Technology is the primary way tax firm leaders wish to increase profitability, according to a recent report; however, firms need to focus more on strategic planning in order to extract value from that technology

Key insights:

-

-

-

Technology is a priority — Those tax, accounting & audit firms that are prioritizing technology to increase efficiency and profitability are already seeing improved efficiency.

-

Strategic planning is essential — While technology is crucial, many firms still lack a formalized growth strategy, which limits their ability to extract the most value from their technology investments.

-

Positive financial outlook — Despite challenges, tax firms are in a strong financial position, with 65% reporting increased revenue in the past 12 months and 45% seeing profit growth.

-

-

For today’s tax, audit & accounting firms, there are a number of differing pathways to reach growth and profitability. Many are expanding their service offerings, such as a move into advisory services; some are looking to increase headcount, betting that more personnel can translate into more work from clients. And a portion are even looking into outside investment, such as from private equity firms, hoping that a bolstered bottom line can help them get a jump start on the competition.

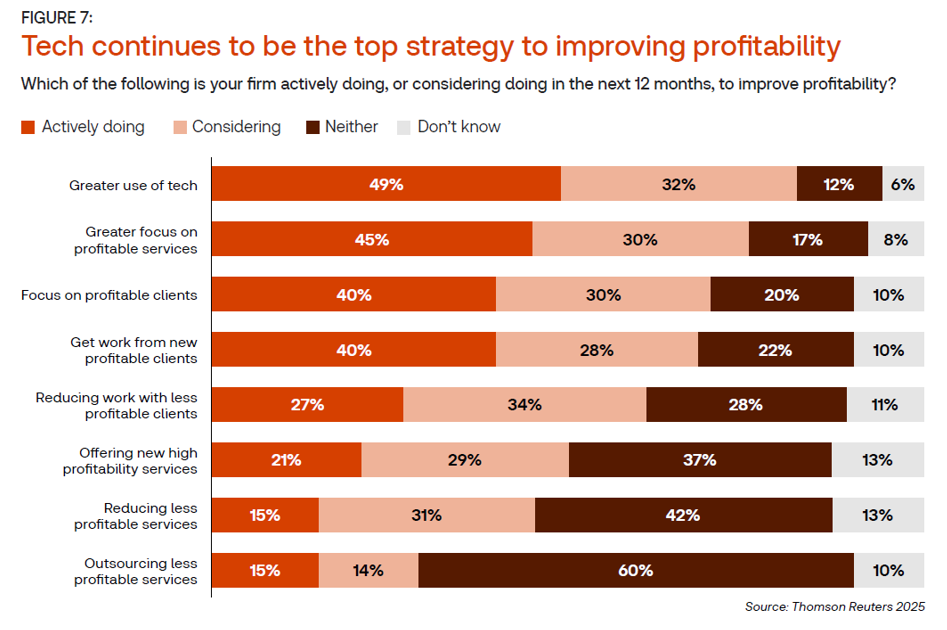

Yet no matter the growth strategy, there is one paramount priority among all firms today: technology, which they see as a necessity to gain greater efficiency. Indeed, improved efficiency and adding more technology are tax firms’ top priority for the coming year, and in turn, greater use of technology is seen as the dominant strategy to drive firm profitability, according to the recently released 2025 State of Tax Professionals Report from the Thomson Reuters Institute.

Tying technology to overall growth, however, may be easier said than done. Many firms still have not formalized their growth strategy, and a number are still trying to optimize use of their current technology, let alone keep up with new innovations such as generative AI (GenAI). As a result, technology may be the primary way firm leaders wish to increase profitability, but they need to focus more on strategic planning to better extract value from that technology in order to succeed.

The importance of efficiency

Overall, today’s tax, audit & accounting firms look to be in a strong financial position. Almost two-thirds (65%) of survey respondents report that their firms saw increasing revenue in the past 12 months, while 45% say their firm’s profit has grown, too. Similar percentages also report expecting their firm to increase revenue and profit over the upcoming 12 months as well.

Even with these positive indicators, however, many firm leaders indicate there is more room for growth. In particular, many are pointing towards technology as a potential area of interest, with nearly half (49%) of respondents saying their firms are actively applying greater use of technology as a growth strategy, while an additional 32% said their firms are considering technology usage as part of their growth strategy.

This is perhaps no surprise given the tax industry’s need to do more with less. Previous years’ iterations of the Tax Professionals Report have highlighted the recruiting and talent struggles facing the industry, and this year is no exception. Hiring, attracting & retaining talent, and staffing matters still rank among the top challenges for firm leaders, and as such, it’s no surprise that firms are turning towards automation to fill those gaps.

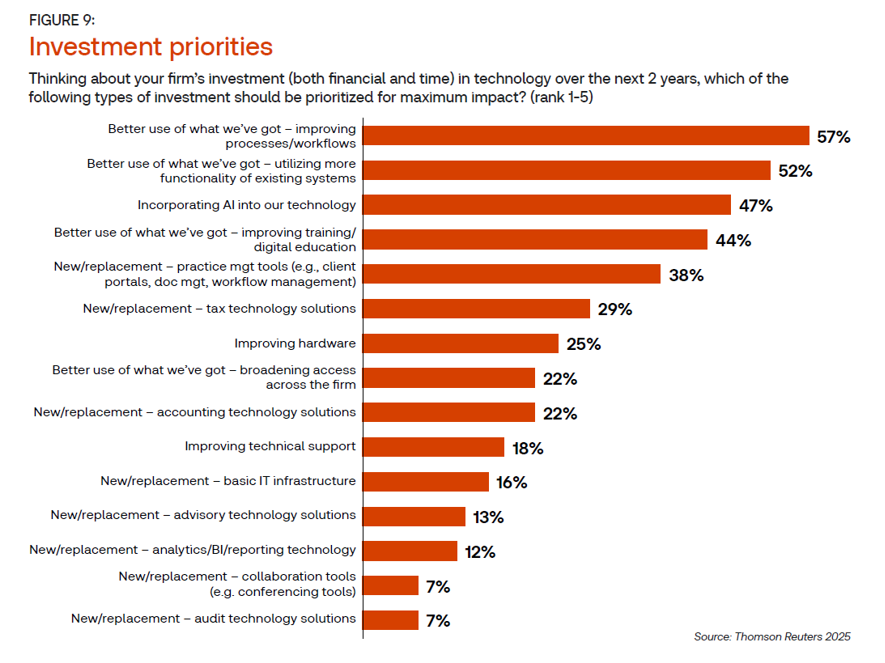

New advanced tech tools such as GenAI are increasingly included among those strategies that leaders see that could make up for talent shortages by providing more efficient tax return preparation, regulatory research, and document summarization and review, among other tasks. According to the report, however, while firm leaders are interested in GenAI and other new technologies, they’re still looking to extract more value from the technology tools they already have first.

Indeed, when many firm leaders talk about technology driving growth, it may not be that they’re really considering investing in new technologies at all. Many firms have invested heavily in technologies in recent years, but don’t actually get the most value out of those new systems because they are left unused, or because tax professionals are untrained and don’t use the systems properly — or even because client demands do not align with the technologies that firms have put in place.

When firm leaders want technology to drive their future, what they really want are more efficient processes and procedures that technology can bring, allowing them to do more with less.

A strategy for technology

With that in mind, how can tax, audit & accounting firm leaders extract the most value from their technology purchases, both new and old? It starts with tying technology usage to the overall growth strategy of the firm.

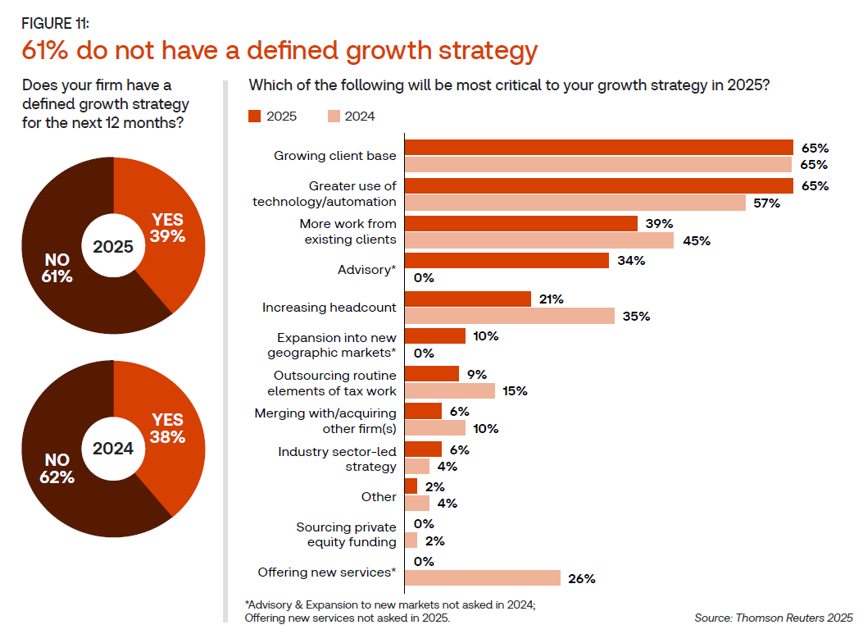

In some ways this should be straightforward, given how many firm leaders cite efficiency as one of their foremost goals. For some firms, however, tying technology to strategy may run into a fundamental problem: They don’t actually have a directly defined growth strategy. This is true particularly for smaller firms (those with 1 to 3 employees) at which only 26% of respondents said their firm had a defined growth strategy. However, even in midsize firms (4 to 29 employees), just 40% of respondents said their firm had a defined growth strategy.

Given that, getting the most out of technology may require firms determine a defined strategy for growth first. That strategy can have a number of varying facets, but of those firms that do have a growth strategy, it’s no surprise that technology and growth are intertwined. About two-thirds of respondents report greater use of technology and automation as a part of that strategy.

With a growth strategy in place, firm leaders should then more easily be able to invest in technologies that would align with that strategy. For example, firms that include growing the client base as a core tenant of their growth strategy may want to invest in marketing and business development technologies, or explore which of their pre-existing technologies can be leveraged for that purpose. Firms looking to grow by moving into advisory services for the first time, meanwhile, may be looking to leverage technologies such as GenAI for idea and document generation.

Regardless of what direction that growth strategy may take a firm, it’s clear that technology will likely play a major part in its future. Not only are clients clearly indicating that they want their outside tax firms to do more with less, but those firms now see that technology is having a positive impact on their bottom line.

As the Tax Professionals Report notes: “Many people have concerns about the impact of AI and other emerging technologies on how professional services are managed and delivered, but the evidence thus far suggests that the onward march of technology is helping (not hurting) accounting firms’ ability to provide the services and guidance their clients want and need.”

You can download a full copy of the Thomson Reuters Institute’s 2025 State of Tax Professionals Report here