Diving deeper into the recent "2023 Report on the State of the Legal Market", we take a closer look at how demand growth was distributed and why some firms saw increases, while others saw declines

The Thomson Reuters Institute’s 2023 Report on the State of the Legal Market was by no means a victory lap for the large law firm industry. Worked rate growth was below inflation, and significant expense growth contributed to a decrease in firm profits in the absence of demand growth.

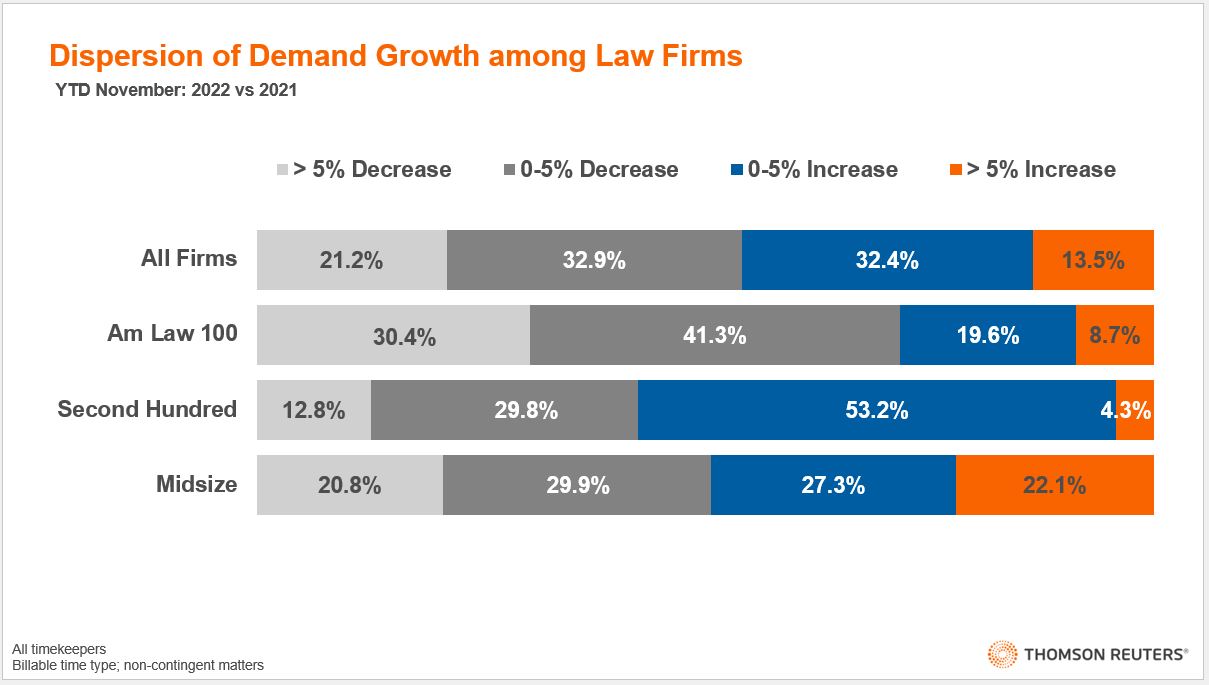

Yet, while the average firm may have fared less spectacularly than in previous years, there was a small subset of firms (roughly 13.5% of the large law market) that had an extremely successful year, growing their worked hours by 5% or more year-to-date through November 2022. Simultaneously, a much larger subset of 21.2% of firms had a rougher time, with their hours worked declining by more than 5%.

With such a wide breadth of success, we wanted to take a closer look at how demand growth was distributed this year, and how some firms managed to grow their worked hours considerably while other’s saw notable declines.

To best see this dispersion, we’ve separated law firm segments into four sub-groups based on performance:

-

-

- firms with a greater than 5% decline in demand;

- firms with a decline in demand greater than 0% but less than 5%;

- firms who grew demand greater than 0% but less than 5%; and

- firms with a greater than 5% increase in demand.

-

While it is true that Midsize law firms had higher average demand growth in 2022, the Am Law Second Hundred segment actually achieved a greater proportion of its firms achieving some form of demand growth compared to their non-Am Law counterparts. At the same time, the proportion of Midsize firms that saw that 5%-plus surge of growth was five-times as large as the Second Hundred’s. In other words, the majority of the Am Law Second Hundred firms managed to sustain, while a portion of Midsize firms were able to thrive.

The Am Law 100 segment, conversely, saw 71.7% of its firms bill fewer hours than last year, with less than one-tenth of these firms growing beyond the 5% level.

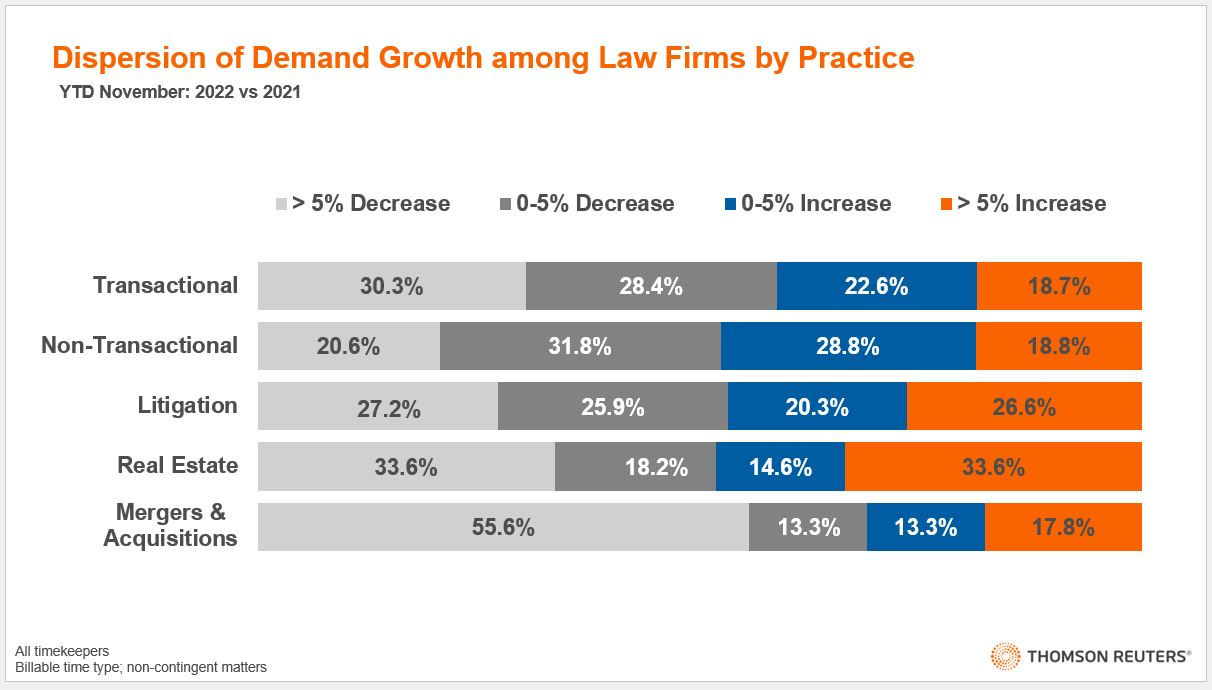

As stated in the report and other publications, part of the blame for this disparity in demand growth between size segments comes down to the practice mix. Am Law 100 firms tend to be more leveraged towards transactional practices and thus more vulnerable to macroeconomic headwinds that accompany that work. Transactional work — composed of the corporate general, real estate, tax, and mergers & acquisitions practices — saw large declines as economic uncertainty and inflation made clients uneasy.

Indeed, almost one-third of law firms experienced a greater than 5% decrease in hours worked, compared to non-transactional work in which only 20.6% of firms declined as severely. This, plus the greater growth that larger firms had in this area in 2021 and early 2022, played a large part in the struggle that Am Law 100 firms experienced.

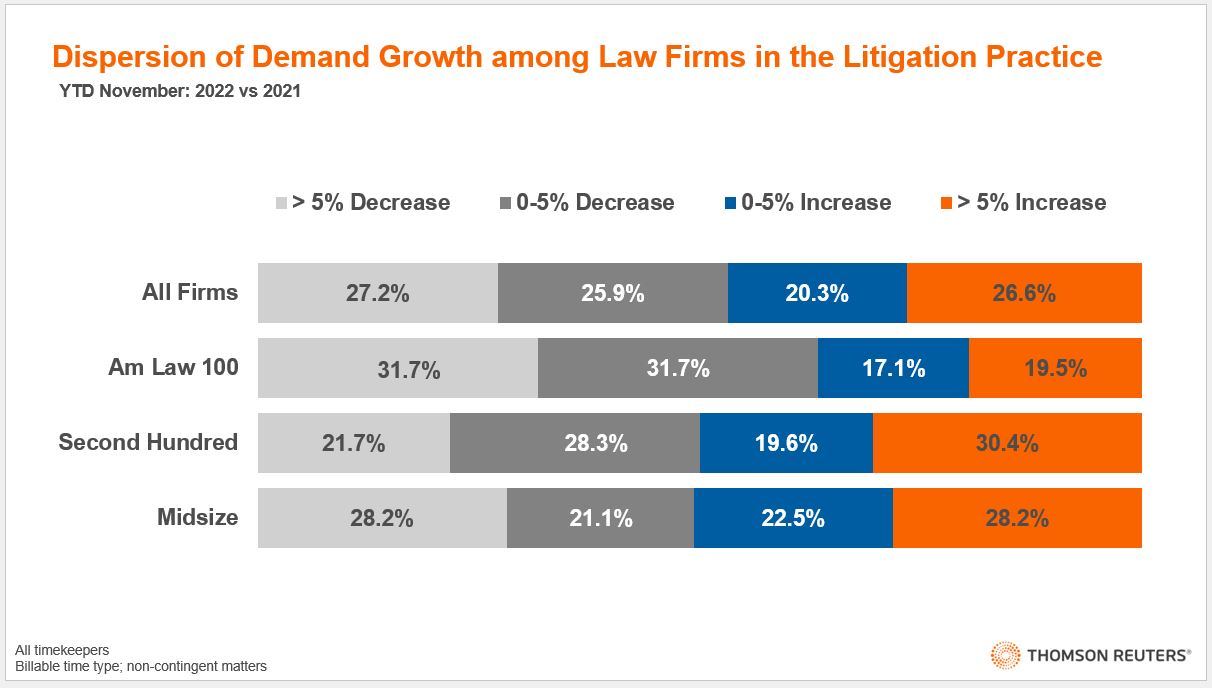

However, the impact of practices went beyond segmentation’s practice alignment. When we look at a single practice such as litigation, which makes up a large portion of hours for both Am Law and non-Am Law firms, we can see a growth dispersion that controlled for this factor.

Even with growth in litigation last year favoring smaller firms, we can see segmentation still had a major effect at the individual practice level. The Am Law 100 segment had 63.4% of their firms see declining litigation demand in 2022 compared to other segments which saw at least half of their firms grow litigation demand. So, if this isn’t a case of practice mix, baselines, or general practice headwinds, why are some law firms struggling more than others?

The answer may lie in price. Am Law 100 firms are generally able to command higher rates due to their position in the market and their decision to leverage prestige in pricing is an important long-term strategic angle for law firm leaders. In tight times in which clients are looking to save money, it’s not unreasonable to believe these clients may move down-market to cut the cost of legal services. (This idea that demand is mobile within the legal market is a topic we examined at great length in the State of the Legal Market Report.)

As clients pulled back due to macroeconomic uncertainty and inflationary pressures on their budgets, they seem to become more cost sensitive and are moving their business to lower-cost firms. Some of our data supports this proposition, with clients reporting smaller spending increases per hour compared to the average increase of firms, as well as a majority of clients directly saying that they’ve included new law firms among their roster of outside counsel.

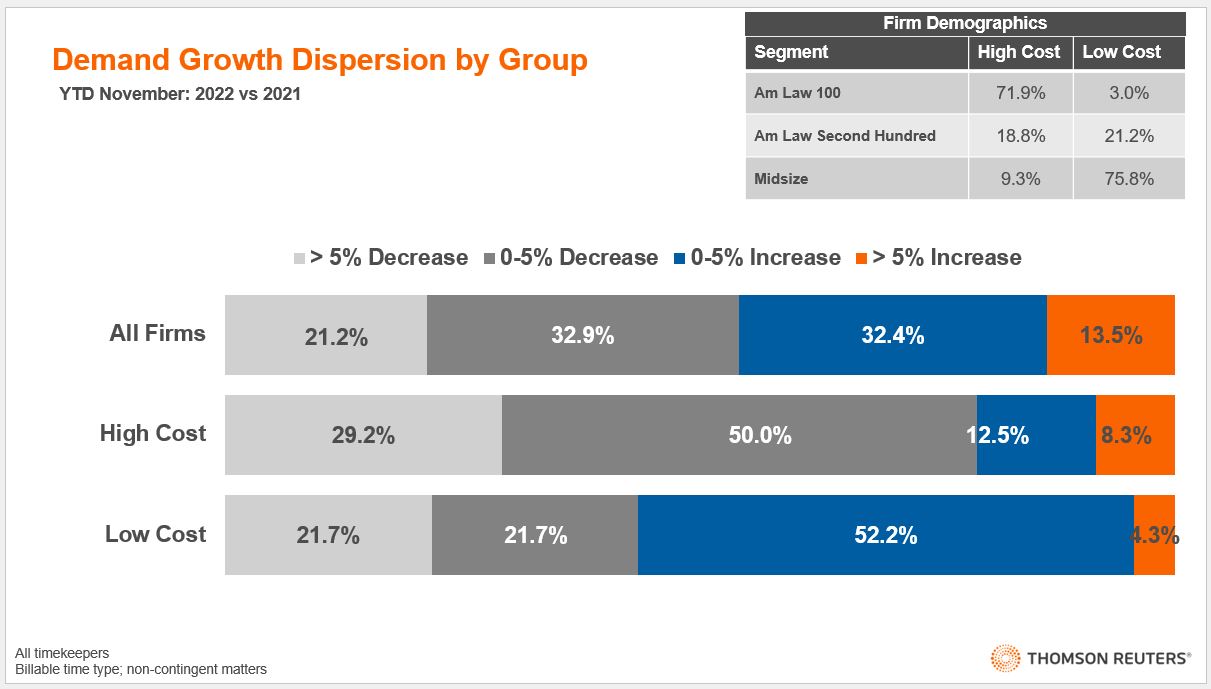

To show this, we broke down firms into two new categories — high-cost firms and low-cost firms, each in the respective 20th percentile of worked rates for the entire market. While there is large crossover between the traditionally more expensive Am Law 100 and these high-cost firms, the new group does include some Second Hundred and Midsize firms. This is again mirrored in the low-cost firms, which include a majority of Midsize firms but also a share of firms from the other segments.

Looking at the demand dispersion of these groups illustrates the idea of mobile demand with greater clarity. A full 79.2% of the high-cost firms saw demand decline in 2022, compared to 2021; and only 8.3% of these firms managed to grow significantly during that time.

At the same time, low-cost firms significantly outperformed the industry’s average proportion of positive growth, but notably the majority of these firms only achieved a relatively small degree of demand growth, with less than one-in-twenty of these firms growing more than 5%. Combined with our findings in the State of the Legal Market Report that these low-cost firms struggled to grow their rates, it would seem that the success of low-cost firms was even more limited that a mere average demand growth suggested.

Seeking to be a high or low-cost provider is a vital strategic decision for a firm and, as we can see in the above graphic, that decision can have steep consequences. Simply focusing on using the premier reputation of your firm or leveraging a low sticker price was not enough of a strategic advantage to find grand success in 2022.