The Financial Data Transparency Act and structured business reporting are shifting from static, form-based filings to standardized, machine-readable data, enabling greater efficiency, transparency, and strategic opportunities for both regulators and industry

Key takeaways:

-

-

-

FDTA drives a data revolution — The FDTA and structured business reporting are driving a shift to machine-readable data formats, which could fundamentally transform companies’ compliance processes.

-

Organizational change required — Successful adoption of the FDTA and structured business reporting requires not only technological upgrades but also significant cultural and skill changes within organizations.

-

Compliance in action — To successfully transition to data-driven compliance under the FDTA, organizations should conduct readiness assessments, appoint cross-functional leaders, adopt scalable data architectures, and actively engage with policymakers and vendors early in the process.

-

-

Financial reporting is at a turning point as regulatory consistency supersedes a check-the-box mentality. For decades, compliance in the United States has centered on paper-defined, form-based filings that were systemically encoded by software. Paper and e-form documents were submitted to regulators, parsed by analysts, and stored in disparate systems within industry and oversight agencies. This approach is quickly losing relevance, however, due to an explosion of data, new intelligent solutions, and a need for one version of the truth.

The vision of financial data modernization is not new, but its transformative speed and benefits are accelerating both internationally and domestically. For the US, the Financial Data Transparency Act (FDTA), signed into law in 2022, represents the first step to achieving structured business reporting, which was originally proposed in 2017. Each of these public-private initiatives represents sweeping mandates to transition from static reports to machine-readable, standardized data that in turn reduces compliance burdens, improves data quality, and in the long-term, reduces costs.

International data standardization and regulatory consistency directives began decades ago, and they represent lessons learned for domestic policy makers. FDTA legislation and structured business reporting designs represent the end of static reporting and the beginning of data-driven regulatory oversight. Both public agency and private industry leadership can treat the FDTA and structured business reporting as another regulatory mandate, or they can embrace it as the building blocks for financial data modernization in which compliance consistency can be a driver of efficiency, transparency, and competitive advantage.

From documents to data

The FDTA requires US regulators to adopt common, machine-readable formats for the data collected. By 2027, regulatory filings will no longer be about submitting PDFs or e-forms — rather, submitted filings will require structured, standardized, and interoperable datasets.

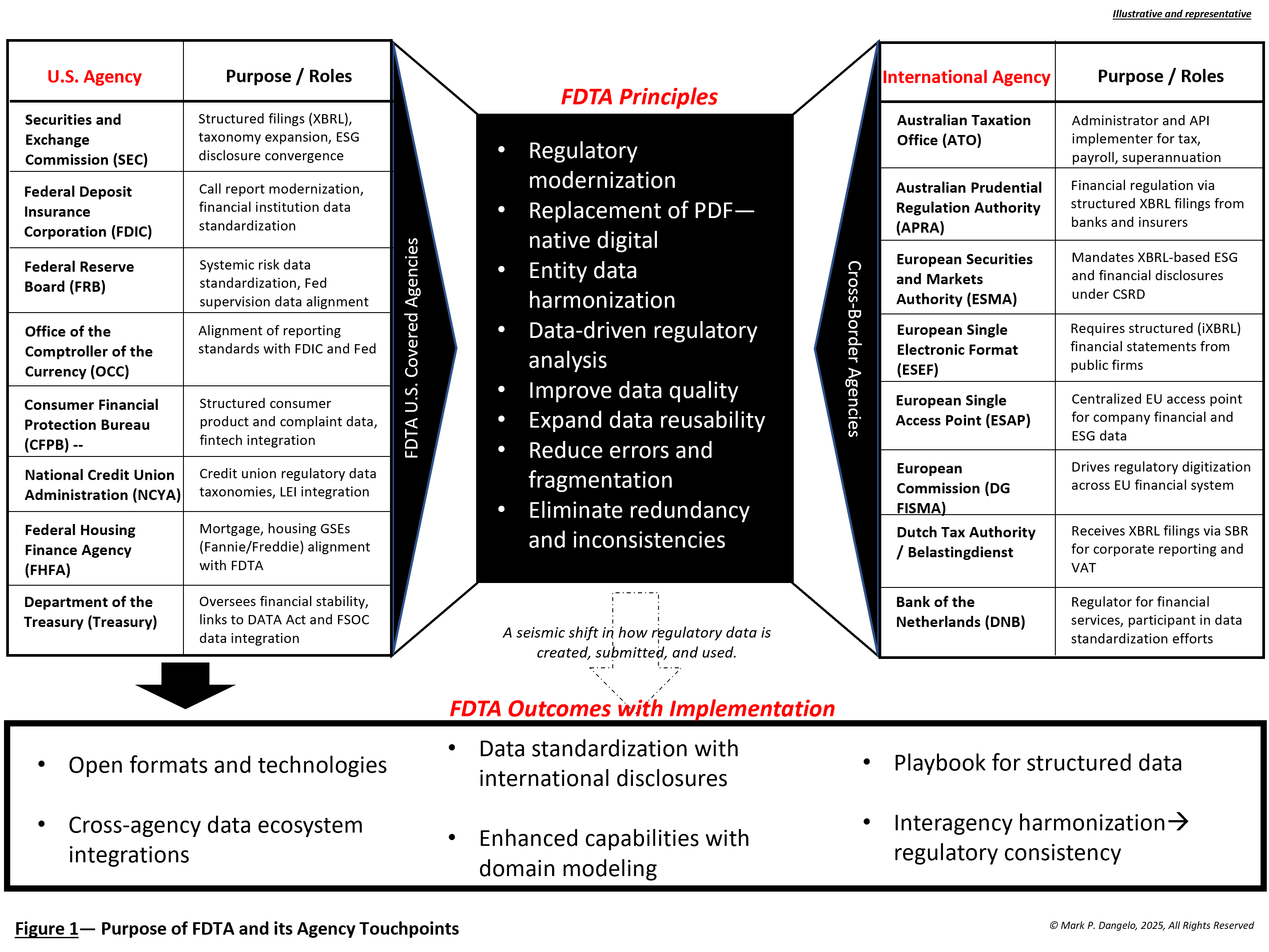

This is more than an administrative shift. Indeed, it will force agencies and industry to overhaul data ingestions, governance, taxonomies, and internal systems to ensure that filings are accurate, traceable, and consistent across individual data stores. The chart below showcases the regulatory agencies impact by FDTA and the oversight influences from non-domestic partners.

While the FDTA will require organizations to invest in supporting data technologies, the longer-term efficiencies, elimination of duplication, and improved transparency must be balanced against data design and governance changes and staff retraining. In this way, the FDTA represents the initial starting point of rethinking regulatory compliance with an eye toward financial data modernization.

Due to its data-driven fundamentals, structured business reporting is designed for regulatory consistency across many agencies — not regulatory compliance and complexity. Taken holistically and using lessons learned from the foreign initiatives, which have preceded US adoption, structured business reporting is as much a cultural shift as a technological one.

Indeed, structured business reporting will require strong collaborations between public agencies, auditors, software vendors, and financial institutions. And its adoption will continue to be debated until such time that efficiency gains outweigh the pains of operational and data transformations.

Practical impact of people

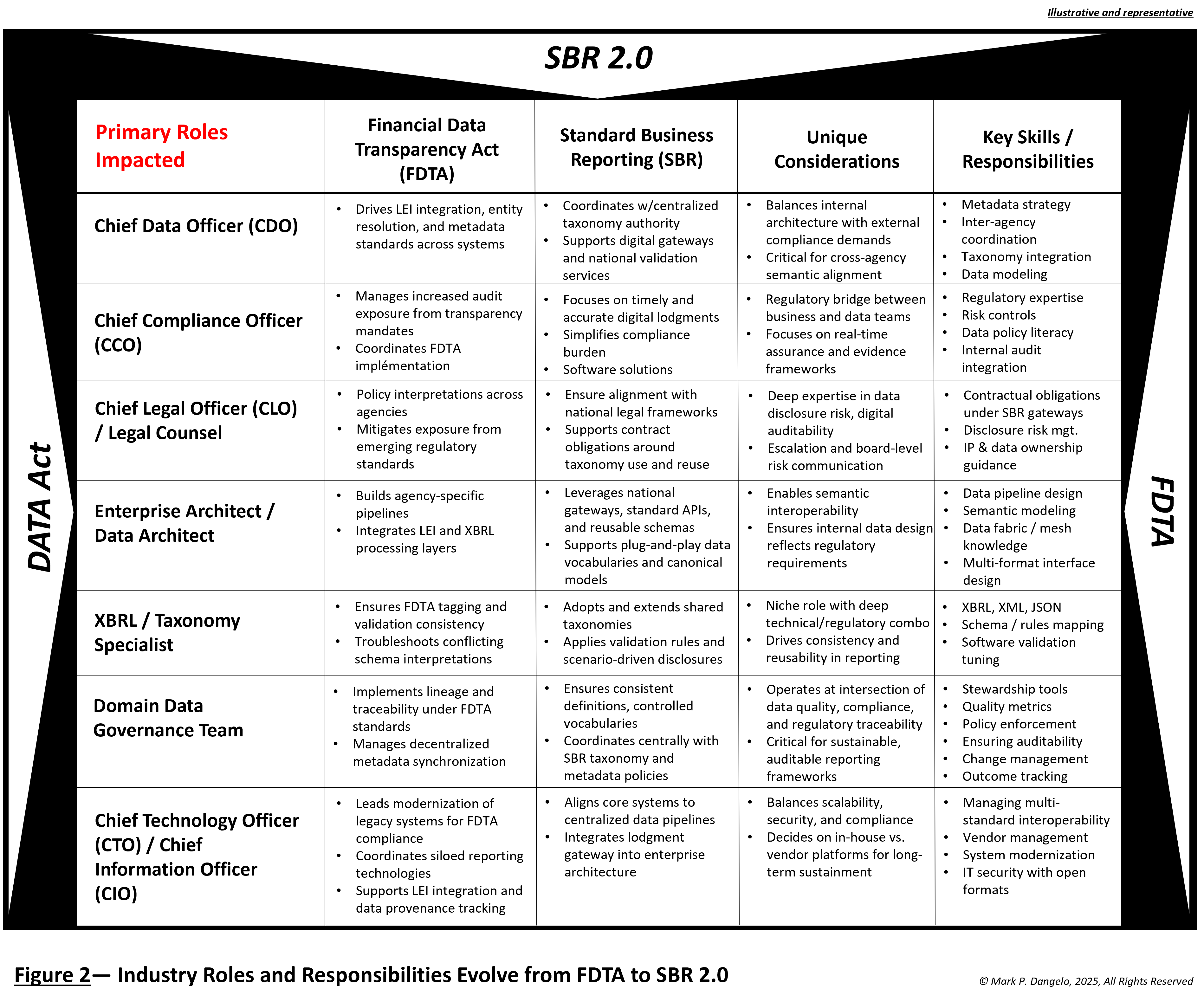

Data modernization is more than the schemas, taxonomies, and APIs often presented as solutions. Success for the FDTA and structured business reporting are rooted in people and skills. While each envisions native machine-readable data and robust cross-functional data governance demands, the investment in training coupled with continuous change management cannot be underestimated.

The chart below provides a snapshot of the differences using FDTA and structured business reporting as the catalyst for change.

What is also implied from this comparison is that the legal and audit implications are non-trivial. Once filings are machine readable, discrepancies, errors, or omissions are visible using advanced analytics and growing AI capabilities. Litigation, enforcement, and reputational risks will reside with the quality, variation, and integrity of the data submitted. The skills needed for these eventualities and the demands to get it right the first time will create unfamiliar priorities against traditional business-as-usual practices.

The calls to action

The FDTA is a legislative demand which will accelerate its reach over the next two years. By not actively engaging with agencies to shape the final implementations of the FDTA, industry leaders risk more of the same inefficiencies when it comes to systems, complexities, data fragmentations, and rising compliance costs.

To prepare for the FDTA and structured business reporting, leaders are encouraged to: i) conduct readiness assessments; ii) appoint cross-functional leaders; iii) adopt scalable, compartmentalized data architectures; iv) design success using crawl, walk, run approaches; and most importantly, v) engage with policy makers and vendors early.

The real benefits beyond traditional compliance cultures and systems, once data is standardized, are many-fold, including: i) AI-driven regulatory consistency, such as leveraging RAG and agentic AI; ii) predictive regulation that can anticipate potential exposures; iii) market innovations using transparent data; and iv) safeguards that consistently protect data regardless of the platform or application.

The market demands are clear: Consistent compliance data is an economic imperative. Data modernization will not only meet public regulator demands but also will provide scalable data architectural building blocks that will improve organizations’ transparency, auditability, efficiency, and trust.

Institutions that thrive using the FDTA and structured business reporting will treat regulatory data not as a burden of regulatory compliance — but rather as data-driven, regulatory consistency asset that spans the organization. Indeed, US markets cannot scale the regulatory burdens any further — the FDTA and structured business reporting may represent an opportunity to permanently shift to data-driven submit once, use everywhere designs.

Of course, this all hinges on something unprecedented — industry taking the data-driven lead when it comes to financial data modernization and consistency around regulatory compliance.

You can find more blog posts by this author here