While the average law firm saw demand drop in 2020, profit per equity partner increased by an average of 11.5% because of shifts in who was doing the work

There is much evidence that the large law firm market finds itself at a crossroads. Evidence of the approach toward a tipping point was laid out in the 2021 Report on the State of the Legal Market, which is jointly issued annually by the Center on Ethics and the Legal Profession at the Georgetown University Law Center and Thomson Reuters Institute.

In 2020, a year that was anything but normal, the average large law firm in the United States increased their profit per equity partner (PPEP) by an average of 11.5%. That may come as quite a surprise to many — especially when considering some of the surface-level metrics occurring at the same time. For example, the average law firm saw demand, measured by the number of billable hours worked, decrease by 1.6% over the same period. Litigation, the largest practice by proportion of hours worked, decreased by nearly double that.

Since the onset of the pandemic, firms have swiftly and aggressively reduced their expenditures. Headlines noting dramatic cuts in marketing & business development costs served as effective attention-grabbers and were an easy enough target for many to cite as the main driver of firms’ profitability growth. However, while the firewall around profitability created by expenditure cuts did contribute, it was not the main driver of the historic highs in PPEP.

No, the main driving force was the surge in the average worked rate charged in the market.

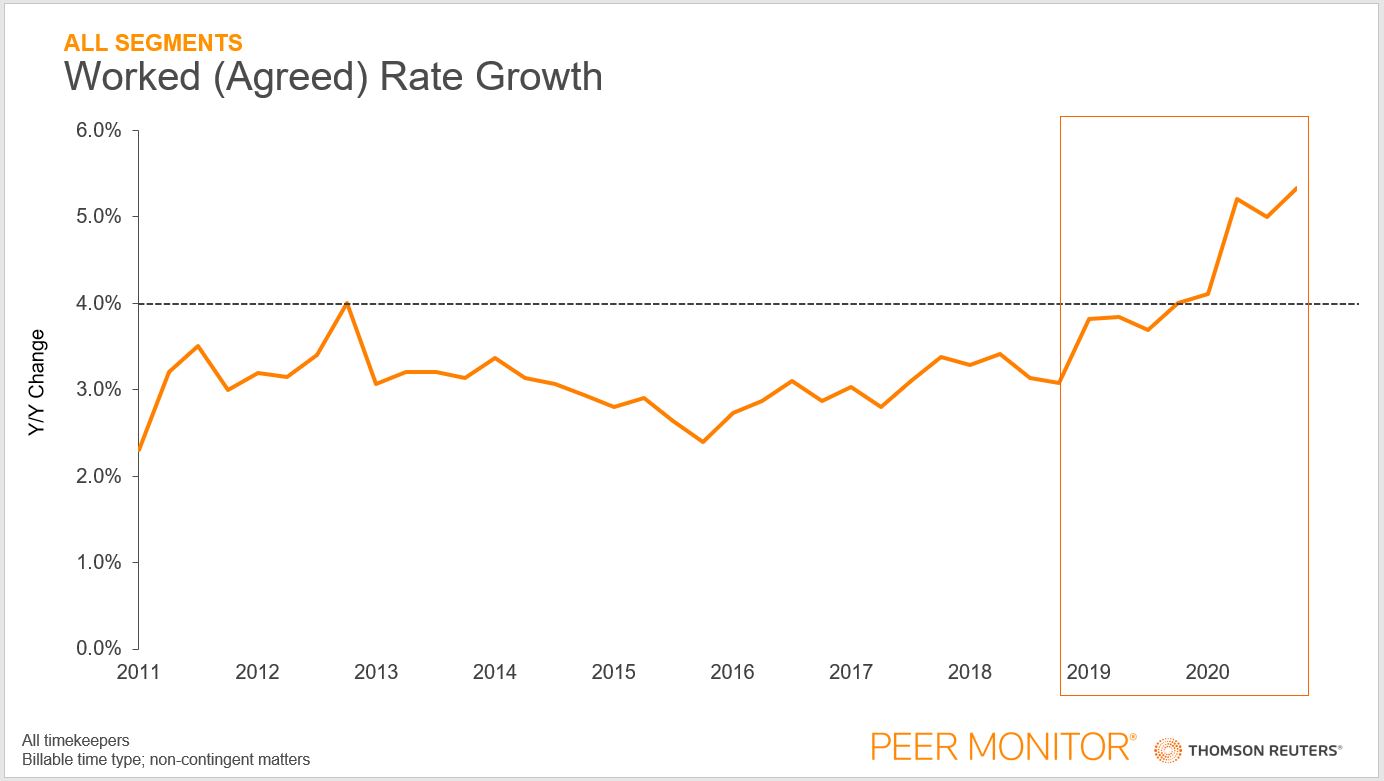

Worked, or agreed-on, rates grew by an average of 4.9% overall in 2020. Further, after a first quarter with historically solid 4.1% growth, the last three quarters of 2020 all eclipsed 5.0% on their own. For some perspective, the average worked rate increase per year from 2011 to 2018 was 3.1%.

Firms did not begin charging higher rates once the pandemic truly took hold on the country in March, so what happened?

It was who was doing the work that changed.

In the early months and at the peak of the unknown, firms reported that they “were hearing directly from the clients, that in a period of uncertainty, ‘We really want to rely heavily on the counsel of individuals who know our business best, who have longstanding relationships,’” explains Mike Abbott, Vice President of Market Insights and Thought Leadership at Thomson Reuters. “And that’s frequently the partner level. So, a lot of that work was staying with or actually going to more senior people at the law firms.”

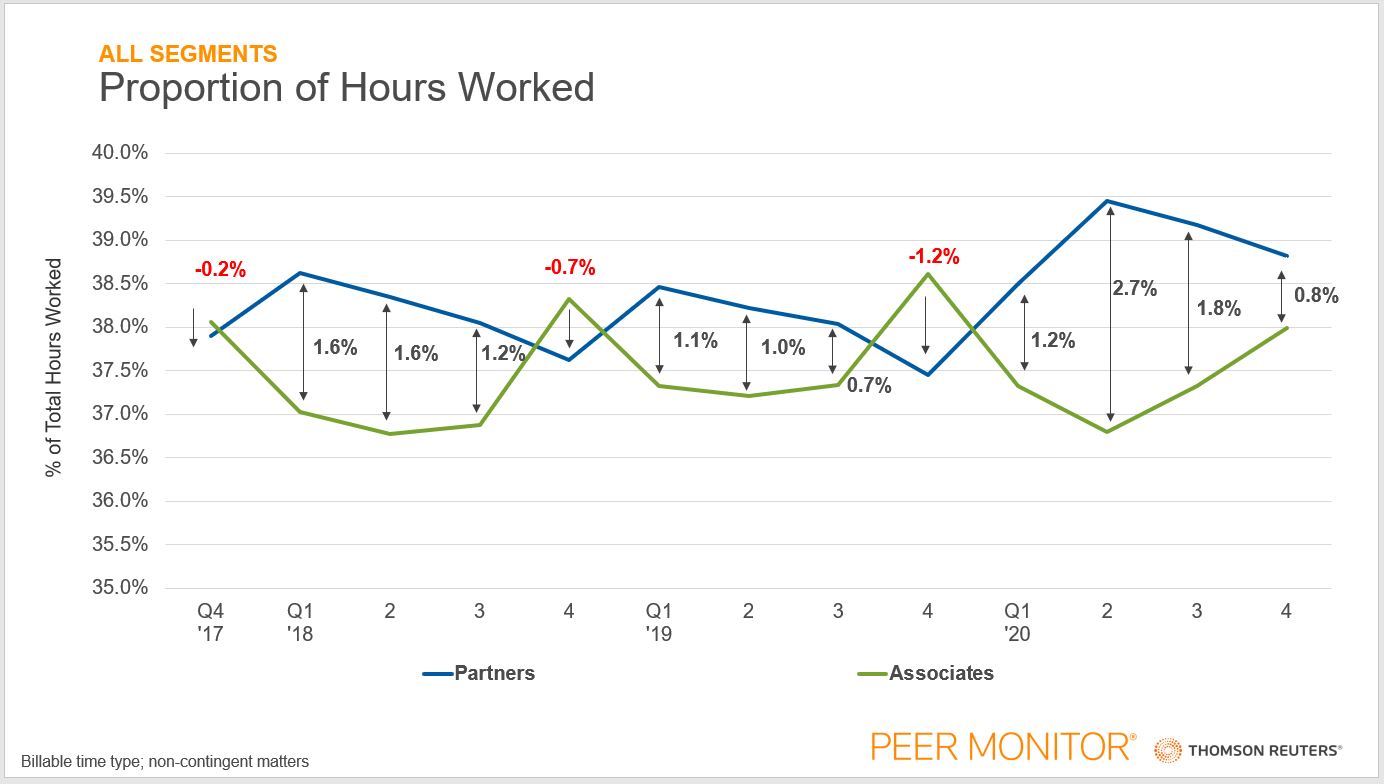

Partners, who worked between 1.6% and 0.7% more of all hours relative to associates, worked a full 2.7% and 1.8% more in the second and third quarters, driving the average worked rate even higher. Associates, who in the fourth-quarter periods in the last three years would actually work a higher proportion of hours than partners, for the first time fell short in 2020’s fourth quarter. It is worth noting here that this was not all based on client preference; and associates also were the preferred target of firm layoffs among the lawyer ranks. The average law firm employed 4.5% less associates by the end of December 2020 than they had in December 2019.

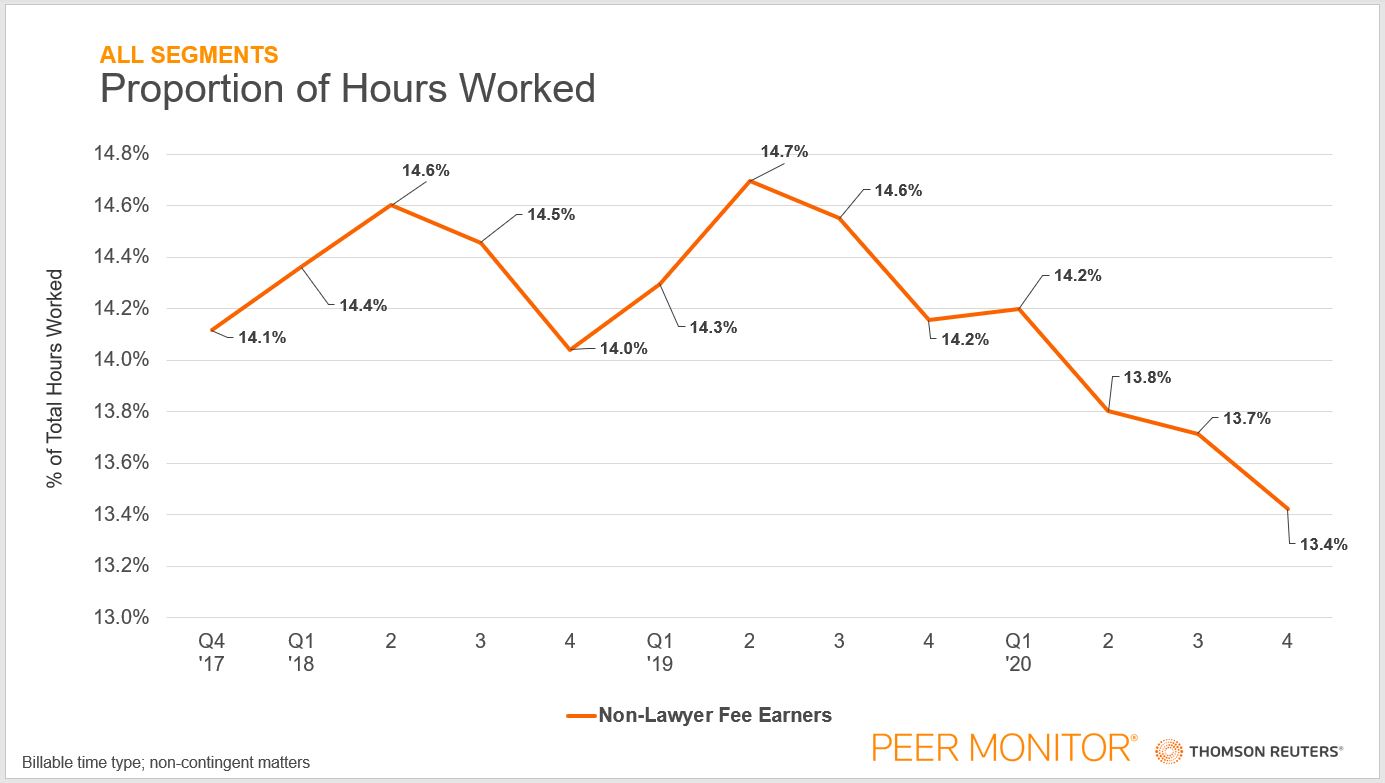

Further compounding the rise in rates attributed to work shifts were non-lawyer fee earners. Allied professionals, such as paralegals, were responsible for between 14.1% and 14.7% of all billable hours between Q4 2017 and Q1 2020. That mark decreased each quarter subsequently in the past year, as allied professionals were subject to headcount reductions that started in March and persisting through the remainder of the year. By year’s end, allied professionals only worked 13.4% of all billable hours in the fourth quarter.

The decrease in the amount of work completed by lower-fee associates as well as allied professionals coupled with the corresponding increase in work completed by partners at their higher-on-average rates had an outsized effect on law firm profitability.

Firms began 2020 with initial rate increases of 4.1% and shifts in who was doing the work was a main driver of the additional percentage point of worked rate growth that occurred from the Q2 through the end of the year.

Still, many questions remain. Chiefly, will clients be willing to accept similar levels of rate increases in 2021, especially if the pandemic crisis wanes? As we progress into 2021, this question will weigh heavily on the market and hold in its resolution whether the outlook for law firms represents a true tipping point in the delivery and pricing of legal services.