Just like May flowers follow April showers, Ponzi schemes will follow a market crisis, and financial institutions need to be on guard for the coming wave

The last example of this phenomenon was the 2008 financial crisis and ensuing market crash. In 2008, there were 40 Ponzi schemes valued at more than $1 million uncovered in the U.S. In 2009, there were more than 100.

During the 2008-‘09 Ponzi scheme surge, it wasn’t just Mom and Pop investors who were lulled into the schemes, large investment advisers, broker-dealers, and banks were eventually swept up in investor litigation and regulatory enforcement actions. We can expect to see the same situation play out again in the coming months and years.

Why Market Crises Expose Ponzi Schemes

Rising markets can mask Ponzi schemes — often, it is easy to raise funds, and few investors are asking for redemptions. When the stock market crashes and investors simultaneously try to cash out of a previously unknown fraudulent investments, the schemes quickly collapse due to the ensuing liquidity crisis. For instance, fraudsters will have a difficult time raising new money from investors during a market crash, which is how in “normal” times they keep the schemes running.

The list below shows the principles used to keep a Ponzi scheme going during normal market conditions.

Ponzi Scheme Longevity Rules:

-

-

- Recruit new money — New money is key to maintaining a scheme for an extended period.

- Encourage “re-investment” of income — The less income the schemer pays out, the longer the scheme will last.

- Discourage redemptions — Paying out principal to investors at a high rate will crash the scheme quickly. Therefore, schemers may institute a large penalty for early redemptions or promise an even higher Rate of Return if the principal is reinvested instead of withdrawn.

- Make big promises — The Rate of Return promised should be higher than alternatives, but not so high that paying out income will quickly bankrupt the scheme.

- Moderate the amount stolen each year — If the fraudster steals a smaller amount each year, the scheme will last longer, and he will likely be able to steal more money overall.

-

Recognizing the Signs that a Ponzi Scheme Is Imploding

Ponzi schemers may also turn to loan fraud in order to keep the scheme going when new investor funds are not available. Federal depository institutions have filed Ponzi-related Suspicious Activity Reports (SARs) that indicated the subject was a borrower that had turned to Home Equity Loans and Residential Mortgages to prop up their schemes, as reported by the SARs Product category.

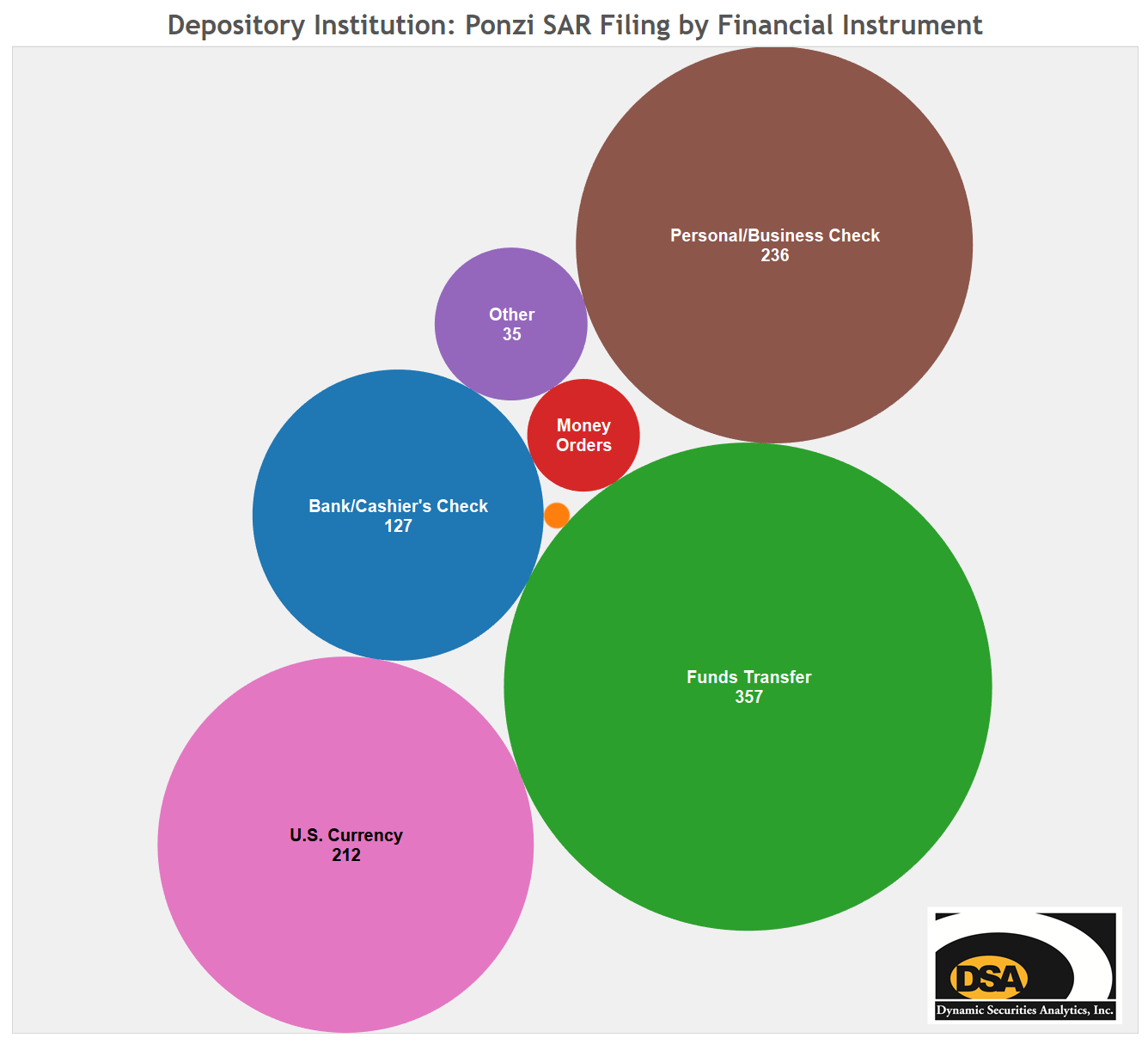

Another way a fraudster will try to keep the scheme afloat is to buy more time by engaging in check-kiting. Checks have a float time that can be manipulated to inflate a bank balance at one bank and allow a schemer to make fake “interest” payments to investors. Banks reported Bank/Cashier Checks and Personal/Business Checks (combined) as the leading instrument type involved in suspected Ponzi schemes.

Here is the playbook of a Ponzi schemer trying to postpone being discovered:

-

-

- “Temporarily” freeze redemptions;

- Stop paying dividends;

- Shuffle money between bank accounts to artificially inflate account values; and

- Stop answering investors’ calls.

-

A financial institution may be tipped off to a previously undetected Ponzi scheme imploding at their institution when they receive calls from customers (or the schemer’s customers) who are unable to redeem their investment or who stopped receiving income disbursements.

Financial institutions should be alert to these signs and utilize know your customer care and customer due diligence to identify collapsing Ponzi schemes.