“Fairy tales are more than true: not because they tell us that dragons exist, but because they tell us that dragons can be beaten.”

— Neil Gaiman, Coraline

About a year ago, Thomson Reuters released a new version of its Dynamic Law Firms Report, which sought to examine the top quartile of law firms in its Peer Monitor program in order to identify which aspects had made some firms more successful than their peers. We’ve been watching these firms throughout the pandemic, and this coming spring we will release another full report.

Out of curiosity, we checked in on how these firms are doing midway through 2021. What we have found is very much like a fairytale, though not necessarily one with a happy ending for everyone.

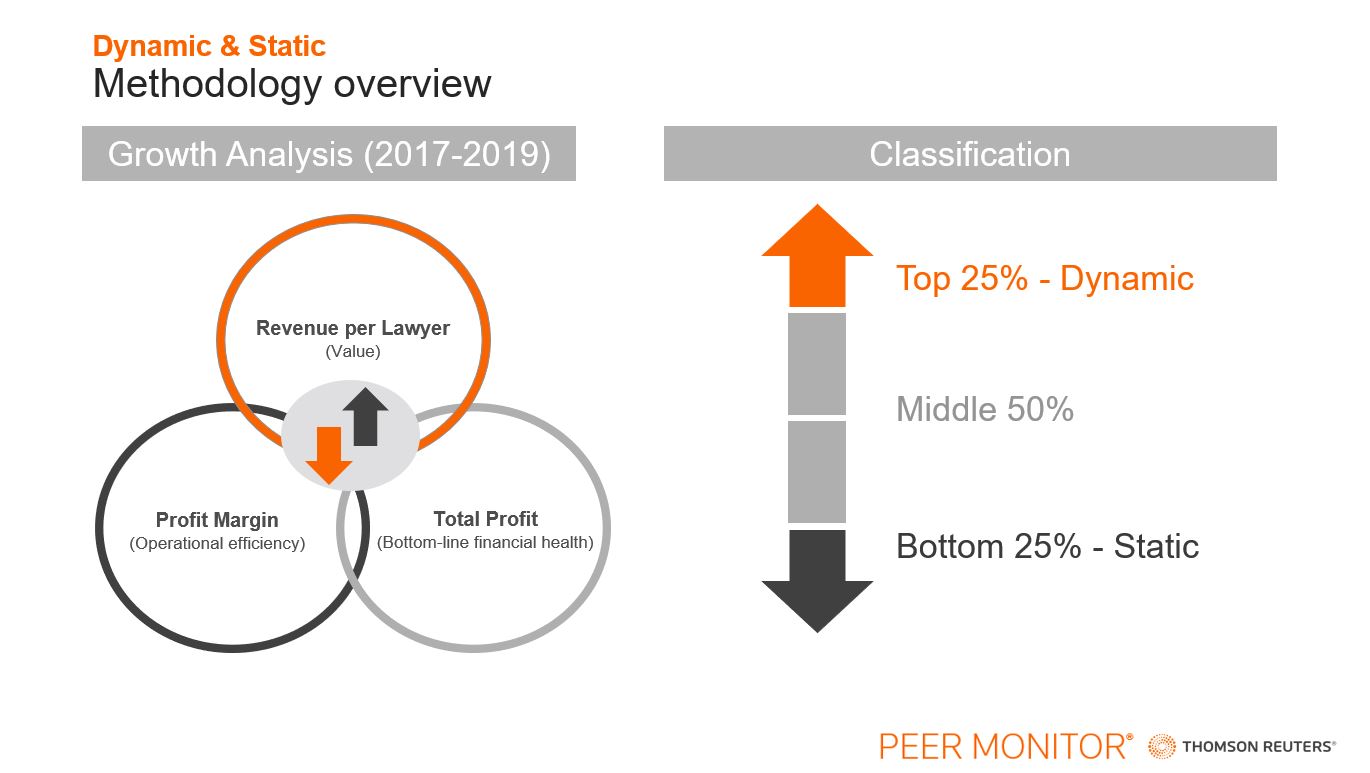

The Dynamic Law Firms Report ranks all of the firms within the Peer Monitor program according to a weighted index of three key growth statistics: revenue per lawyer (RPL), total profit, and profit margin. The top 25% of law firms on this list became the Dynamic subset. In contrast, the bottom quartile of firms was identified as Static firms. So, what has happened to these firms over the last few months?

Act I

In early 2020, the threat of the pandemic appeared to be a black dragon which threatened to swallow law firms whole along with the rest of the economy. Firms found themselves thrust from crisis to crisis. Legal demand seemed set to plummet into an abyss; yet by the end of the summer of 2021, our all-firms average shows most key performance indicators (KPI) are positive, law firms are hiring, and profit margins are up.

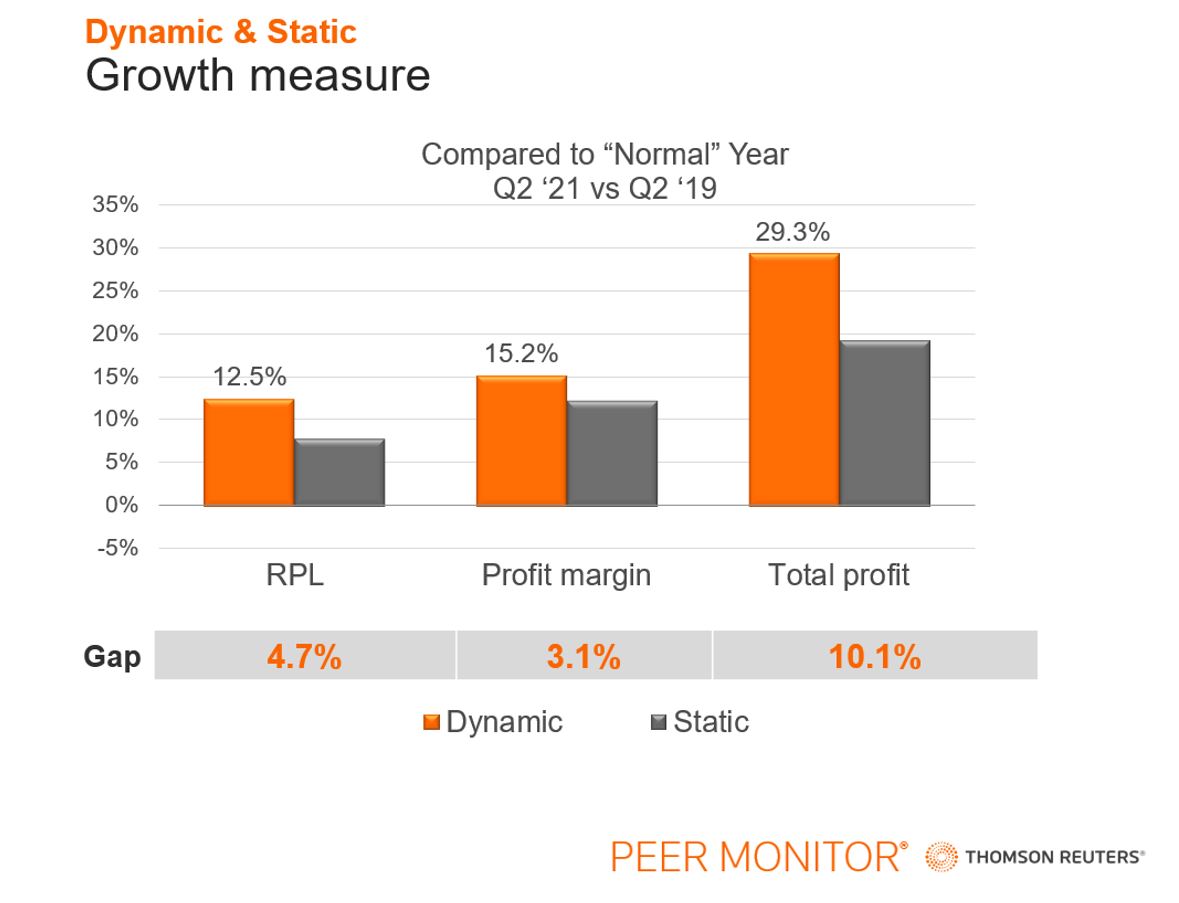

Comparing Q2 of 2021 to Q2 of 2019 (the last normal year and a good benchmark for actual growth), both Dynamic and Static firms had solid increases in their baseline metrics. Dynamic firms grew their RPL by 12.5% on average — a development achieved through two cumulative years of rate increases and substantial demand growth in corporate practices. These firms also managed to achieve a 15.2% growth in their profit margins over 2019 levels, the result of substantial cuts in expenses and cost savings from transitioning to a work-from-home model.

You can see the digital version of the 2022 Dynamic Law Firms report here.

Even Static firms achieved 7.8% growth in RPL and a corresponding 12.1% growth in their profit margin. The crowning achievement still belongs to Dynamic firms, whose cumulative deeds combine to achieve 29.3% growth in total profits — 10.1 percentage points higher than Static firms’ gains.

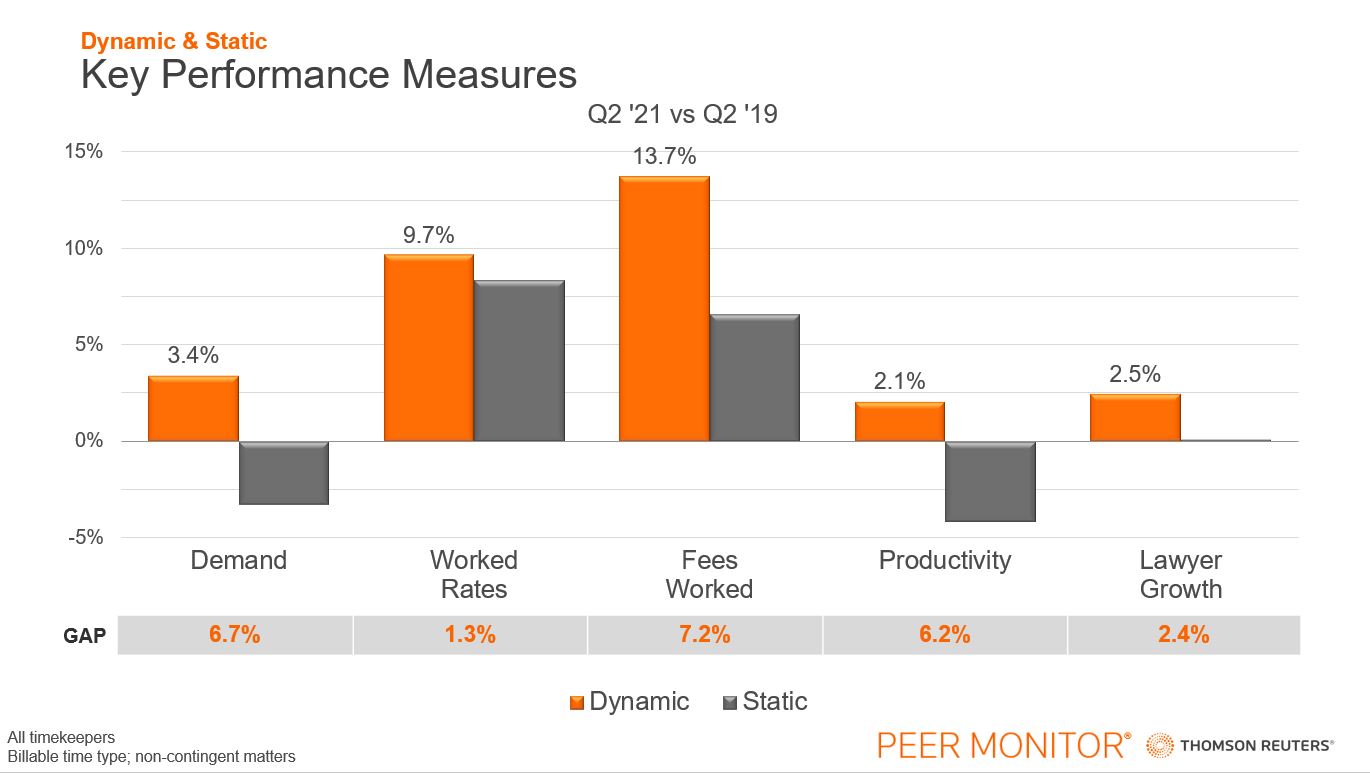

By the end of Q2 2021, all of Dynamic firms’ KPIs were up when measured against Q2 2019. Worked rates had grown almost 10% (with two years of rate increases included in this figure), and fees worked were up 13.7%.

Dynamic law firms also seem to be looking to continue their success. In a hot labor market, these law firms are making big moves, growing their headcount when new blood is hard (and expensive) to find. In nearly every metric we’re tracking, Dynamic firms are either maintaining their lead over their competition or pulling further ahead. Corporate and real estate practices in particular have seen so much dominance by Dynamic firms that we will soon publish a separate article on their performance.

It’s a fairytale ending. The dragon appears to have been slain, riches rain upon the heroes, everyone lives happily ever after… except this story may not be finished.

Act II

In many classic fairytales, the story does not end when things appear to be wrapping up. There is a final twist, a final challenge. In our case, the dragon may only be mostly dead. To see this, you only need only to dive more deeply into the Static firms.

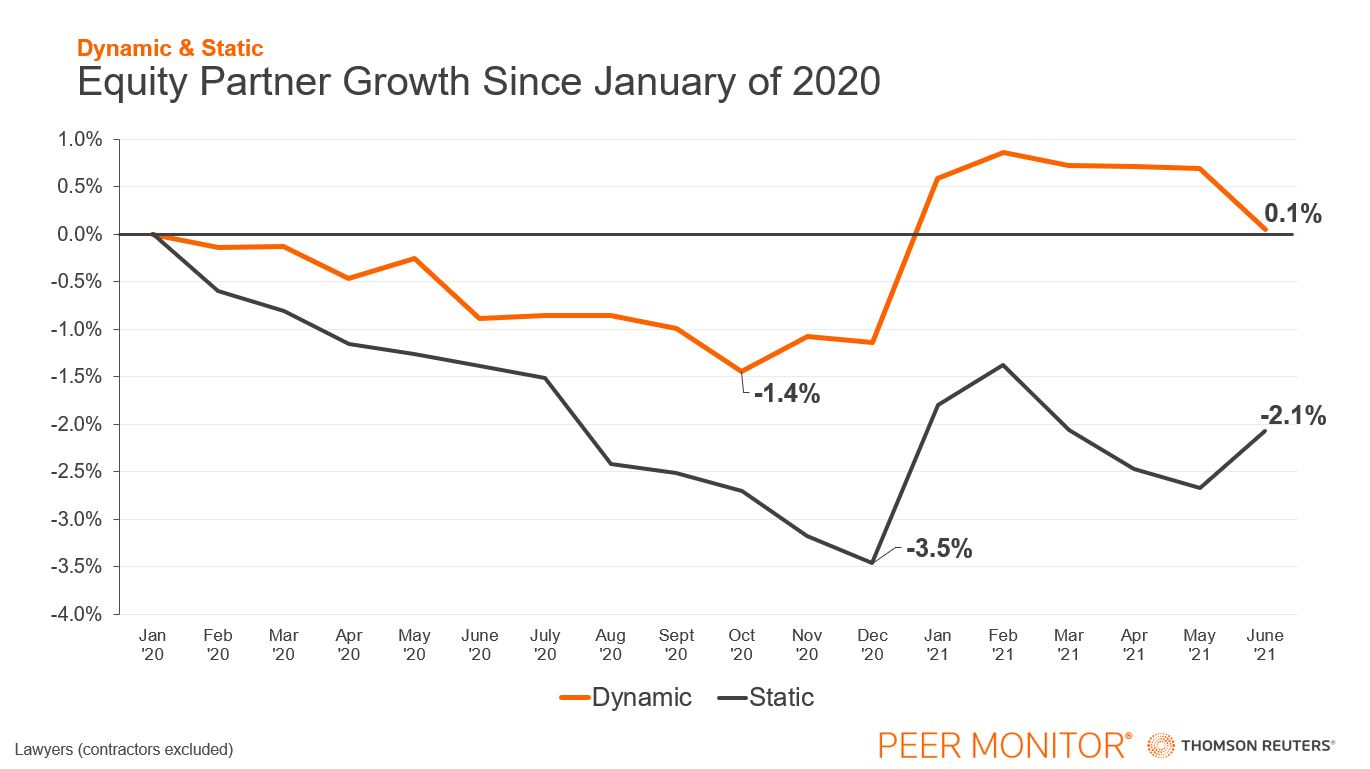

The above graph measures full-time equivalent (FTE) growth from January 2020 levels. When the pandemic hit, both Dynamic and Static firms began reducing the number of equity partners in their ranks. Static firms cut their equity partners down 3.5% from their January level, while Dynamic firms only cut down 1.4%. Dynamic firms returned to pre-pandemic levels at the beginning of 2021, yet Static firms are still below their January 2020 equity partner levels as of June.

Look again to the KPI measurements. Worked rates for Static firms are up 8.3%, but fees worked is at a lower level, growing only 6.6%. This is because demand, measured by the hours a firm worked, is down 3.3% on average for Static firms. Indeed, Static firms have witnessed greatly reduced demand in almost every practice during Q2, with litigation, bankruptcy, and tax each seeing billable hours contract by 9% or more on average when compared to 2019 volumes. If anything were to happen to corporate or real estate practices (the only major categories with any sign of growth), Static firms could be thrown once more into crisis.

In the last few months, the labor market has tightened and even with skyrocketing salaries firms are having trouble finding talent. Multiple economic threats still loom, COVID-19 is by no means gone, and the specter of cheap credit being replaced by high inflation persists. Any of these threats could very well jeopardize that essential corporate work — the very practice that is enabling Static firms to hold onto some 2019 levels.

This fairytale is not over, the dragon yet lives. This time, Static firms may have to slay it themselves.