For corporate tax directors and CFOs, navigating the post-OBBBA landscape does not require a tweak, but rather a mandate to rebuild how to model, plan, and communicate tax outcomes to leadership

Key takeaways:

-

-

-

Your post-OBBBA forecasts should look different — If the tax department doesn’t own the OBBBA model, someone else will own the OBBBA story.

-

-

-

-

-

Rely on your department’s inner strengths — It’s governance and analysis — not tools — that get you into the strategy room.

-

Factor in the conflict in the Middle East — The Iran war risk belongs in your tax model, not just in your CFO’s macro deck.

-

-

The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, enacted large business tax cuts, most notably by providing permanent full expensing of many forms of investment. Under the previous major corporate tax legislation, 2017’s Tax Cuts and Jobs Act (TCJA), bonus depreciation was scheduled for gradual phase-out following 2023. The OBBBA restored that expensing 100% retroactively for assets acquired from mid-January 2025 onwards.

The after-tax cost of new machinery, fleets, and equipment has effectively fallen by around 21%, designed to encourage immediate capital outlays by allowing businesses to write off these expenses in the year they are incurred rather than amortizing them over five years.

For corporate tax departments, that’s not a disclosure footnote — that’s your capital plan.

Capital-intensive corporations will see tax burdens reduced through permanent rate extensions, depreciation adjustments, and expansion of the state and local tax (SALT) deduction cap — but only if your models are built to capture the timing and location of investment, the mix of debt compared to equity, and where your organization books its next dollar of income.

Not surprisingly, most corporate tax departments aren’t there yet. They’re still recalculating last year, plus a few adjustments. That’s glorified compliance, not modeling.

A standout tax department doesn’t ask, What’s the OBBBA impact? Rather, it asks, Which version of OBBBA do we choose for this business? — and it has the models to back it up.

From spreadsheet heroics to controlled modeling

For many organizations, tax modeling still means creating a massive spreadsheet that only one director truly understands. The spreadsheet gets pulled out for budget season, rebuilt under pressure, and quietly retired until next year. That’s a single point of failure, not a process.

And after OBBBA, continuing that practice is dangerous. One wrong assumption on expensing or interest limitation can move cash tax by millions of dollars and blindside the Finance Department.

Here’s what disciplined modeling looks like in practice:

-

-

- Create a unified model — Build one integrated model that the whole team can use or accept that your department is choosing to fly blind.

- Use the same assumptions — Standardize the levers that matter most (such as capex timing, financing mix, jurisdiction, and incentives) and make sure every scenario runs off the same assumptions.

- Conduct modeling reviews — Treat major OBBBA-driven decisions (such as large capex, funding shifts, supply-chain redesign) as tax deals that must go through a modeling review before they’re greenlit.

- Document your assumptions explicitly — Under permanent full expensing, the difference between a well-supported assumption and a poorly documented one isn’t just an audit risk, rather it’s a credibility problem with your CFO.

-

It’s also important to remember that in a post-OBBBA world, this level of disciplined modeling is not technology transformation — it’s basic survival.

Governance: Where leaders quietly win or loudly fail

The differentiator isn’t which corporate tax department has the fanciest tool — it’s which one has the cleanest governance. And the data is unambiguous: More than half (55%) of tax departments are still in the reactive phase of their technological development, stuck with five capex models circulating with five discount rates and the tax team arriving late to the planning meeting.

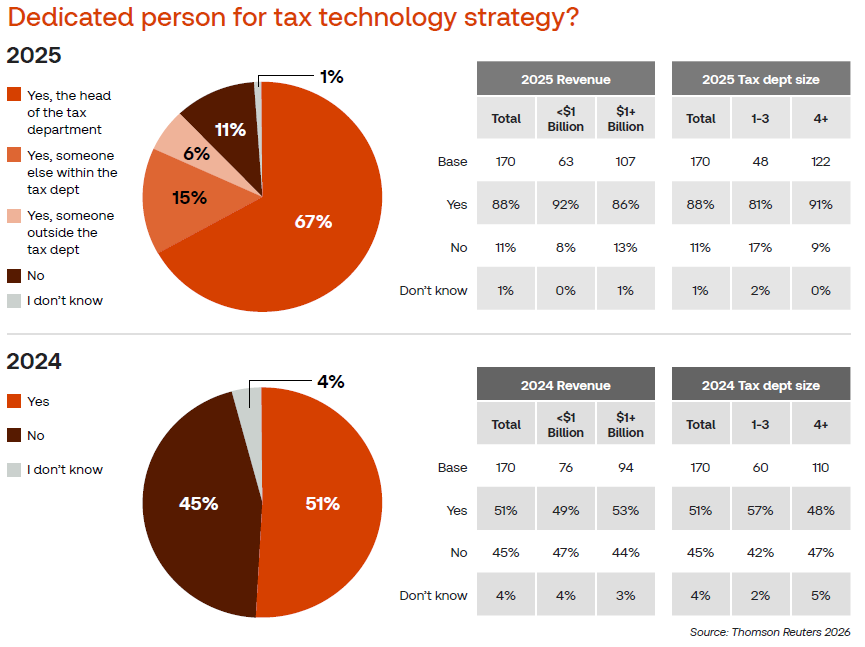

Those tax departments that are breaking out of that pattern share one trait: They put someone formally in charge. In the Thomson Reuters Institute’s recent 2026 Corporate Tax Department Technology Report, a large portion (88%) of survey respondents said their company had appointed a person to lead the tax department’s technology strategy. That number jumped a whopping 37 percentage points, from 51%, from the previous year’s survey. That single structural move separates those departments with a governance model from those that simply hold a governance conversation every budget cycle and forget about it.

Clearly, this type of ownership drives results. Two-thirds of those surveyed agreed that their company’s investment in technology has enabled a shift from routine, reactive work to more strategic, proactive, higher-value work.

Under OBBBA, the kind of governance isn’t housekeeping. It’s how you get invited into strategy discussions instead of having to clean up after things go awry.

Why your OBBBA win may not feel like a win

On paper, the tax changes embedded in the OBBBA look generous. In practice, your effective tax benefit is colliding with something you don’t control.

When the war on Iran began, all shipping through the Strait of Hormuz was effectively halted, removing roughly one-fifth of the world’s oil and gas supply from the market. Fuel prices throughout the world spiked and are likely to remain elevated as long as conflict persists.

With oil prices hovering around $100 a barrel, there are concerns that resulting higher gasoline prices will wipe out the benefits of higher tax refunds this year for most Americans. If those benefits, arising from Trump’s 2025 tax cuts, are erased for the average American, only the top 30% of taxpayers will still seeing a net gain.

For corporate planning purposes, the parallel dynamic is real: The topline OBBBA benefit is being eroded by higher fuel, freight, and financing costs across the business and its supply chain.

Inflationary pressures are being driven by higher energy prices tied to the Iran war, and the conflict’s impact on a wide range of goods and services is likely to last for months — with experts saying even a ceasefire is unlikely to immediately ease global energy shortages.

A serious corporate tax department doesn’t handwave these concerns away. It takes three actions:

-

-

- Run a war-extended scenario — The scenario should show exactly how sustained higher energy costs and borrowing rates change the payoff from accelerated expensing and leverage — with specific numbers, not just directional commentary.

- Share your forecasts internally — Put your monthly or quarterly cash-tax forecasts on the table for Finance to see, so that it can manage liquidity rather than hope the annual plan holds.

- Force the hard conversation — Ask the tough question: At today’s rates and fuel costs, the after-tax return on this project is X. Are we still in? That question should come from the tax team now, not from the finance team six months later.

-

Clearly, the daily fluctuations in oil prices matter less than monthly and quarterly averages — and volatility will likely remain elevated given the absence of a clear timeline for the end of the war. That’s exactly the kind of sustained uncertainty that belongs front and center in your scenario set, not in a footnote.

The bottom line

The OBBBA gives corporate tax departments a genuine opportunity to move from being simply a compliance function to becoming more of a strategic advisor. Permanent full expensing, richer cost recovery, and more flexible interest rules can create real levers to add value, but only for those organizations that model them rigorously, govern them cleanly, and stress-test them against the macro environment their business actually faces today.

Indeed, the Iran war is a live test of that readiness. The corporate tax departments that show up with modeled scenarios, cash-tax forecasts, and a clear point of view on after-tax returns will earn a seat at the strategy table. The ones that show up with caveats will be asked to leave it.

You can download a full copy of the Thomson Reuters Institute’s recent 2026 Corporate Tax Department Technology Report here