Rising rates and strong demand for services drove performance for law firms in Q1 but questions swirl around whether each trend is sustainable

There is no doubt that the first quarter of 2024 was encouraging for large law firms by just about any standard. As reported in the Thomson Reuters Institute’s Q1 Law Firm Financial Index (LFFI) report, the overall Index score rose 2 points for the quarter, driven by moderating expenses and strong growth in both worked rates and overall legal demand. Both of those latter factors merit further discussion.

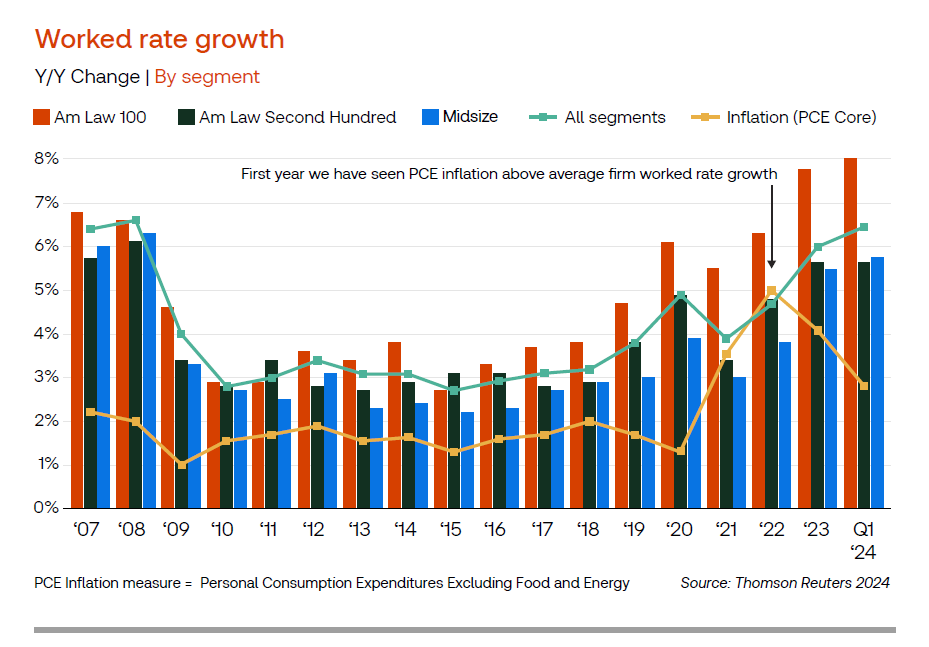

Strong rate performance continues

Full-year results from 2023 showed an interesting phenomenon in worked rates, sometimes called agreed-upon rates, which are simply the rates that are negotiated with clients. Throughout 2023, the pace of worked rate growth accelerated, growing from 5.5% in Q1 2023 to 6.5% by the end of the year. As a consequence, we did not see the jump in worked rates we typically see in each year’s Q1 — instead, we saw the continuation of that upward trajectory.

The interesting question, at this point, is whether that trend will continue. Many law firms justified their 2023 rate increases by pointing to inflation over the previous year. That meant that the rate increases firms pushed through for 2022, in many cases, actually resulted in firms ending up with diminished buying power as the rapid pace of inflation outstripped rate growth — an occurrence not seen before in the history of our data set. Consequently, many law firms were more aggressive with their rate increases at the start of 2023, and evidence suggests that focus on pushing higher rates did not soften throughout the year.

The start of 2024, however, paints a different picture. Although inflation concerns have not disappeared, the pace of inflation has notably slowed. This is posing a challenge for law firms in how they will justify their continued rate increases, creating a bit of a conundrum.

At least through the first quarter of this year, however, law firms seem undeterred. And it does not appear, at this point at least, that clients are pushing back too aggressively as revenue growth ticked up in Q1 2024 compared to the previous quarter.

Indeed, the performance of law firm rates will merit close scrutiny for the remainder of the year; however, there is no argument that the year began in any way other than strong.

Demand growth driven by litigation

The same description can also be applied to the growth in average legal demand for law firm services. The average law firm saw demand for their hours grow by 1.9% in Q1 2024. By historical standards, this is strong growth, particularly in light of the fact that Q1 2023 saw essentially flat demand performance, meaning this year’s Q1 was building off a relatively stable baseline.

It was not long ago that we would write about 1.9% demand growth using bold fonts and banner headlines, as the market tended to hover between -1% demand contraction and 1% demand growth for several years.

However, while last quarter’s demand growth number is impressive in its own right, and what makes for an even more interesting story is the driving force behind that performance. Counter-cyclical practice demand remains strong, with bankruptcy and labor & employment practices posting 3.0% and 1.0% growth in Q1 2024, respectively.

The undisputed demand champion for the quarter, however, was litigation work, which grew by an impressive 3.8% for the quarter. Notably, that growth comes on top of 2.4% growth in litigation work in Q1 2023 meaning the market experienced strong growth on top of strong growth. Given that litigation makes up slightly more than one-quarter of the overall total of billable hours tracked, that pace of growth provides a ready explanation for the 1.9% bump in overall average demand for the quarter.

The bump, however, was not a tide that lifted all boats equally. For Am Law 100 firms, litigation demand grew by a reasonable average of 1.2%. Standing alone, that figure would seem relatively strong; however, it was greatly overshadowed by the Am Law Second Hundred segment, which enjoyed litigation demand growth of 5.2%, and Midsize law firms which saw litigation demand growth of 4.7%. Notably, this marks the third consecutive Q1 in which Midsize law firms posted litigation demand growth at or above 3.4%, a remarkable period of strong growth in a practice that struggled to find growth for much of the prior decade.

Continued strong performance for law firm rates and counter-cyclical practices will likely be key to law firm financial performance throughout the remainder of this year. There are indications that transactional practices could make a bit of a comeback as corporate work stepped into positive territory with 0.6% growth in Q1 2024, but uncertainty around the US presidential elections, interest rates, inflation, and the broader economy could cause businesses to hold back on any major transactional moves. Consequently, law firms will likely be looking to maximize those practices that they see as their current growth drivers.

You can find more about the Thomson Reuters Institute’s Law Firm Financial Index (LFFI) reports here