The EU's Omnibus initiative seeks to streamline mandated sustainability reporting by narrowing scope and data points to cut compliance costs, but it ignites a debate over whether simplification will erode accountability and comparability as the legislation moves toward a resolution

Key takeaways:

-

-

-

Smart resource efficiency and decarbonization are good differentiators —Concrete gains in decarbonization, smarter resource efficiency, and rigorous human-rights due diligence increasingly distinguish market leaders from the rest.

-

Consideration for voluntary reporting is required — Companies should keep strengthening ESG data governance, involve finance and audit early, and consider voluntary alignment to maintain credibility with investors and supply‑chain partners regardless of legal thresholds.

-

Ongoing monitoring of regulation is critical — Legal uncertainty will continue, likely even up to the final decision. Companies should expect ongoing uncertainty and legal risk throughout the rest of this year.

-

-

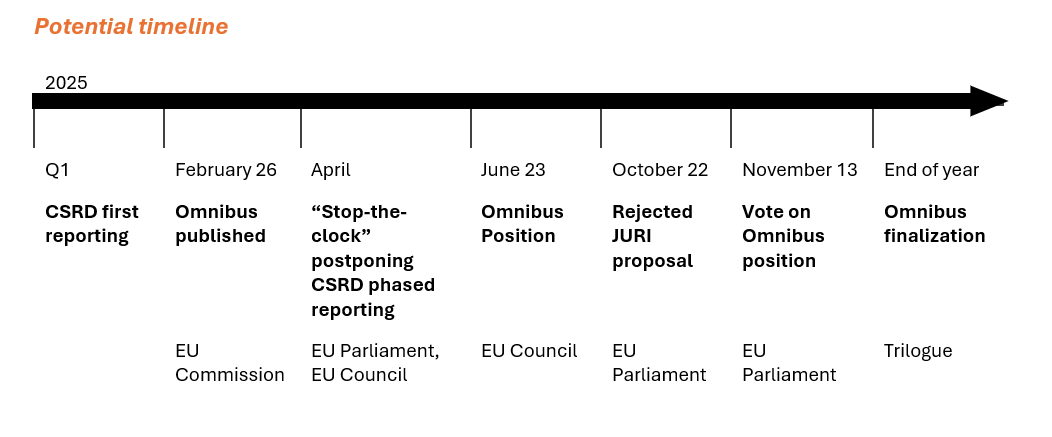

The European Union’s effort to streamline its sustainability rulebook has entered a decisive stage. Through the Omnibus initiative, the European Commission aims to align and simplify overlapping environmental, social, and governance (ESG) regulations, particularly its Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD). Framed as a push to enhance competitiveness, the Omnibus package reflects a broader recalibration that seeks to balance economic pragmatism with the EU’s sustainability ambition. The current goal is to finalize the legislative process by the end of 2025.

Over the past three years, the EU has assembled one of the world’s most far‑reaching reporting frameworks. CSRD seeks consistency and comparability in disclosures, while CSDDD extends human‑rights and environmental responsibilities across value chains. The Omnibus would narrow which companies report, reduce data points, and limit due‑diligence obligations mainly to tier‑one suppliers.

Proponents argue this will ease compliance and focus effort where it matters most. Critics fear that fewer reporters and fewer metrics could dilute accountability and the CSRD’s role as a global benchmark.

Debating the details

Decision‑making now shifts to the European Parliament and the Council, followed by a trilogue, in which the institutions converge on a compromise text. The Council has already staked out a position to raise the CSRD turnover threshold to €450 million from €50 million, which would significantly reduce the number of companies under its scope. Inside Parliament, center‑right groups prioritize deregulation and cost relief, while left‑leaning groups press to maintain or strengthen standards and comparability.

What happens next will determine scope and granularity. If thresholds rise and data points drop, complexity and audit costs decline, especially for smaller and midsize companies. Yet comparability could suffer if disclosures become thinner or less standardized.

The central question is whether simplification improves usability or merely softens obligations. Striking the right balance will shape the EU’s standing as a standard‑setter and the usefulness of ESG data for capital allocation, supply‑chain management, and regulatory oversight.

Reactions remain split. Business groups welcome burden relief and a narrower due‑diligence perimeter as pro‑competitiveness measures. Civil‑society organizations and some investors, on the other hand, warn that scaling back disclosures could undermine transparency, reduce comparability across sectors and borders, and weaken incentives for meaningful action on environmental and social issues. The debate underscores the persistent tension between short‑term economic pressures and long‑term sustainability objectives at the heart of the Omnibus process.

What companies should do now

For companies preparing for CSRD, the Omnibus adds uncertainty. While some smaller organizations may fall outside scope, larger enterprises must continue under a simplified regime. Practical steps include maintaining strong ESG data governance, engaging finance and audit teams early, and focusing on material topics that drive performance and risk management. Companies also should track institutional positions through 2025 and adjust their programs, targets, and controls as the final contours emerge.

Regardless of their position under the current or future framework, several strategic actions can help businesses stay prepared and maintain credibility with investors and regulators alike, including:

-

-

- Continue to strengthen sustainability data and governance — Even if the reporting scope narrows, robust ESG data management remains essential. Companies should ensure that internal processes, data systems, and oversight structures can deliver consistent and verifiable information. This will reduce compliance risks and position those companies well for any future expansion of requirements.

- Consider voluntary alignment with simplified frameworks — Some firms potentially falling outside CSRD scope may still benefit from voluntary reporting under frameworks such as those for small and midsize entities (SMEs). This supports transparency with lenders, investors, and supply-chain partners that increasingly may expect sustainability disclosures, regardless of legal thresholds.

- Focus on decarbonization and risk mitigation — Beyond reporting, tangible progress on decarbonization, resource efficiency, and human-rights due diligence remains a critical differentiator. Companies that integrate these areas into strategic risk management will be better equipped to respond to global sustainability standards and maintain market access in Europe.

-

The Omnibus represents more than a technical adjustment to EU sustainability rules. Indeed, it is a test of how effectively the bloc can balance economic pragmatism with ambitious climate and social objectives.

While the Omnibus may lead to political compromise, it does not fully close the door on legal risk. Legal scholars and practitioners have warned that certain proposed changes could conflict with EU principles of proportionality and the Charter of Fundamental Rights, particularly in the absence of comprehensive impact assessments.

For companies in Europe, the key takeaway is that even after legislative adoption, the regulatory landscape may continue to evolve, which will make ongoing monitoring essential.

You can find out more about the challenges corporations face with regulatory enforcement here