How will creeping inflation impact law firms' ability to raise their rates, which has become their go-to method of enhancing revenue and profit growth?

The 2022 Report on the State of the Legal Market, produced by the Thomson Reuters Institute and the Center on Ethics and the Legal Profession at Georgetown University Law Center, provides detailed analysis of some of the problems facing the legal industry, but raises questions regarding others.

The impact of inflation on law firms is one such question. The ability of firms to raise their rates in an inflationary environment should be a top concern. Law firms have predominately relied on raising their rates each year as key means of improving profits, as opposed to increasing the hours their firm works, on average. Therefore, depletion of the value of hours worked is a significant threat to the average law firms’ finances, especially when it could eliminate multi-year gains relatively quickly.

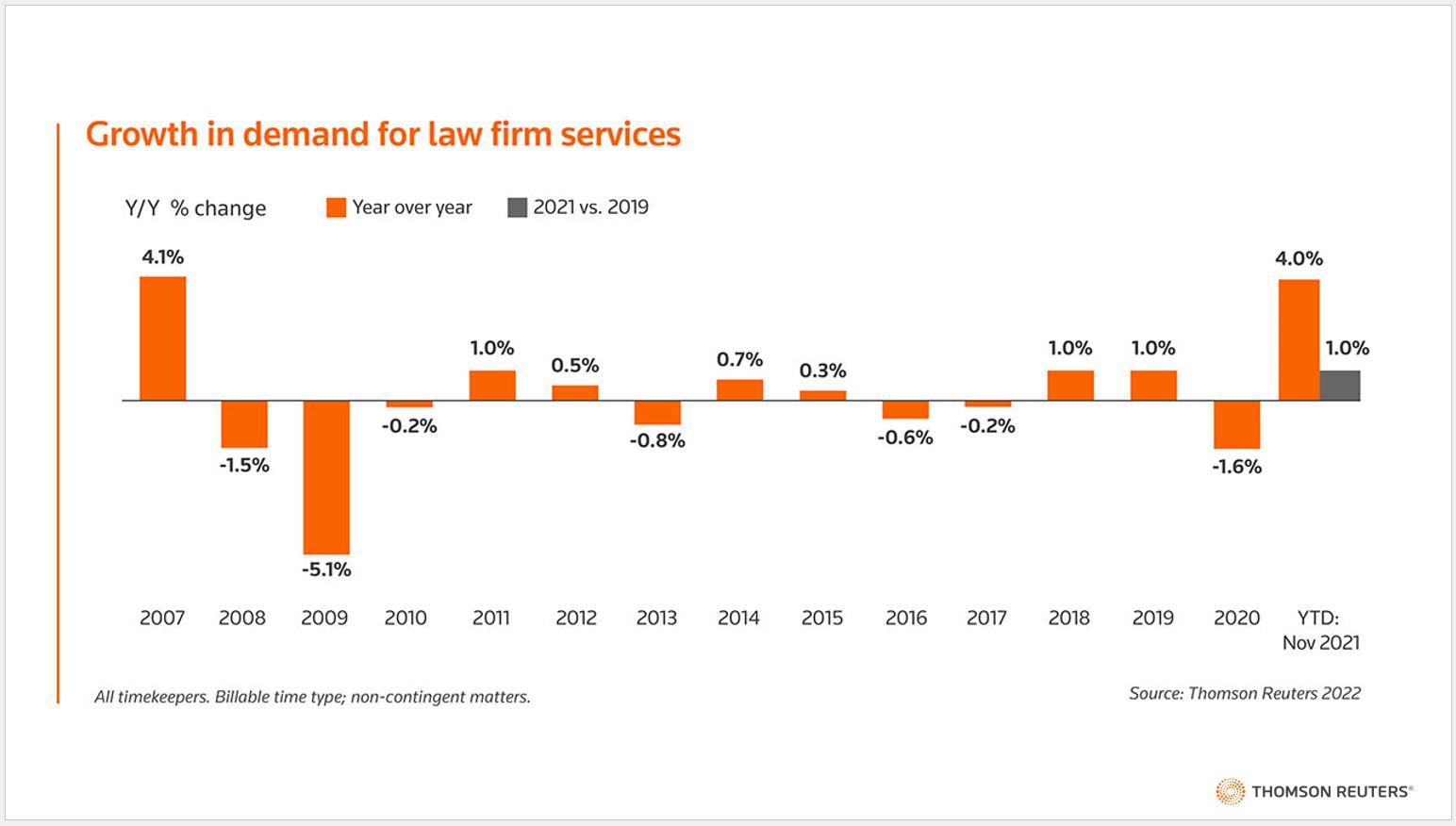

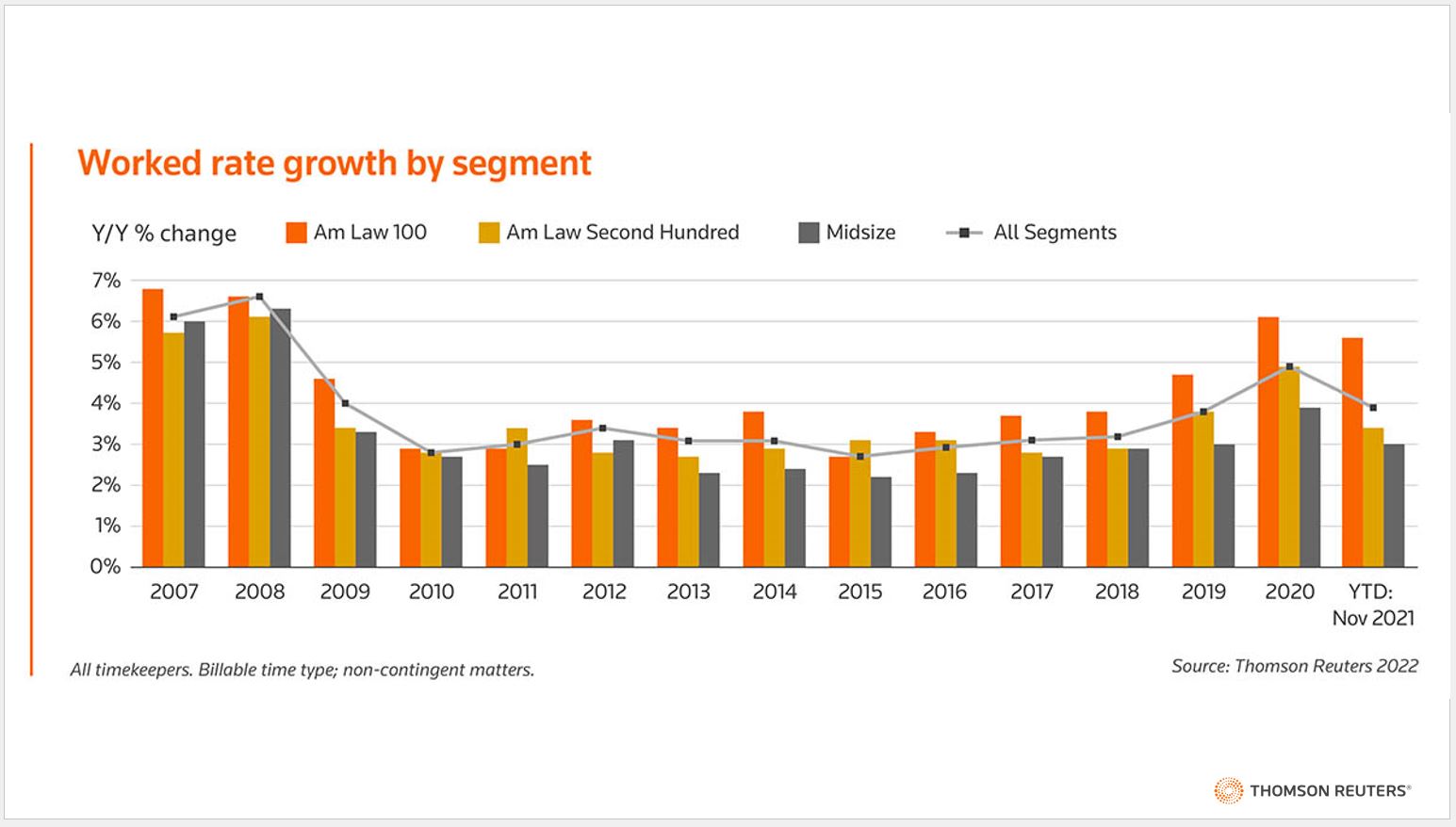

As you can see in the charts below, growth in demand (billable hours worked) remained essentially flat for most of the past decade. At the same time, worked rates (the rate which a firm and a client negotiate for a specific matter) have consistently grown above 3%. Historically, when firms are trying to earn real revenue — that is, revenue growth that outpaces inflation — rate increases are the tried-and-true source.

Typically for firms, new rates are put into effect in January or at some other fixed point in the calendar and are maintained for the rest the year. This ubiquitous trend explains why, when the pandemic first gripped the US in late March 2020 and rates jumped from 4.1% growth in Q1 to 5.2% in Q2, we knew the culprit wasn’t firms taking opportunistic advantage of their clients but rather something more complex working under the surface.

For a complete discussion of the current state of the legal market, you can download a copy of the 2022 Report on the State of the Legal Market here.

What we discovered was an underlying shift in how work was distributed, with a greater amount of work being done by higher-cost timekeepers, driving average rates up, without necessarily driving individual timekeeper rates upward to nearly the same extent.

Discovering this underlying shift led to another question: When would this trend reverse?

When 2021 began, we were already seeing evidence in our data that these swings were starting to unwind. Rate growth dropped from 4.7% average growth in Q1 2021, to 3.4% year-to-date by Q2, the lowest mark since 2018. This historical context is important because 2022’s rate measurements won’t have to deal with these dramatically fluctuating baselines, giving us a much cleaner look at how much law firms are actually raising their rates. This historical context helps explain what we see when comparing rate growth to inflation.

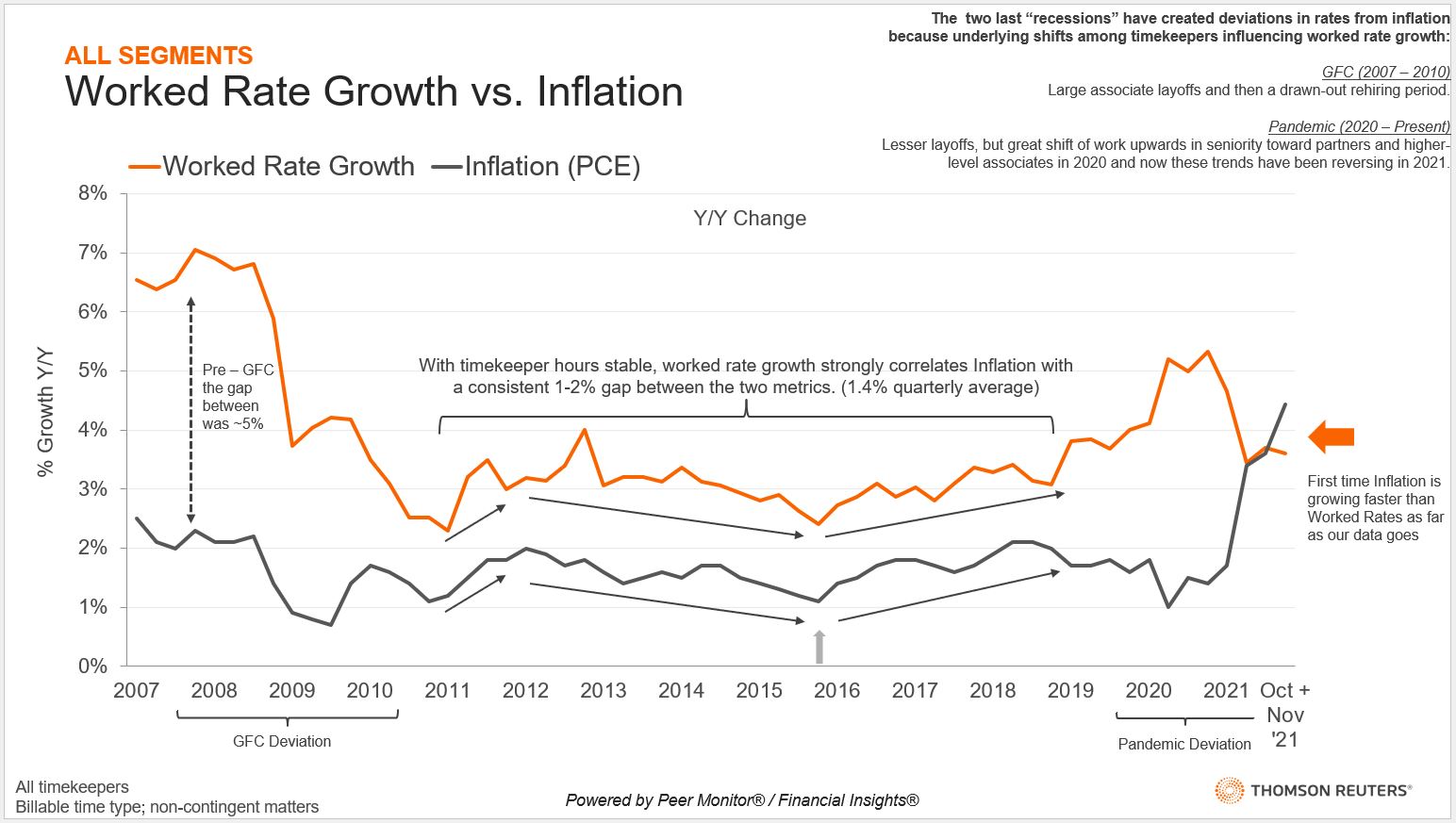

For the past decade, as law firm timekeeper staffing and hours distribution remained in relative stasis, law firms captured real rate growth of 1 to 2 percentage points above inflation. Worked rates and inflation (per the Personal Consumer Expenditure (PCE) calculation from the Federal Reserve) track in near parallel.[1] The correlation broke down during the global financial crisis that began in 2007 as well as during the pandemic. This was because both of those periods saw similar shifts within law firms regarding who was doing the bulk of the work.

Another interesting note regarding the financial crisis is the lasting impact it seems to have had on the advantage that worked rates had enjoyed relative to inflation. Before the financial crisis, real rate capture was near 5%. Following the financial crisis, average worked rate growth ranged from 3% to 4%, and firms settled into the more modest 1% to 2% real rate capture advantage relative to inflation until well into 2019.

In 2021, we saw overall hours increase dramatically while the talent to work those matters struggled to keep up, especially in the red-hot corporate practices. This was the result of a classic supply and demand issue, where law firms’ capacity to meet corporate demand was exceeded, and rates increased accordingly, as seen by worked rate growth in 2021 above 5% maintained by Am Law 100 firms. As opposed to during the financial crisis, worked rates seem to have fared much better.

Further, the rise of realization rates discussed in the State of the Legal Market Report also potentially signals a relaxation of client pushback on rates.

We should also address a bit of an elephant in the room with the graphic above: Inflation ramped up so quickly during the second half of 2021 that many law firms had very little chance to react. As a consequence, worked rate growth currently lags inflation for the first time in the history of our data set.

Between the threat inflation poses and the ever-increasing costs of the escalating talent war, there are plenty of incentives for firms to push the envelope with regard to rates. With all this in mind, the data suggest it would not be beyond the pale should firms attempt to grow their rates by 6% or possibly more in 2022.

Of course, this will test the willingness of clients to accept such steep rate increases. With macroeconomic inflation being as pervasive as ever, clients initially may look to chalk up cost savings among their vendors other than their outside counsel, especially in a time when legal advice is as valuable as ever.