Worked rate elasticity remains exceptionally strong, but emerging pressure on client budgets suggests that the profit engine which powered firms through 2025 may face tighter constraints in 2026

Key takeaways:

-

-

-

Worked rate momentum is slowing at a crucial time — Q4’s 7.1% growth in worked rates, while historically strong, is the smallest quarterly increase of 2025, indicating the rate‑driven profit engine may not be endlessly responsive as firms approach 2026.

-

Elasticity at its strongest and most vulnerable — Since late-2022, worked‑rate growth has translated almost one‑for‑one into law firm profitability, but even a slight softening in rate momentum now poses outsized risks as client budgets tighten.

-

History shows the system has limits — The 2021– ‘23 period demonstrated that rate growth alone cannot sustain profitability. Today’s Formula 1‑level responsiveness boosts gain quickly enough, but it can leave firms more exposed if the market changes direction.

-

-

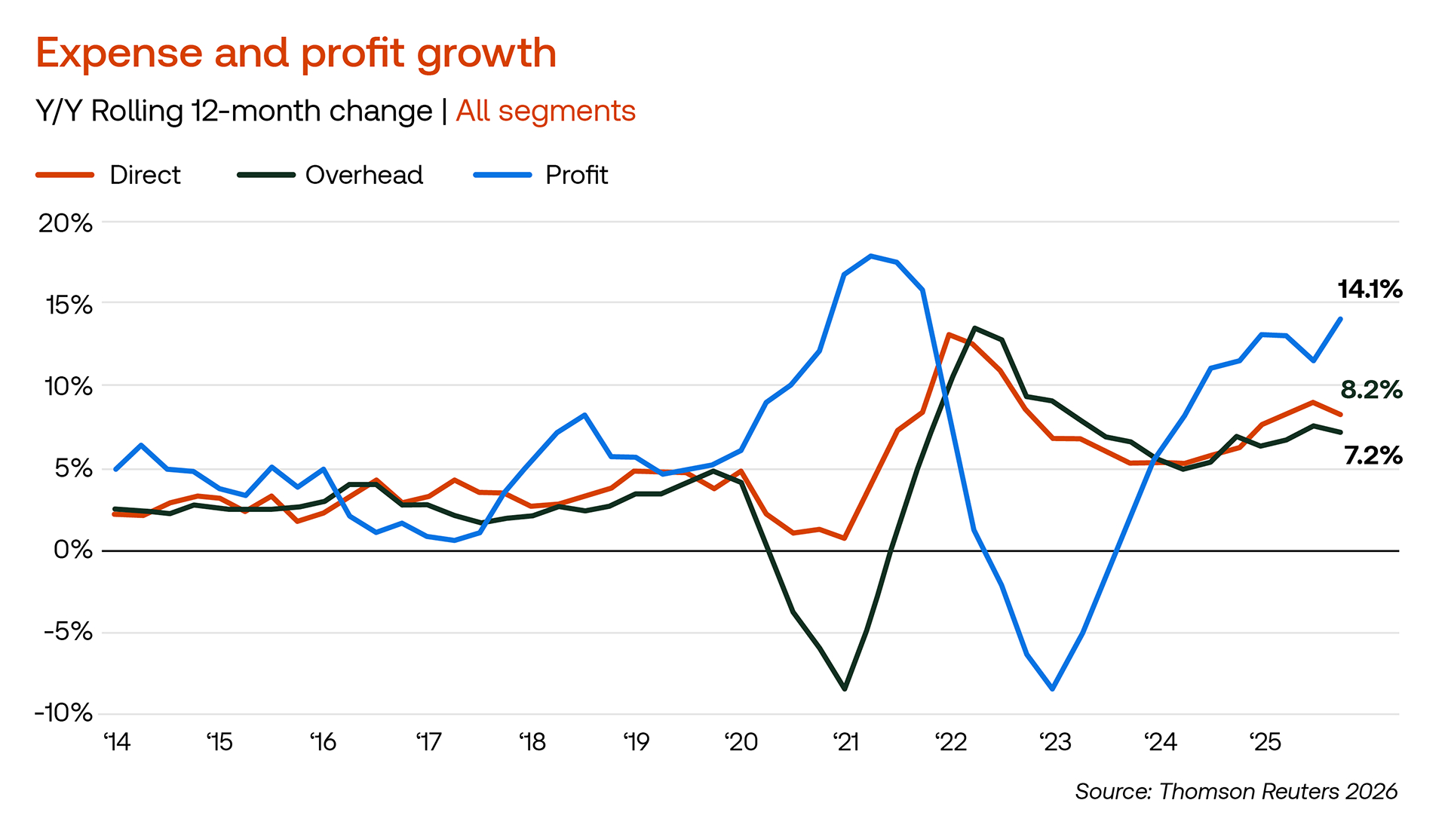

Even as the winds shift, law firms still managed to sail into a strong finish in the fourth quarter of 2025; but beneath that smooth landing, the current was already changing direction. As the Thomson Reuters® Institute’s Law Firm Financial Index (LFFI) edged down 2 points to 61 in Q4, a small but notable reversal after a full year of steady gains. The dip was driven largely by cooling demand growth, and while modest in absolute terms, it hints at a broader realignment that may be taking shape just as the industry steps into 2026.

Unsurprisingly considering its role in profitability, much of this shift comes down to worked rates and their relationship to profitability — a relationship that, in recent years, has been remarkably tight. Yet Q4 showed the first signs that the market may be entering a more complicated phase.

The F1 machine

In the previous decade, the rate-driven profit engine behaved more open, stable, predictable, and generally comfortable — albeit with one important limitation. It didn’t offer much acceleration. In fact, most of the higher‑velocity gains only began to appear as the industry approached the pandemic era. Then, when the pandemic hit and the system started to strain, with any acceleration felt weighed down and less responsive as firms navigated uneven pavement and constant adjustments.

Beginning in 2023, the industry shifted again — this time with the acceleration power of a Formula 1 race car. Rates became extraordinarily efficient in being translated into profitability. In recent quarters, profit rates have seen significant growth, so when firms pressed the accelerator, the needle moved quickly.

However, an F1 car demands precision. The faster it goes, the less margin there is for error. Today, the market is operating in a phase in which rate increases translate to profit gains at incredible speed.

A decade of history reveals a crucial pattern

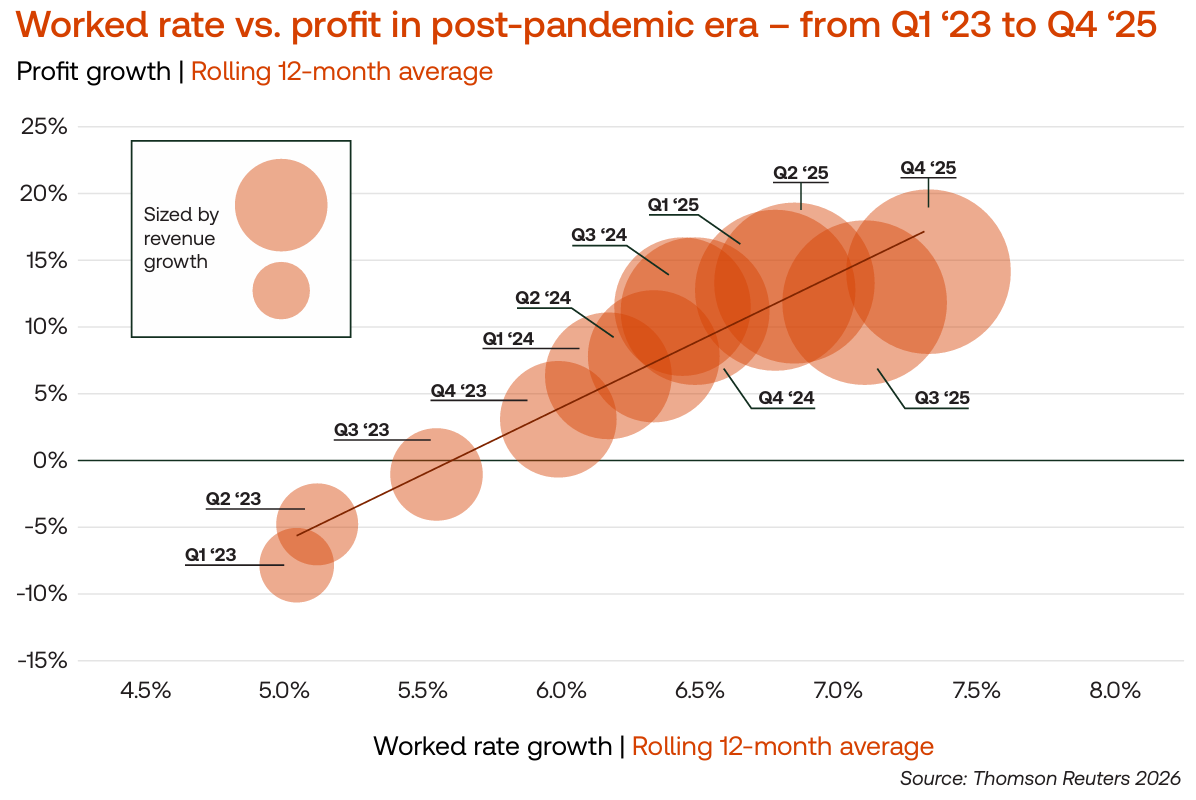

The chart above broadens the lens to cover more than 10 years of data, bringing an important nuance into focus. The relationship between worked rates and profitability has not always been as linear — or as reliable — as it has in the most recent period. From Q1 2015 to Q4 2021, firms were driving at a manageable pace: For every 1% increase in worked rates, there was an approximate 0.7% growth in profit. Indeed, most of the historical data aligns with the intuition that higher rates bring higher profits.

However, between Q4 2021 and Q1 2023, the pattern bends in the opposite direction. Rate growth accelerated sharply, yet profitability declined. At first glance, it appears counterintuitive, but in racing terms, the track conditions had deteriorated sharply, making speed alone not just ineffective but actually risky. This was a period marked by elevated inflation, rapid expense growth, compensation escalations, and operational volatility across many law firms.

The logic was simple: Even aggressive rate increases couldn’t fully offset the pressure on margins. Moreover, in such a strained environment, attempts to raise worked rates by 1% led to a nearly 0.9% decrease in profits — almost a complete reversal. As a result, firms were recording some of their highest worked rate growth levels in nearly a decade, yet profitability on a rolling 12‑month basis dipped into negative territory and remained there for several quarters.

The goal of discussing this period isn’t to argue that rate increases backfired. They technically didn’t. Rather, the lesson is more subtle… and more relevant today: Rate growth is essential, but not omnipotent. It cannot solve every profitability challenge on its own.

The more recent elasticity story: Rates and profit move together

The LFFI’s softening in Q4 was influenced not only by decelerating demand growth, but also by a subtle easing of rate growth’s momentum. Worked rates grew 7.1% for the quarter — as we said, still strong, but the slowest quarterly increase of 2025. In a different era, this might have been a footnote; however, since the pandemic, rate growth has become the central pillar supporting law firm profitability. Where productivity and demand once balanced the equation, rates now serve as the primary driver. This means that any moderation, even a slight one, carries outsized significance.

The chart above illustrates this dynamic clearly. Without belaboring the mechanics, each point represents one quarter, with worked rate growth on one axis and profitability on the other, both on a rolling 12‑month basis. The clustering shows a close, consistent linkage over the last several years, showing that as rate growth pushed steadily upward, profitability almost invariably followed.

One takeaway stands out, however. Since late 2022, every 1% increase in worked rates has corresponded with roughly a 0.9% increase in profit growth, contrasting sharply with the patterns observed during the pandemic period. That kind of elasticity is rare in the history of the legal industry, and it helps explain why 2025 was such a profitable year across the market. Firms exceeded a two‑decade threshold in rate growth, achieving average increases near 7% and double‑digit gains at the top end.

Again, however, that relationship cuts both ways. If rate growth were to stall — or if clients were to push back more aggressively on rates — the profit engine that has powered firms through much of the last three years could lose momentum quickly. The early signs of that tension were already present in Q4, and they could intensify in 2026. Corporate budgets are under acute pressure, and counter‑cyclical demand often rises during economically turbulent periods, tightening constraints even further.

Put simply, the market is showing early signs that clients’ ability to absorb further rate increases may clash with firms’ dependence on that rate growth to sustain their profit growth. And the years of historical data serve as a reminder that this relationship isn’t unbreakable, and that even well‑calibrated systems can behave unpredictably when conditions shift.

The real question heading into 2026 is not whether firms can continue pressing the accelerator, but whether they can do so safely. At this Formula 1 speed, maintaining profitability isn’t just about adding power — it’s about navigating a track that is becoming narrower, more volatile, and far less forgiving.

You can download the Thomson Reuters Institute’s Q4 2025 Law Firm Financial Index here