The second quarter of 2025 continued where the first left off, with strong revenue growth — but with expense growth continuing to accelerate and showing no signs of slowing

Key findings:

-

-

-

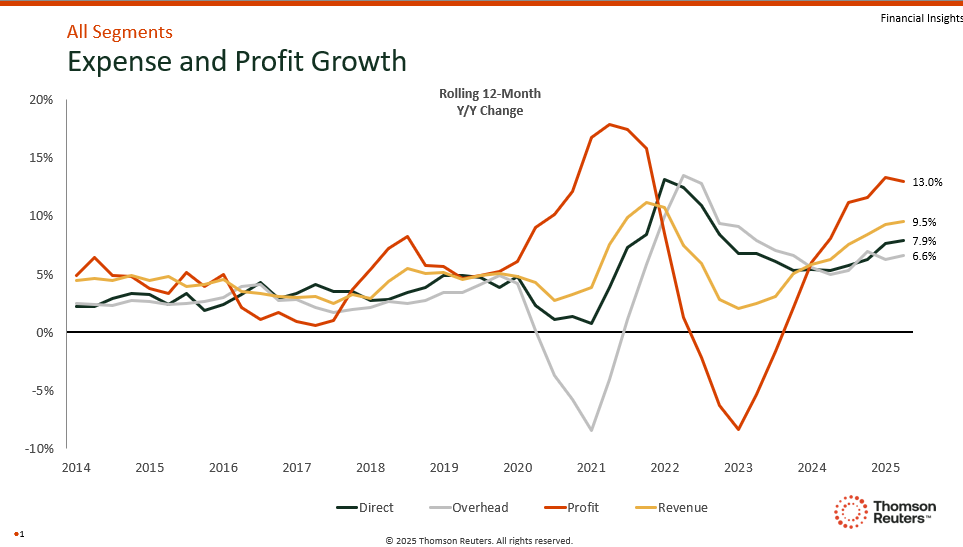

Expense growth is accelerating — Both direct and overhead costs are rising faster than in Q1, posing a potential risk if revenue growth slows.

-

Law firms are adapting strategically — With Am Law 100 firms leveraging pricing power over headcount expansion, other firm segments are investing in technology and smarter resourcing to manage costs.

-

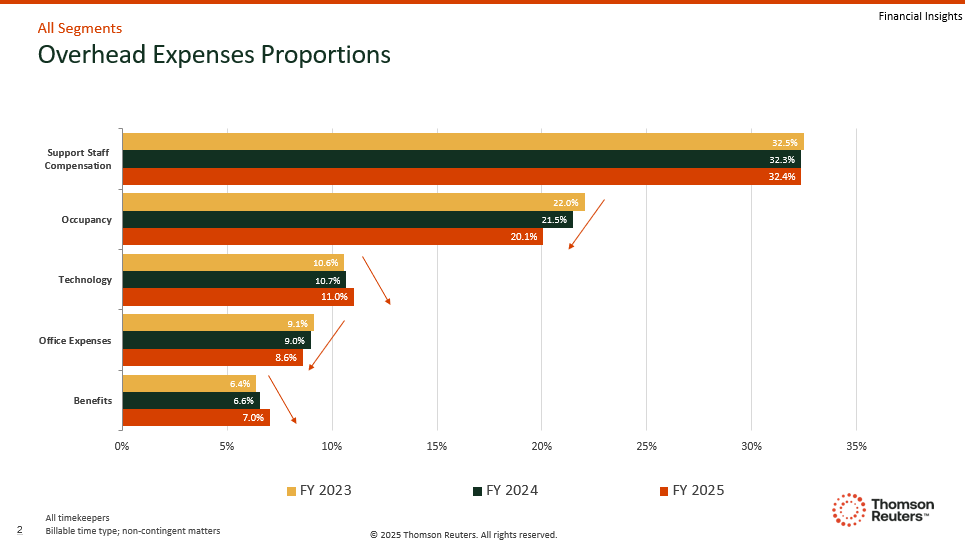

Overhead spending trends are shifting — Increased investment in tech and benefits, and a decline in occupancy costs are signaling a move toward hybrid work and operational efficiency.

-

-

The story of 2025 has been the ongoing trade war, which has driven uncertainty around global economic and policy matters. Coupled with rising geopolitical instability, the situation has left economists and business leaders holding their breath. Yet the US legal market’s second quarter was unexpectedly calm — and surprisingly prosperous, according to the Thomson Reuters Institute’s Law Firm Financial Index for Q2, which rose as more clients turned to their outside counsel for guidance.

This rise can be attributed to an increase in legal demand of 1.6% and robust worked rate growth of 7.4%. Together these gains offset a 1.3% productivity decline. While these topline gains are encouraging, law firm leaders should remain vigilant on the expense side.

Both direct and overhead expenses saw a modest increase in growth this quarter compared to Q1, rising to 7.9% and 6.6% respectively, continuing a trend underway since the second half of 2024. Revenue growth is still outpacing expense growth, keeping profits strong, but any slowdown in revenue could leave firms in a lurch, just like we saw in 2022.

After the robust level of demand and rate growth of the first half of 2025, an increase in spending might have been expected heading into the rest of the year, as law firms continue to chase the opportunities in front of them. However, the broader instability shows no signs of easing, suggesting continued volatility across the global market that will eventually impact firms.

This may leave firms stuck between a rock and a hard place — the strength of the legal market offers opportunities for growth; however an increase in spending in that push for growth could leave firms overexposed to a slowdown if clients may become reluctant to spend. This means firms should consider ways of slowing expense growth in other areas, in order to be able to continue to invest in their growth strategies.

Breaking down direct expense growth

When looking at how firms can limit their direct expense growth, one option that should be considered is to adopt the same strategy observed among Am Law 100 firms since 2023. While direct expense growth is at 7.9% for the market, the Am Law 100 firms saw a slower growth rate at 6.9% as these firms have limited their headcount growth.

Reducing hiring classes and stricter performance management is one of the easiest ways to slow direct expense growth, but it has opportunity costs. As previously mentioned, legal demand remains strong so law firm leaders will not want to miss out on the chance to increase their market share. Indeed, the Am Law Second Hundred and Midsize firms have seen much greater success by seeking to expand their market share in recent years.

Other options such as reducing compensation packages or cutting benefits are unlikely to be successful solutions for firms because those solutions may see talented individuals leave and dampen firm morale amid an ongoing talent war. With very little wiggle room on the direct expenses to maneuver, one way to slow expense growth will rely on leveraging process improvements, technology, and smarter resourcing — not pay cuts.

Changing overhead expense trends

Over the past three years, the proportion of firms’ overhead expenses has seen shifts as well, indicating a change in priorities. The proportion going to occupancy and office expenses has been trending downwards, while technology and benefits expenses have been on the rise.

Rising technology spend will not surprise firm leaders; it’s widely seen as essential to long-term efficiency and profit margins. In fact, many law firms have shown a willingness to invest, especially in AI driven tools. Certainly, leadership will want to see a return on these investments — and if results are not produced or are not at the levels expected, firms could be tempted to cut their losses and scale down investment into technology, especially in the event of an economic downturn. Given the arms race brewing around these tools, however, such pullback may reduce the long-term competitiveness of the firm.

Occupancy’s share of overhead expenses has decreased by 1.9 percentage points in recent years, suggesting that even while firms pushed for a full return to the office, commercial real estate costs have not kept up with revenue growth. With long‑term office leases up for renewal and negotiation, leaders may again embrace a shift toward broader hybrid work to further increase those savings.

Support staff compensation has remained at almost one-third of all overhead expenses, maintaining essentially the same proportion of overhead expenses over the last three years. That does not tell us the full story, however, as support staff covers several different functions for law firms and the growth and the changes in those areas tell us about what business functions firms are prioritizing.

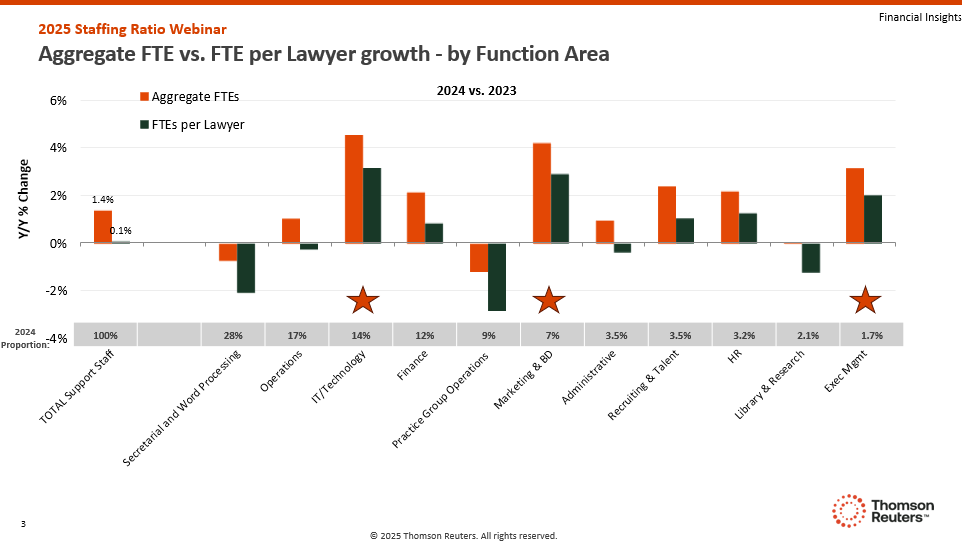

The Thomson Reuters Institute’s Staffing Ratio Survey indicates that the growth of full-time equivalent (FTE) support staff per lawyer mirrors broader overhead trends — one which emphasizes technology, business development, and management roles. Firms are focusing on improving internal business processes to better support lawyers, with the aim of enhancing efficiency and quality across their operations. At the same time, functions that are declining are in more manual-task roles such as word processing and research, signaling that technology investments have been delivering tangible results to the bottom line. This shift is particularly significant because word processing staff constitute the largest share of support staff at 28%, down from 36% in 2016.

What is next for the legal market?

Despite — and partly because of — a turbulent economy, the US legal market remains resilient, posting another quarter of continued demand growth and robust worked rate increases. Yet the memory of rapid expense inflation is fresh for law firm leaders, and with ongoing trade tensions and geopolitical uncertainty, the threat is real.

As firms choose expense strategies, they must balance supporting short-term opportunities with long‑term sustainability. Actions such as cutting headcount can lift near‑term margins but risks leaving firms under‑resourced when growth returns, given the time required to ramp up headcount. Data suggests that firms are willing to invest in process and productivity improvements, which may increase near‑term pain to secure longer‑term gains.

In the second half of 2025, leadership decisions made amid volatility will be pivotal. Firms that pair disciplined cost control with smart, forward-looking investment will be best positioned not only to weather the pending storm but to accelerate when conditions improve.

You can get a fully copy of the Thomson Reuters® Institute’s Law Firm Financial Index for the second quarter of 2025 here