For those tax & accounting firms and law firms that want to get an edge on gaining advisory service work from clients, having their own internal ESG strategy may be the way to go

Tax & accounting firms are in a good position to gain a competitive advantage in advisory work in the environmental, social & governance (ESG) area because firms have the expertise to dominate in both the accounting and audit areas that are at the center of certain new regulations. In addition, tax & accounting firms are more likely to focus on financially material issues — including data governance management — given their IT governance expertise.

At the same time, both tax & accounting and legal services providers have a ways to go in executing their own internal ESG strategies, even as client demand for this information through the procurement process is exploding. Indeed, I constantly have to remind firms that their own house has to be in order, because one of the first questions a prospective client is going to ask is, “What are you doing for ESG within your own firm, if you are here to advise me?”

The good news is that tax & accounting and law firms already have experience to lean on as they create a holistic ESG strategy. Indeed, clients have been asking for firms’ demographic data around diversity, equity & inclusion (DEI) for at least the last five years. In fact, DEI information is a major portion of the social or S part of ESG; and the expertise among accountants and CPAs involves many areas of the governance or G, it’s easy to see how the creation of a comprehensive ESG strategy is not as daunting as it seems.

Areas of priority to create a holistic ESG strategy

The two most urgent areas of focus for both law firms and tax & accounting firms in this area are: i) formalizing a material assessment, and ii) calculating greenhouse gas emissions (also referred to as carbon emissions) when they are assessing their gaps in client service offerings and consolidating existing activities around ESG issues into a complete strategy.

Identifying material issues — A materiality assessment exercise involves collecting feedback on material issues across all a firm’s stakeholders — including future, current, and past partners; associates and business services staff; clients; charitable organizations; and suppliers. Going through this process helps the firm identify the issues of greatest importance that should be prioritized for the firm’s own ESG strategy.

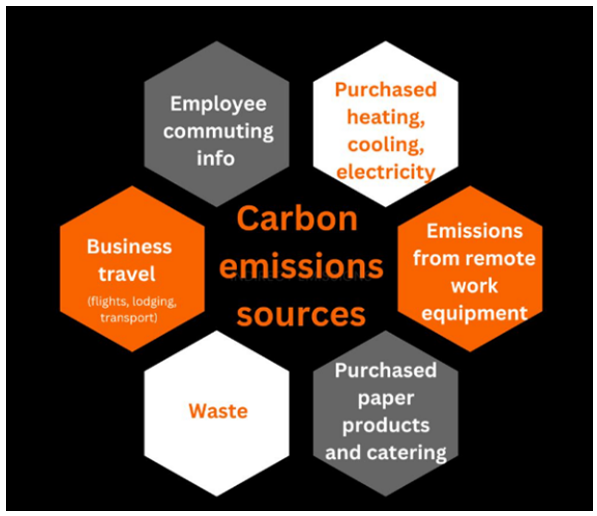

Carbon emissions calculations — Often, the biggest area of priority for tax & accounting and legal services providers is the environmental or E part of the equation. More specifically, calculating carbon emissions is the most urgent task, and it does involve some effort. The graphic below shows the typical sources of carbon emissions for tax & accounting and law firms.

Challenges may slow positioning

The process of creating and executing an ESG strategy does not come without its challenges, of course. One of the main challenges that I see often as part of the governance part is the partnership business model. Partnerships in general are very lax when it comes to governance because often, partnership relationships get in the way of the creation and execution of proper procedures and policies.

Another barrier to progress is that the necessity to create an internal strategy may not seem urgent to internal leaders because in the grand scheme of things, the carbon footprint of accounting and legal firms is small when compared to other industries, such as transportation companies and manufacturing.

To get around this perception, I often highlight that the expectations of clients — especially those who use the greenhouse gas protocol, which is the go-to methodology for companies in calculating greenhouse gas emissions — is that all businesses should seek to reduce their fair share of carbon. For example, an accounting firm and a manufacturing company are expected to reduce their carbon footprints by 90% in order to get to net zero, no matter their baseline — 90% is still 90%.

Challenges around varying preferences of generations among employees and the political environment in the United States are two additional barriers to progress that firms currently are facing. Younger workers may see ESG and reducing a firm’s carbon footprint as a huge business opportunity and a great goal to pursue as part of the firm’s larger commitment to healthy communities and habitats. The older worker cohort, by comparison, may lack the same enthusiasm.

Regarding the political environment, all firms should be cautious in the language that is used to pursue or explain ESG goals, making sure the goals are perceived as a framework to consider business risk and opportunity — not positioned as an ideology. A year ago, this was not a major concern.

On the horizon

The momentum for ESG will only accelerate despite the current headwinds. Indeed, client expectations about firms’ ESG strategies are currently much more strident in the United Kingdom and European Union because of pending disclosure requirements. For example, a client has to report on the carbon footprints of its suppliers, which is referred to as Scope 3, to meet regulatory requirements in certain jurisdictions.

While the U.S. Securities and Exchange Commission’s proposed rules to require companies to collect and report their suppliers’ carbon information are not yet finalized, disclosure of Scope 3 carbon emissions is already a mainstream expectation of many stakeholders. Indeed, the U.S. rules are almost irrelevant for virtually all global companies because such disclosure is already required in the E.U. and the U.K. For example, law firms tax & accounting firms that advise or provide services to multinational clients will be required to calculate and share their own carbon footprint as a supplier to these major public companies.

The accounting and legal professions are in a unique position to do something positive about the challenges we are facing in society — everything from the climate problem to governance issues to data collection, data security, and more. These are the professionals who have the skills, the talent, the expertise, and the connections to address these problems; but they have to walk their talk. And that means focusing on creating and executing their own internal ESG strategy with just as much enthusiasm as they put into going after the tremendous business opportunities of ESG advisory work.