ViDA is bringing widespread changes to EU businesses, especially around compliance, business operations, and technology systems — however, the question is, will they be ready?

Key takeaways:

-

-

-

Understanding is not preparation — Most EU businesses are aware of — but not necessarily prepared for — the sweeping changes that ViDA is bringing.

-

Few businesses have a solid transition plan in place — Only 22% of tax and finance professionals surveyed say their organization has a formal, funded ViDA transition program in place.

-

Some key requirements are already changing — With e-invoice and real-time reporting requirements already shifting, businesses are in danger of falling behind, risking business continuity and non-compliance.

-

-

The European Union’s reforms around its value added tax (VAT) — known as VAT in the Digital Age (ViDA) — represent the most significant shift in tax compliance for businesses operating in the EU in a generation. ViDA is more than merely another new compliance requirement or technology upgrade. Indeed, many organizations will need to modernize their entire invoicing and tax reporting systems to get into compliance.

Jump to ↓

The new compliance horizon: 2026 ViDA Readiness Report

While ViDA’s EU-wide mandates for cross-border e-invoicing and digital reporting take effect in 2030, the pressure on organizations is already mounting as individual EU member states roll out a patchwork of national requirements.

Digging deeper on this, a new report from the Thomson Reuters Institute, The new compliance horizon: 2026 ViDA Readiness Report, reveals a striking paradox in how EU tax and finance professionals are preparing for this overhaul. While awareness is nearly universal, a significant gap remains between awareness of ViDA and tax teams’ readiness for its changes.

Indeed, 86% of EU tax and finance professionals say they are familiar with ViDA; however, a deeper look reveals that only 35% possess a detailed understanding of the specific requirements of the regulatory reform package. This creates a state of “comfortable uncertainty,” in which high initial confidence can often mask a lack of preparation for the massive technological and operational changes ahead.

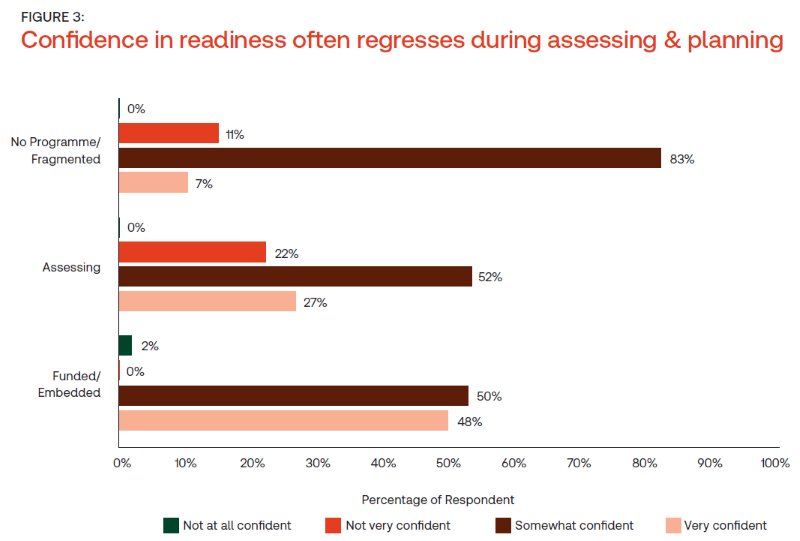

Riding the “Confidence Curve”

One of the most compelling findings from the report is the “Confidence Curve” that shows how many organizations often start their journey with high levels of optimism. In fact, even among respondents who say their organization does not yet have a transition program in place or has one that is fragmented across EU member states, 90% say they feel confident in their organization’s ability to achieve ViDA compliance.

However, the Confidence Curve shows that confidence often regresses during the assessment and planning phase. As teams begin to uncover the complexities of new multi-jurisdictional compliance and real-time reporting requirements, the percentage of respondents who say they are “not very confident” doubles. It is only after a program is funded and embedded into digital transformation strategies that confidence strongly rebounds.

You can learn more about how ViDA readiness can help your organization here

Despite the high stakes, the majority of organizations are still finding their footing, the report shows. Unfortunately, more than three-quarters (78%) of respondents say their organization has no formal, funded ViDA transition program with central governance in place, meaning that they’re working in a fragmented country-by-country fashion or are still in the assessment stage.

These delays are risky Many EU member states have already begun rolling out e-invoicing mandates. That leaves those organizations without programs in place at greater risk of falling further behind.

The ViDA-enabled opportunity

Despite the massive changes in VAT requirements that ViDA brings, the reform package also offers corporate tax functions a tremendous opportunity to elevate themselves from a cost center to a strategic business partner. As the report outlines, taking that path forward requires a cross-functional commitment across numerous corporate functions, including tax, finance, IT, and legal departments.

Yet, those organizations that move beyond providing the “minimum viable compliance” and instead take the opportunity to invest in standardized data and central governance will be better positioned to turn these regulatory mandates into a compliance advantage for the tax function and a competitive advantage for the organization going forward.

You can download

a full copy of the Thomson Reuters Institute’s The new compliance horizon: 2026 ViDA Readiness Report here