Market conditions are pushing many law firms away from moderate demand growth, giving way to dramatic redistributions across demand growth tiers, with middle-ground performance levels experiencing unprecedented erosion

Key takeaways:

-

-

-

Higher polarization is seen — Stable growth levels contracted across all segments, forcing them toward polarized outcomes and eliminating the comfortable stability seen in 2024.

-

Not all firms were equal — While some law firm segments experienced a downward migration toward underperformance, others demonstrated an exceptional upward trajectory.

-

A buffer may be in place — Those firms seeing declining performance tended to concentrate on modest negative levels rather than experiencing severe downturns, suggesting that current market conditions are creating a buffer against sharper declines.

-

-

While the Thomson Reuters® Institute’s Law Firm Financial Index rose in the second quarter of 2025 amid increase legal demand, the overall metrics suggested stability, with clients turning to their outside law firms for guidance. Indeed, the quarter looked unnaturally smooth.

Yet this surface-level tranquility masks a far more dynamic reality. We can examine how individual firms performed by calculating demand growth for each firm and grouping them into six buckets:

-

-

- severe decline (more than 10% decrease)

- moderate decline (between 5% and 10% decrease)

- modest decline (between 0% and 5% decrease)

- modest increase (0% to 5% increase)

- solid increase (5% to 10% increase)

- exceptional growth (more than 10% increase).

-

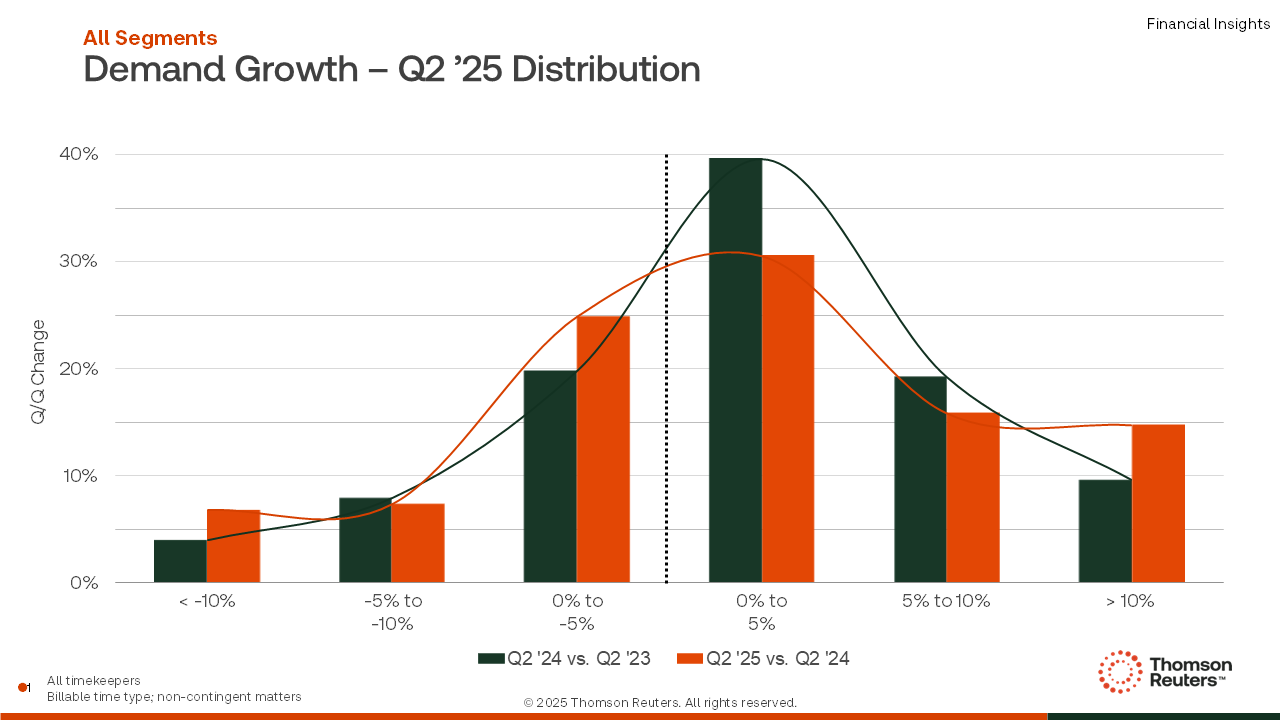

When examining all law firm segments, the data distribution provides compelling evidence for a clear movement. The moderate increase range, which served as the stable foundation for law firm performance, experienced significant erosion as nearly one-quarter of firms were pushed out of this comfortable middle tier. The most notable trend shows industry dynamics driving firms toward two distinct outcomes: exceptional growth at the high end and modest decline clustered just below break-even.

Geography plays a key role in how firms are performing. More firms in the Northeast, Southeast, and Southwest regions are seeing strong growth, while firms in the Midwest and West are showing signs of slower performance and diminishing middle-ground results. Meanwhile, firms with international exposure faced volatility, especially among lower-growth ranges. Interestingly, this volatility seems to create a natural limit to how much performance can drop, helping some firms avoid more severe declines and show a measured response to outside pressures.

However, these overall trends hide important differences between law firm segments. Each group saw unique shifts, showing how similar conditions led to very different results depending on the firm’s size and market position.

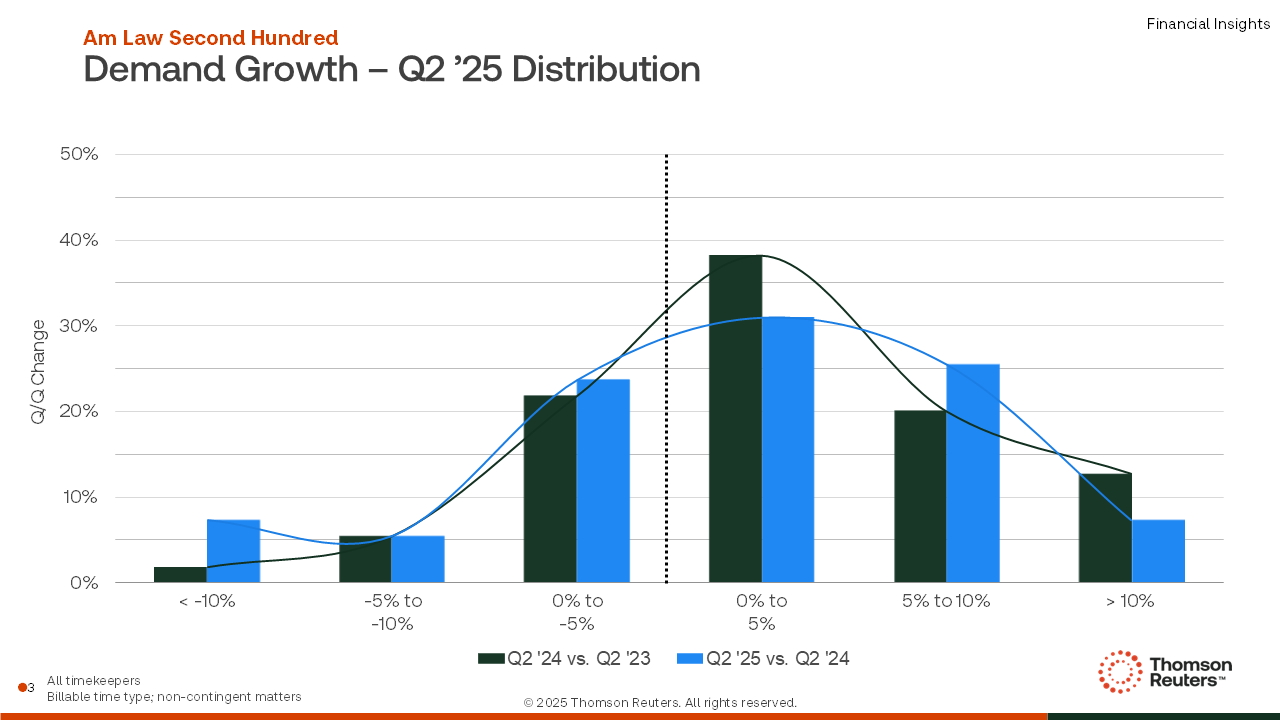

Am Law Second Hundred: Polarization at the extremes

The Am Law Second Hundred responded differently to today’s market pressures. Instead of moving in a single direction like other law firm segments, firms in this group were pulled toward both strong growth and weaker results. The middle range, which was once more stable, has narrowed, and its share has been redistributed across the full spectrum of outcomes.

Many firms that were growing exceptionally fast are now settling into more stable performance levels, suggesting that earlier peaks may not have been sustainable. Rather than abrupt changes, the general trend is moving towards a more stable pattern, albeit with a concerning rise in the number of firms encountering significant declines.

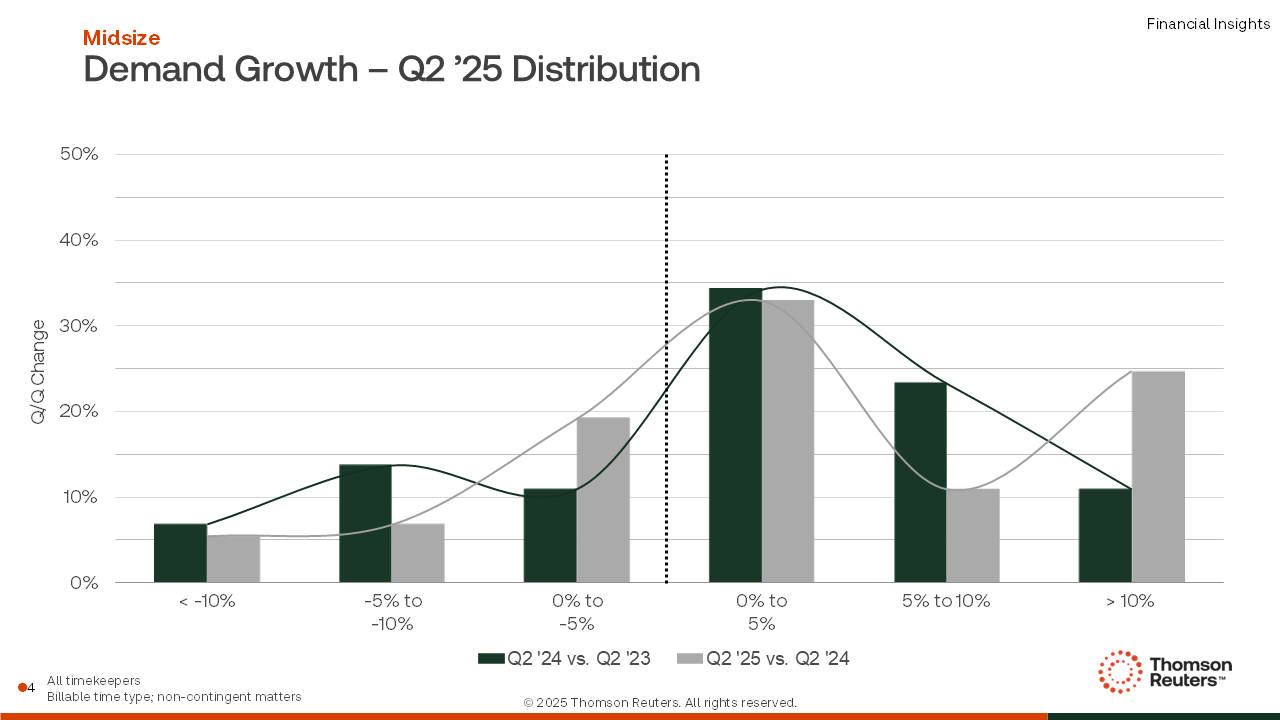

Midsize firms: The upward trajectory

While the Am Law Second Hundred showed a more balanced spread of results, Midsize firms moved sharply upward. Market conditions pushed many of these firms into top performance, with the number of high achievers more than doubling. At the same time, fewer firms struggled with serious challenges. What stands out most is that many firms jumped straight from steady growth to exceptional results, skipping the usual gradual progress.

Current industry dynamics have helped many Midsize firms move from moderate to stronger growth. This change wasn’t the result of a new strategy, but rather the outcome of earlier investments in talent that now fit well with today’s environment. Further, Midsize firms more limited international exposure, stronger focus on litigation, and lower rates may be contributing to this standout performance that has set them apart from the next group of firms.

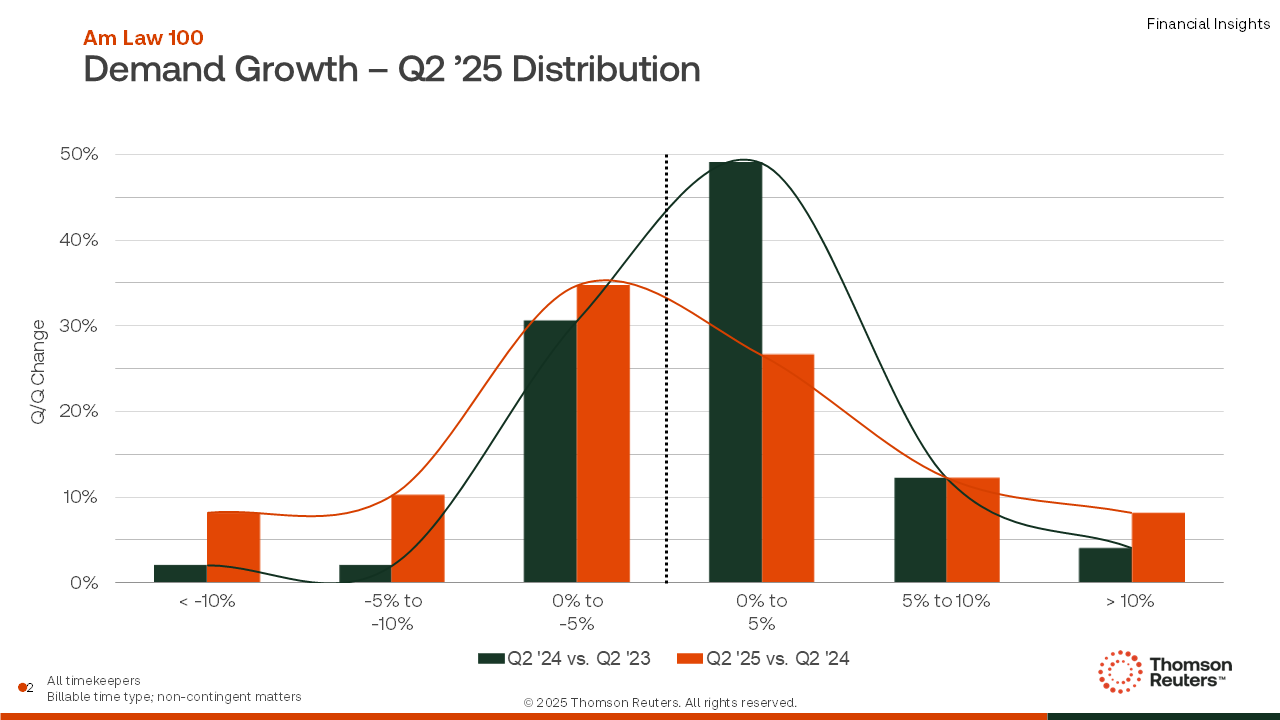

Am Law 100: The downward drift

The demand growth data for Am Law 100 firms shows a clear shift in how performance is spread. The biggest change happened in the moderate growth category, in which nearly half the firms were pushed out of what used to be a stable zone. This shift shows that more firms are ending up with weaker results, while only a few are seeing strong gains. The number of firms with declining performance has increased quickly, and those doing exceptionally well are too few to balance out the overall drop.

The way performance is spreading across Am Law 100 firms shows that steady, moderate growth is becoming harder to maintain. Factors like international exposure, slower hiring, and changes in client needs seem to be pushing firms toward either strong results or weaker demand, with fewer staying in the middle. These conditions are making competition within this group more intense.

The legal market’s current reality

In the second quarter of 2025, the legal market continued to evolve, with different types of firms reacting in their own ways to changing conditions. While the LFFI rose and pointed to general stability, beneath that surface, many law firms are being affected by new pressures: stronger competition, a differing client mix, and overexposure to certain markets — all of which are creating a wider gap between top performers and those firms on the lower rungs.

Focusing clients at the center of business decisions is becoming more important for long-term growth; and each segment-specific pattern demonstrates how firms are finding different pathways to achieve this goal. For example, Midsize firms are doing well, likely because their flexible operations fit the current environment; and the Am Law Second Hundred is holding steady, showing that a mix of business models can help those firms adjust to outside pressures. Meanwhile, the difficulties facing Am Law 100 firms seem to come more from structural shifts and adverse operating conditions than from strategic missteps.

The evolving dynamics within the legal industry suggest increased fluidity. Whereas law firm financial performance in recent years has been influenced primarily by broad macroeconomic trends, current conditions are shaped by volatile policies and geopolitical developments, resulting in diverse business conditions across clients, regions, and industries. These shifts present both heightened risks and new opportunities, making it essential for leaders of law firms of all sizes to assess their positioning in preparation for potential challenges ahead.

You can get a fully copy of the Thomson Reuters® Institute’s Law Firm Financial Index for the second quarter of 2025 here