The first quarter of 2025 saw the chaos of a global trade war, but for law firms, recovering demand and record rate growth pushed them to a strong start to the year

In the final quarter of 2024, the Thomson Reuters® Institute forecasted tepid or contracting demand growth for legal services in early 2025. However, as the Thomson Reuters® Institute Law Firm Financial Index (LFFI) report for the first quarter of 2025 showed, demand grew 0.5%, beating expectations for the quarter although not matching the previous heights of 2024. This growth occurred mostly late in Q1, driven by clients who were seeking guidance amid an escalating trade war.

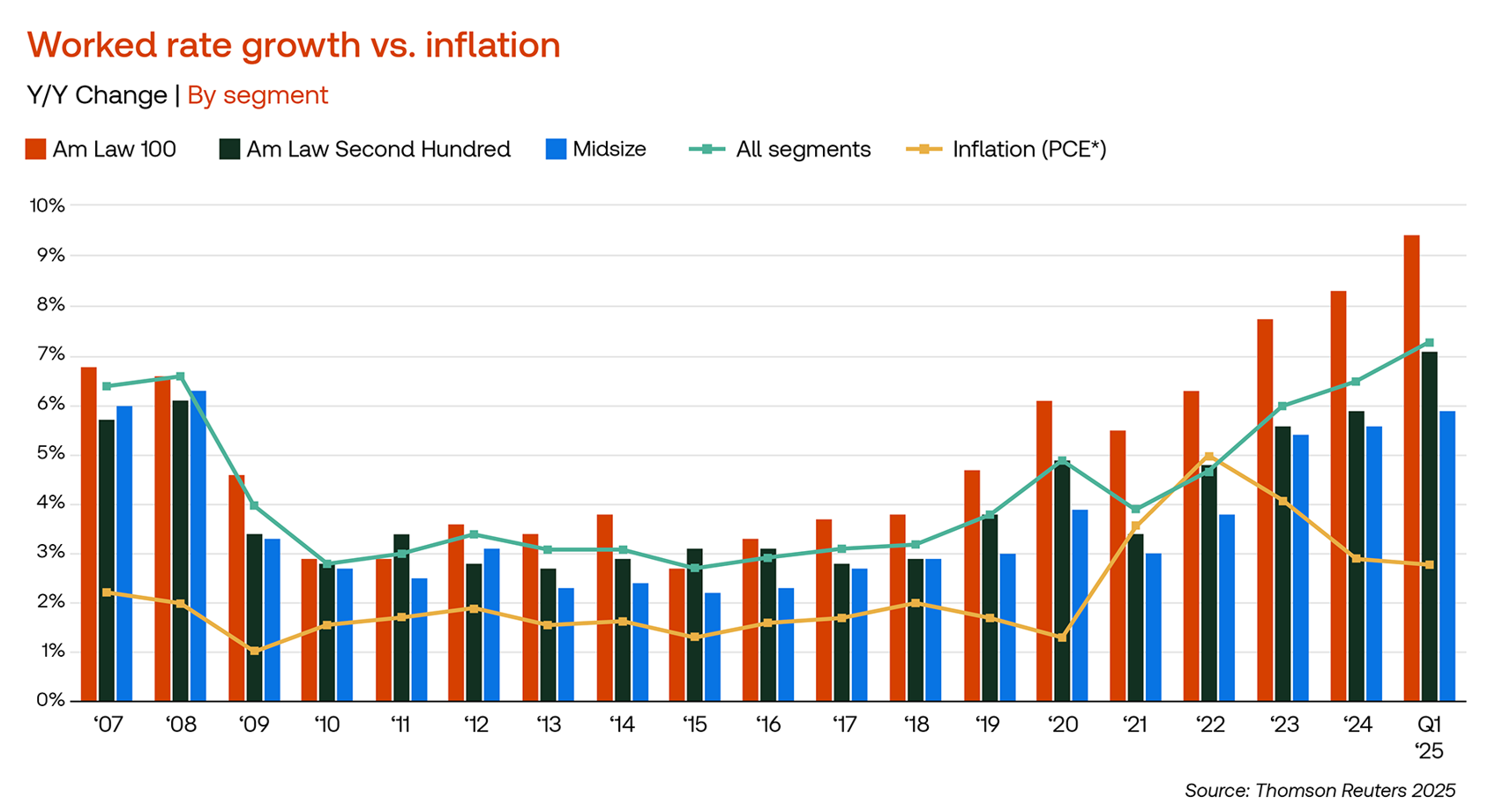

While demand growth was interesting, the LFFI’s headline was that law firms achieved record-high worked rate growth, with an average growth rate of 7.3% — surpassing the levels seen in 2008. Am Law 100 firms pursued aggressive rate strategies, nearing double-digit growth, while Am Law Second Hundred firms achieved all-time-high rate growth. Midsize firms also showed strong growth, although not at the level of the Am Law firms.

Overall rate growth is important, however, deciphering which law firm segments are most driving the acceleration in rate growth performance, compared to 2024 is really interesting. Am Law 51-200 firms appearing to be adopting the strategy that the Top 50 firms have been using for the past few years. Given that Am Law 51-100 and Am Law Second Hundred firms have generally had stronger demand growth than the Top 50 firms in recent years, this success could be emboldening those two segments to push the envelope with rates.

Am Law 51-100 firms accelerated rate growth to 9.0% in Q1, an acceleration of 1.3 percentage points compared to the 7.7% their rates grew in 2024. A similar pattern is seen with the Am Law Second Hundred, with a 1.2 percentage point acceleration from between 2024 and Q1 2025. At the same time, the Am Law 50 firms still saw some acceleration, increasing by 1.0 percentage points, to 10.2% in Q1, from 9.2% in 2024, demonstrating their continued leadership in rate strategies.

Record-high rate growth coincided with a 7.6% increase in direct expenses, surpassing the average rate growth. This trend of increasing direct expenses, which has occurred since late-2024, is partly due to the payment of performance bonuses and an intensifying talent war, with top talent demanding higher compensation. The rise in overall expenses, whether for talent or technology, likely influenced much of these rate negotiations.

The current market instability, exacerbated by the intensifying trade war, is prompting firms to reflect on the possibility of recession and remember past economic tsunamis like the global financial crisis (GFC), especially given the eerily similar environment in 2007 compared to now. Today’s uncertainty likely aids firms in negotiations, as instinct may lead clients to avoid hardball tactics with trusted partners. Instead, clients may feel compelled to seek the highest quality guidance to help them navigate this volatile climate, regardless of the cost.

How are the different segments reaching record rate growth?

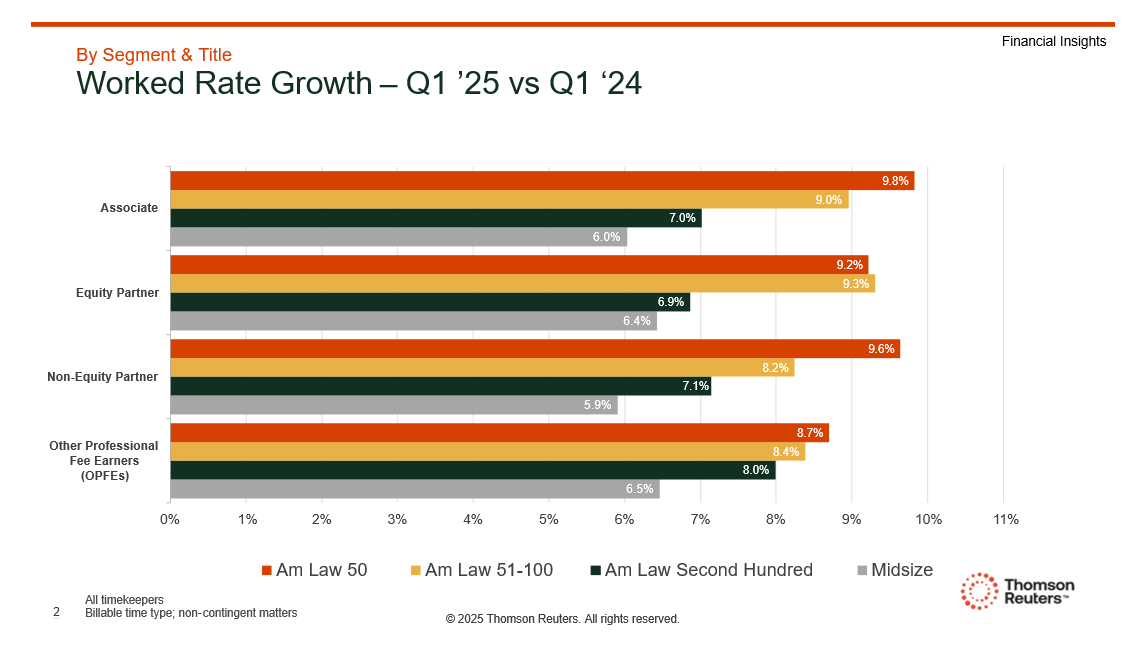

When analyzing rate growth by title, different segment strategies become more evident. Am Law 50 firms notably led in worked rate growth of non-equity partner rates in 2025, outpacing other segments by 1.4 percentage points. By contrast, Am Law 51-100 firms saw a similar pace of growth for associate and equity partner ranks. The competitive landscape for rainmakers and lateral talent, coupled with explosive non-equity partner headcount growth, indicates that Am Law 50 firms might be ensuring these investments yield returns or are perhaps a reflection of an increasing population of relatively higher-priced lateral non-equity partners.

The least division in rate growth among segments is seen with other professional fee earners, such as paralegals and specialists. Midsize and Am Law Second Hundred firms are accelerating worked rates most with this group, indicating a strategy focused on increasing rates of lower-priced hourly rate timekeepers. This approach suggests these firms’ clients are more price-sensitive or aim to limit growth in lawyer rates, making it an effective strategy for maintaining rate growth for firms outside the Am Law 100.

How are clients reacting?

Aggressive rate growth strategies often come with push back from clients, who will also be watching their expenses closely in economically unstable times such as these.

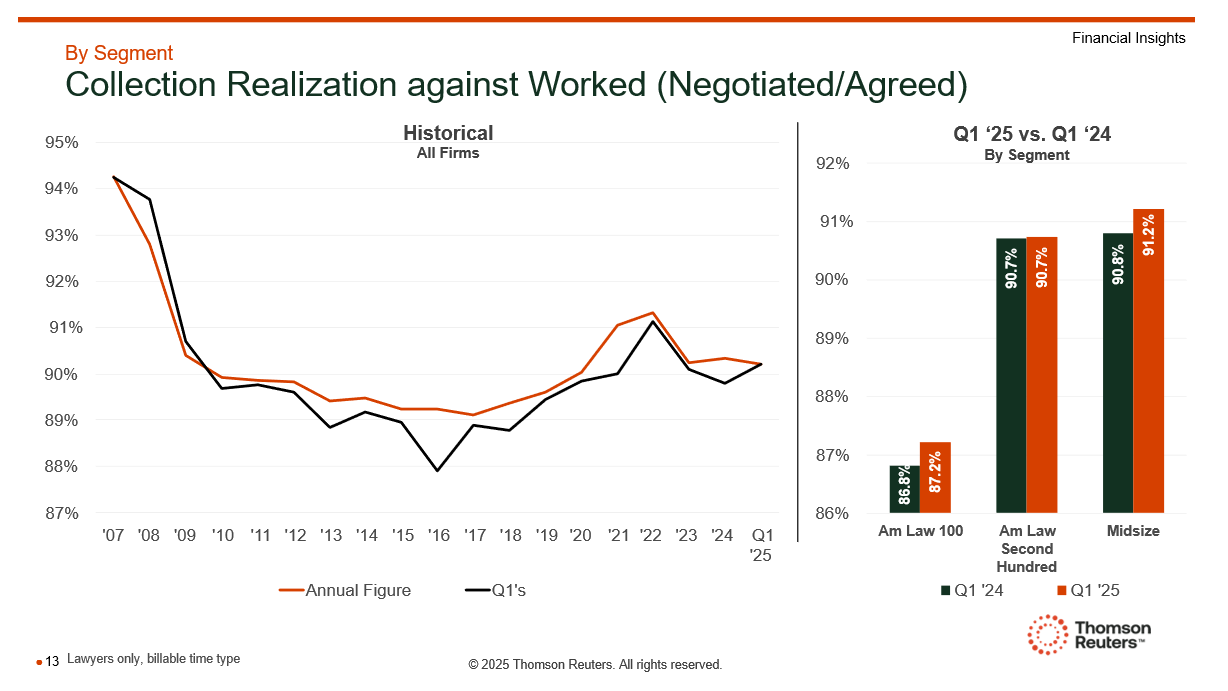

Traditionally, in the first quarter of any year, collection realization is at the low point of the year due to clients adjusting to their outside law firms’ new pricing structures. However, we have seen a noticeable uptick in collection in Q1 2025 compared to last year — the first time that we have seen this in two years. This is a welcome sign for the firms across the market: With rate growth at record highs, a high level of collection could directly boost performance.

As was outlined in the recent LFFI report, as the fires of the global trade war continue to intensify, clients seem to have bigger priorities than bargaining with the firefighters. While the increase in collection may seem small, it is perhaps the strongest positive indicator for the current pricing relationship between clients and their outside law firms.

Looking at how the markets re-started after the pandemic and the GFC show that the start of an economically uncertain period is typically accompanied by acceleration in law firm demand and rates as clients look for guidance. We saw a similar story in Q1 this year: As the trade war escalated in March, legal demand ticked up.

Of course, the concern now turns to what happens after this initial surge. History tells us that if the market does move into recession, a decline in demand and pricing power for firms tends to follow.

Looking to the rest of the year

Since 2023, law firms have seen strong profit growth, driven by growth in key practice areas like litigation, as well as strong increases in worked rate growth, and slowing expenses. The first quarter of 2025 reflects some aspects of recent successful years but also reminds us that market strengths can quickly vanish. Despite this, firms have achieved double-digit profit growth across all segments, creating a cushion for potential downturns.

If the record rate growth can continue, it will improve the performance margin that firms have in a downside scenario. Rate growth remains the main driver of profitability within many firms, so in that light, the results in Q1 are an unquestioned success.

To be sure, law firms today face a level of complexity in this dynamic environment that has each law firm segment deploying varying strategies to various levels of success. As the future remains uncertain, the ability of law firm leaders to make informed decisions that consider both financial and non-financial factors will become increasingly important.

You can download a copy of the recent Q1 2025 Law Firm Financial Index from the Thomson Reuters Institute, here