With more than 2.5 million Suspicious Activity Reports (SARs) being filed through August 2023, filers have been able to alert regulators to something suspicious or possibly illegal in transactions with customers

Through 2023, financial institutions had to grapple with the increase in post-pandemic fraud workloads, facing mounting public and private pressure around reporting requirements, with an enhanced focus on combatting scams, elder financial exploitation, and humanitarian issues.

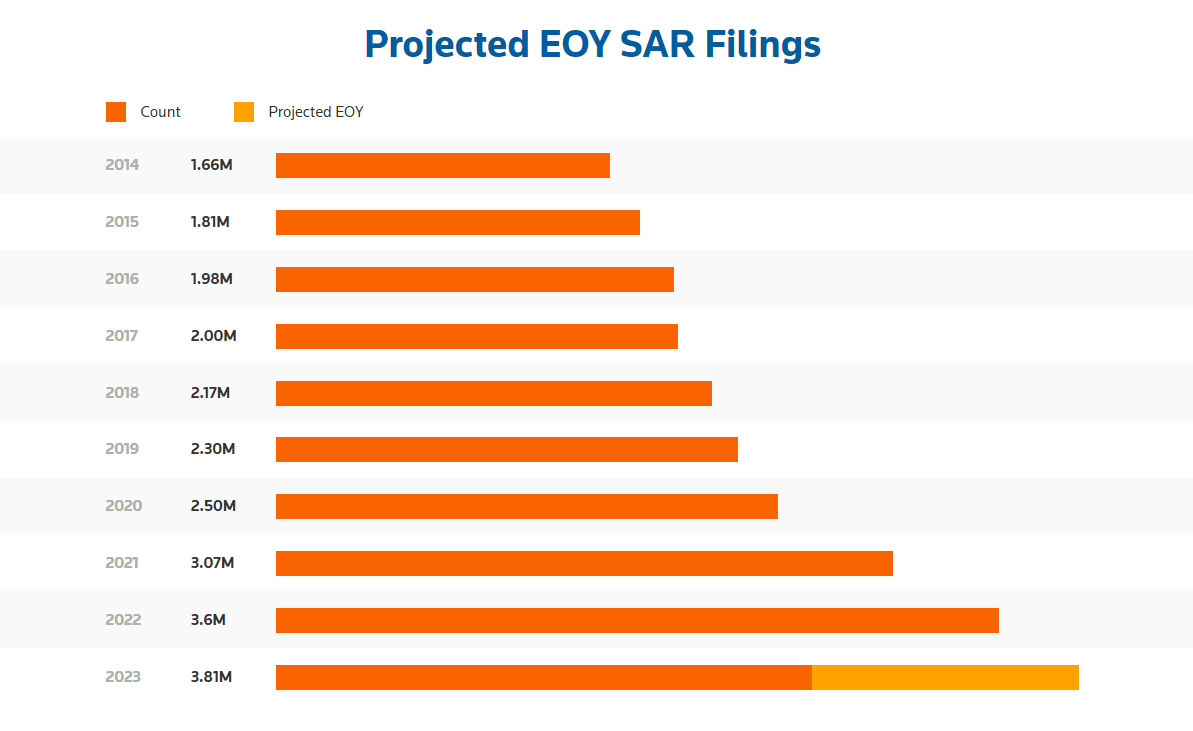

According to the latest statistical data from the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN), a staggering 2,540,437 Suspicious Activity Reports (SARs) have been recorded through August 2023. Filing SARs allow financial institutions and other regulated organizations to alert regulators as to something the filer sees as suspicious or possibly illegal in transactions with customers. SAR filings are seen as a strong weapon in the fight against money laundering and other illicit schemes.

This year’s SAR filing pace aligns with the historical year-over-year growth of about 4% to 5%, a consistency observed before the significant surges in 2021 and 2022. If this trend continues, financial institutions and other regulated organizations are on track to file around 3.8 million SARs in 2023, slightly surpassing the 3.75 million SARs predicted in the Thomson Reuters SAR Special Report published earlier this year.

Uncovering trends in the SAR filing data

Certainly, fraud is now a focus for every financial intelligence unit leader. Confidence scams, job scams, check fraud, mail theft, friendly fraud, account takeover, and identity theft have all witnessed substantial increases in SAR filing activity and consumer losses since 2019.

International organized crime, leveraging compromised or stolen personal identifiable information and bank accounts, is fueling a major rise in bank fraud and consumer losses. As we analyze the data through August 2023, all indicators suggest these challenges are here to stay.

Identity fraud and forgeries

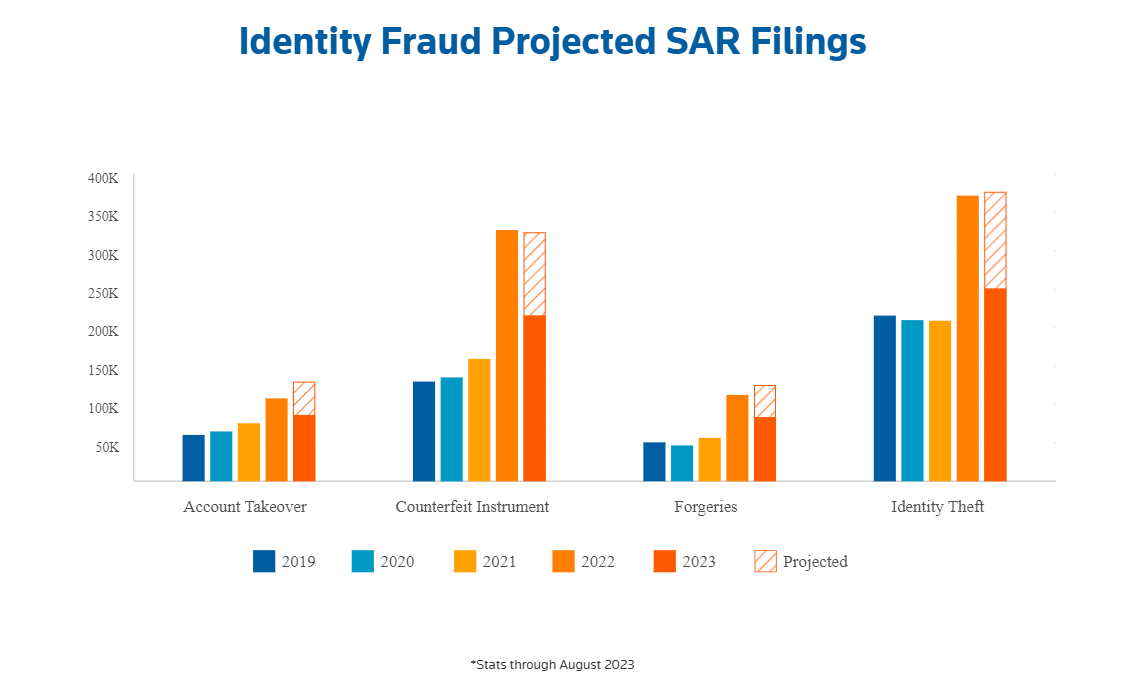

Since 2019, we’ve witnessed a substantial increase in identity fraud and forgery-related activities, with account takeovers, counterfeit instruments, forgeries, and identity theft standing out. Notably, SAR filings related to account takeovers are on track to surpass 129,000 in 2023, up from 108,000 in 2022, highlighting the escalating nature of this issue.

On a somewhat more optimistic note, SARs for counterfeit instruments are showing a slight year-over-year decrease from the significantly elevated numbers seen in 2022; however, filings still are significantly above pre-2021 numbers. Additionally, forgeries and account takeover filings are expected to slightly increase by the end of 2023, indicating a continued struggle against these types of fraudulent activities.

A key driver of identity crime and forgeries is the widespread availability of personal identity data. Indeed, data from the Identity Theft Resource Center reveals that more than 66 million victims of identity data breaches were identified in the third quarter of 2023 alone. Among the most frequently compromised pieces of personal information were full names, dates of birth, addresses, and Social Security numbers, underscoring the critical need for heightened security and awareness among consumers and institutions.

Elder financial exploitation

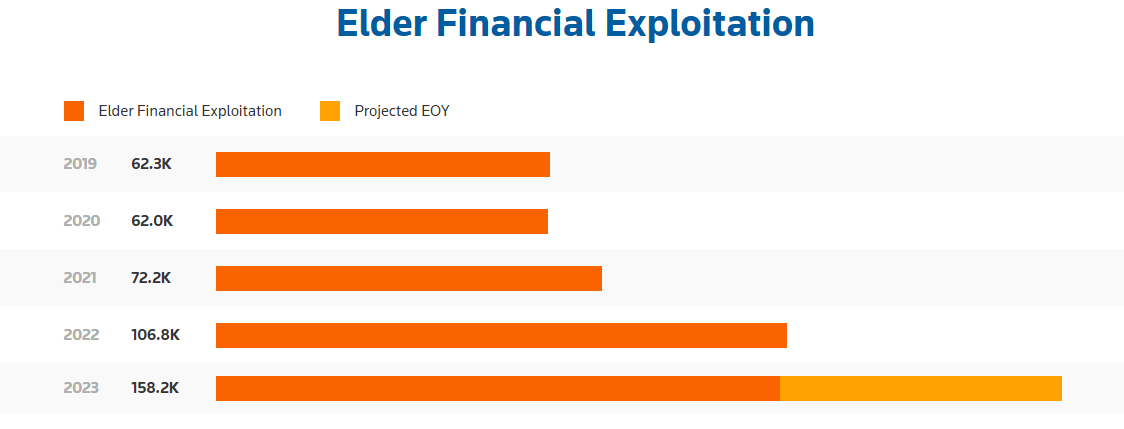

Elder financial exploitation has escalated dramatically, marking it as a major concern in the financial sector this year. By the end of August, institutions had already filed more than 105,000 SARs related to the financial exploitation of senior citizens, nearly matching the number of reports filed in all of 2022. This is a substantial increase from the roughly 62,000 filings reported annually in 2019 and 2020, and a noticeable uptick from the 72,000 in 2021. The 2022 jump to 106,000 SARs alone illustrates a concerning 47% increase.

As indicated in the chart below, the current elder financial exploitation-related SAR filing rate means we could see upwards of 158,000 SARs filed by year’s end. Back-to-back annual increases amounting to double the total number of SARs filed in two years is significant. A portion of this increase likely relates to increased education and awareness within reporting entities; however, the major uptick in elder financial exploitation-related filings strongly implies that the vulnerable elderly population is being victimized by a large increase in scam and fraud activity.

A recent report by AARP (formerly the American Association of Retired Persons) sheds light on the magnitude of this issue, indicating that older Americans lose an estimated $28.3 billion annually to targeted scams. Significantly, a major portion of these losses remains unreported by victims, suggesting the actual extent of elder financial exploitation is likely much higher than what the SARs data reveals.

These stats should serve as a call to action to protect an especially vulnerable population. Understanding that this trend is growing at such an alarming rate, financial crime professionals in both the public and private sector ideally should be taking major steps to combat fraud and shield our elderly population from such financial exploitation.

Conclusion

Conclusion

Heading into the end of 2023, the increase in Suspicious Activity Reports across various sectors – particularly identity fraud, forgeries, and elder financial exploitation – calls for immediate and unified action. The latest fraud trends show that the pressure the financial system has been experiencing the last few years has not lost steam and does not appear to be reverting to pre-pandemic levels.

Based on this information, there is a critical need for financial institutions, regulatory bodies, and the wider community to join forces, innovate, and strengthen all their defenses against fraud, scams, and financial crimes. However, as fraud continues to move into the next technological age, there is not one simple solution to combatting it.

Good data, collaboration, and advanced technology should all be leveraged to safeguard the financial system. In this case, the data speaks volumes, and our financial system needs to be ready to prevent, detect, and investigate fraud in real time.