-focused initiatives such as financial inclusion. To be able to exploit these areas firms need to overcome a number of challenges: budgetary limitations, weaknesses in corporate skill sets, the limitations of existing IT infrastructure, and the developing regulatory picture. They must also ensure they have an appropriate corporate governance framework capable of managing the deployment of fintech systems.

Watch a video interview with Senior Regulatory Intelligence Expert and co-author of the report, Mike Cowan, on the key findings of the report.

Concern about budgetary limitations and pressures are a natural consequence of business and economic disruption, but firms will need to consider very carefully any cuts which might affect risk and compliance functionality. Although boards and risk and compliance functions are becoming more involved with fintech onboarding, and firms have begun to invest in specialist skill sets, further investment may still be necessary.

Understanding your fintech

Firms need an in-depth understanding of any technological solution, and of the limitations of the inputs and outputs. That understanding is dependent, at least in part, on the skill sets of those seeking to use the outputs. Despite potential future budget constraints, firms must continue to invest in personnel with those skill sets at all levels if they are to make the most of digital transformation.

The maintenance and development of these skill sets is also important in terms of individual accountability. Chief executives, board members, and other senior individuals will be held accountable for failures in technology and should therefore ensure that their technological skill sets too remain up-to-date and relevant.

Regulators have shown substantial forbearance in their response to the pandemic, but that patience is not infinite. Firms should be aware that the delivery of good customer outcomes is not negotiable, and that regulators and politicians alike will not tolerate any senior managers who fail to take the expected reasonable steps with regard to skill sets, systems upgrades, and cyber-resilience.

The business impact of the pandemic has made firms think about what regtech can, cannot, or should not do for them. They will increasingly need to flex their approach to better deal with limited budgets and understand that there is no ‘one solution fits all’ option.

There has been a huge leap forward in the adoption of technology and the associated digital transformation, but there is still much that technology could deliver. Improved efficiency and speed are essential if financial service firms are going to be able to deliver more with less and achieve the required cost savings. However, firms should be careful not to sacrifice mature corporate governance in their haste to exploit the opportunities that fintech presents.

You can find out more about Thomson Reuters Regulatory Intelligence here.