Australian law firms remain on solid ground at midyear, but a closer look reveals diverging strategies and early signs of structural change in the market

Key findings:

-

-

-

The market remains strong, but growth is difficult — Australian law firms are still posting solid demand and rate growth in the first half of FY 2026, yet the pace is becoming more challenging to sustain.

-

Australia is no longer a single legal market, but three distinct ones — The report identifies three clearly differentiated law firm segments: Large firms leading demand growth through aggressive investment; Big 8 firms emphasizing pricing power and cost discipline; and Midsize firms pursuing steadier, more moderate growth.

-

Early signals suggest GenAI is reshaping productivity and leverage — Changes in hours worked across seniority levels point to possible early impacts of GenAI; and while overall productivity is stable, non‑equity partners and associates are logging fewer hours, while senior associates and equity partners are working more.

-

-

The Australian legal market enters the back half of FY 2026 with strong topline numbers, but beneath the surface, the market is working harder to maintain its momentum. Firms are navigating slower rate growth, shifting demand patterns, and the early tremors of what may prove to be a generative AI-driven transformation.

Solid footing, harder-won gains

Australian law firms built an impressive track record over the post-pandemic era, and the first half of FY 2026 shows that run may not be over yet — although its character is changing. Demand growth of 4.8% year-to-date sits a full percentage point above the average quarterly pace since FY 2022, according to the Thomson Reuters Institute’s just-released 2026 Australia: Midyear Legal Market Update report. Worked rates, meanwhile, rose 4.7%, which is respectable, but a noticeable step down from the 5.4% average growth firms had enjoyed since FY 2022.

At the practice level, the picture is broadly encouraging. Both transactional and counter-cyclical practice groups are accelerating, with workplace relations leading all practices at 9.9% year-to-date growth and corporate general close behind at 7.7%. However, a potential warning sign lies in the divergence among each macro-category’s flagship practice: insolvency & restructuring is surging at 7.9%, while mergers & acquisitions sits in contraction at -2.1%. If dealmaking remains subdued while restructuring activity accelerates, transactional practices could face meaningful headwinds in the quarters ahead.

Three markets, not one

Perhaps the most significant finding in this year’s report is what the market-wide averages have been concealing. Last year’s Australia State of the Legal Market report highlighted growing competition between the Big 8 and a broader group of Large law firms that were challenging the Big 8’s dominance. This year, a refined three-segment framework reveals that the former Large category was actually masking two very different stories, between Large firms and a newly identified set of Midsize firms.

The newly delineated Large firms have emerged as the clear demand leaders, posting nearly 7% year-to-date growth — roughly double their peers — fueled by aggressive investment and expansion. The Big 8, by contrast, are leaning into pricing power and cost discipline, growing demand at a more measured 2.7%. And the Midsize cohort, at 2.4% demand growth, is charting a balanced, moderate course.

The profitability divergence is even more striking. Since FY 2022, the firms now classified as Large have grown profits per lawyer by 27.4%, while Midsize firms managed just 3.1% — much closer to the Big 8’s 7.1% than to their former stablemates. What previously appeared to be a broad-based challenge to the elite was, in reality, concentrated among a smaller group of high performers that were pulling the average upward.

Early signals of AI-driven change

The report also surfaces a potentially significant development in law firm productivity. While overall hours worked per month ticked up slightly for the average qualified fee earner, the gains are unevenly distributed. Non-equity partners recorded their third consecutive productivity decline, and junior and mid-level associates are also slightly down. Yet senior associates and equity partners are logging more hours, keeping overall numbers stable. One possible explanation is GenAI — if firms are deploying these tools most heavily on research, drafting, and document review tasks that traditionally filled junior and mid-level associate hours, this is precisely the pattern we would expect to see. While it’s too early to draw solid conclusions, the distribution of hours may represent an early sign of how AI is beginning to reshape the traditional leverage model.

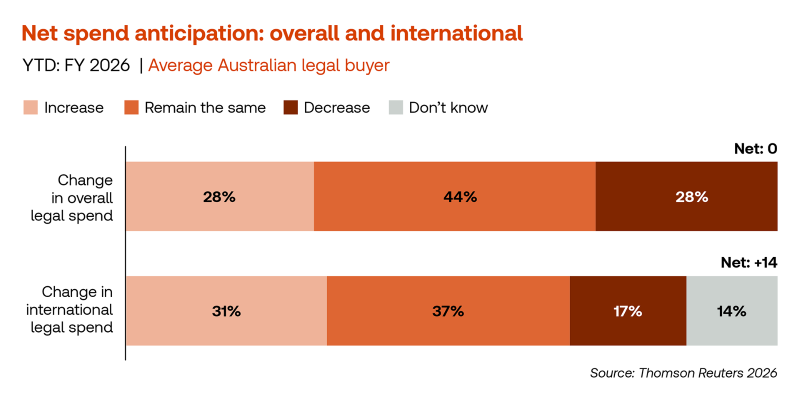

There is also a note of caution from firms’ clients. Thomson Reuters Market Insights data shows Australian general counsel growing more conservative in their spending outlook, with net spend anticipation for overall legal work dropping to 0 points. That means just as many GCs see their legal spend increasing as those that anticipating it decreasing.

Interestingly, international legal spend tells a different story — Australia-based GCs are increasingly looking outward, with the Asia-Pacific and Latin American regions emerging as areas of particular activity, while Europe has cooled. For Australian firms with cross-border ambitions, the short-term opportunity may lie to the global east and south rather than west.

Looking into the second half of the year

As the Australian legal market moves into the second half of FY 2026, the story is no longer one of uniform prosperity but rather, one of strategic differentiation. Demand remains healthy, profitability is solid, and expense discipline is improving; however, growth is no longer evenly distributed. The law firms that thrive in the quarters ahead will be those that understand which game they’re playing. In an increasingly segmented market, adaptability — not scale alone — will define success.

You can download a full copy of the Thomson Reuters Institute’s “2026 Australia: Midyear Legal Market Update” report by filling out the form below: