In the third quarter, the robustness of the legal industry was such that the LFFI reached its second-highest score of all time — but what is driving that growth?

The legal industry has been enjoying robust demand growth that is being mainly driven by counter-cyclical practices and improvement in transactional spaces, bringing hopes for a major resurgence in these latter group of practices— specifically in corporate M&A.

Indeed, so robust was this growth that the Thomson Reuters’ Law Firm Financial Index (LFFI) score rose 4 points in Q3 to an impressive score of 71 — the second-highest score of all time. As 2024 comes to an end, law firms are continuously experiencing significant growth, approaching near-record levels. In fact, with seven straight quarters of improvement, firms have not only achieved one of their highest historical scores but also appear to be fundamentally stronger than at any other time in recent years.

Demand in the legal industry performed exceptionally well, rising 3.6% in Q3. Worked rate growth also continued accelerating at a similar pace to the previous two quarters. Moreover, if we set aside artificially inflated growth for fees worked in Q2 2021 caused by the outbreak of the pandemic in the previous year, fees worked exhibited its fastest expansion historically this quarter.

Additionally, an increase in productivity was partly driven by the previously mentioned surge in demand, but another contributing factor was the restrained level of hiring by many law firms. Although they continued to expand their workforce, many firms did it at a more conservative rate than in recent years. Ultimately, the industry’s strength is clearly demonstrated by stable but managed expenses and solidifying growth, with revenue reaching record highs and accelerating rapidly, despite minimal contribution from one of the most lucrative practice areas, M&A.

While much of the third quarter’s vigor came from a resurgence in legal demand and counter-cyclical practices remained the major source of this growth, transactional demand also surprised many with a robust performance. M&A, probably the transactional practice that has struggled the most in recent years, continued to fight its way back to prominence — a trend that many are eagerly monitoring and are hoping will persist well into 2025.

State of M&A so far in 2024

For the first nine months of 2024, M&A volume rose by 18.8% year-over-year, reaching $2.5 trillion USD, with each quarter in 2024 surpassing its corresponding quarter in 2023, according to a recent report from Dealogic that examined global M&A performance. The M&A landscape appears more resilient, as the number of megadeals valued at $10 billion USD or more increased 24% in the first nine months of 2024 compared to the previous year. However, the overall number of deals decreased slightly, down 4% year-over-year.

From a regional perspective, Dealogic’s report highlights that North America experienced a notable resurgence in M&A activity during the first nine months of 2024, after a couple of unenergetic years. And even though there was a 3% decrease year-over-year in volume during Q3, M&A value exceeded $1.23 trillion USD for the first nine months, reflecting a 20% increase over the same period last year.

With this context in mind and reflecting on our previous Q2 demand estimates by segment, it suggests that even if our growth figures could’ve appeared less optimistic compared to other sources — likely due to sampling differences and limitations — analyzing the broader business and corporate environment can help us understand that the transactional landscape is becoming increasingly favorable for many, especially those law firms whose main source of growth is driven by this macro-practice group.

Is an M&A comeback on the horizon?

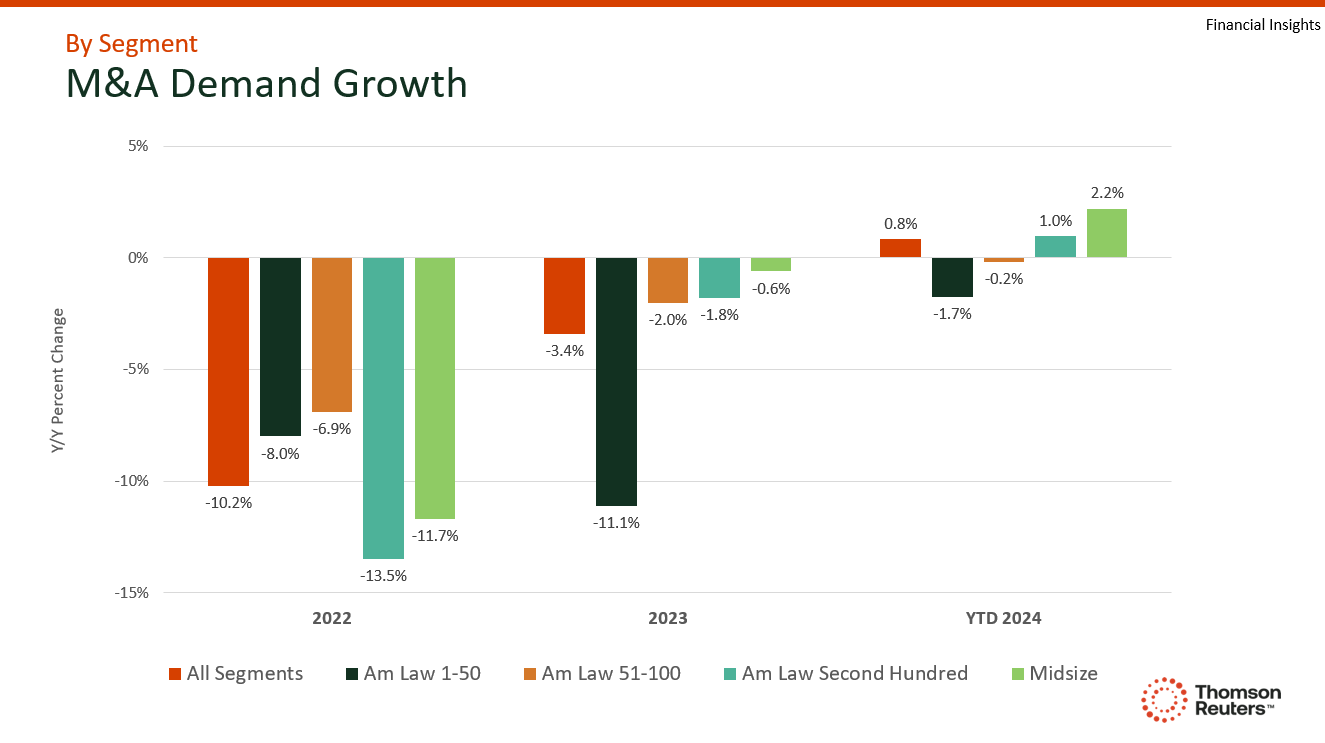

Overall M&A activity has experienced some challenges in recent years, mainly because of a slow economy coupled with high inflation, geopolitical uncertainty, and business skepticism. In 2022, the average law firm suffered a 10.2% contraction in M&A demand hours, with Am Law Second Hundred firms suffering the greatest hit. While 2023 continued to be a hard year in terms of M&A work, most segments started to move in the right direction, except for Am Law 1-50 firms.

However, the trend has continued to improve so far into 2024 and is showing no signs of weakening, with Am Law Second Hundred and Midsize year-to-date growth now sitting in positive territory after almost three years.

M&A activity is only expected to keep climbing because the needs and desires of corporate leaders to transform their businesses — due primarily to the impact of AI and to accelerate their growth in a sluggish economy — are creating more and more opportunities for M&A, according to the Institute for Mergers, Acquisitions and Alliances (IMAA). The IMAA argues that due to accumulated constrained M&A activity the pressures from both the demand and supply sides continue to rise, making a major comeback in M&A dealmaking inevitable. And it’s not a matter of if, the IMAA states, it’s a matter of when.

Indeed, the broader economic landscape might start to clear up in the coming months as well, potentially setting the stage for an upward trajectory for M&A deals in terms of both value and volume. And further expected interest rate cuts from central banks in North America and Europe could lead to greater economic activity. Additionally, the results of the US election may provide more clarity for investors regarding anticipated policy and regulatory changes, as well as sector impacts.

While uncertainty may continue to loom for some time, with the LFFI reflecting an increase in law firm hours, deal values rising, expectations about the new Trump administration becoming more positive, and economic factors continuing to trend in the right direction, a resurgence may occur sooner rather than later. Therefore, law firms should remain vigilant and be prepared to fully capitalize on these opportunities.

You can download a full copy of the Thomson Reuters® Institute Law Firm Financial Index report for the third quarter of 2024 here.