Expanding horizons

Countries and jurisdictions throughout the world mandate that entity financial statements be prepared using International Financial Reporting Standards (IFRS), and that audits be conducted in accordance with International Standards on Auditing (ISAs). Although the use of IFRS and ISAs isn’t mandated in countries such as the US, in our increasingly global economy, many accounting firms must now be able to address the needs of clients with reach outside the primary country in which they operate. Those needs may translate into auditing international affiliates of local clients or, conversely, auditing local affiliates of entities based abroad. Since their affiliates may use a different set of accounting principles or be subject to different auditing standards, those scenarios may demand an expanded set of skills for audit firms.

International Financial Reporting Standards

IFRS is a single set of accounting and financial reporting standards developed by the International Accounting Standards Board (IASB). They are intended for global use by entities in all types of economies – from developing countries to emerging markets to well-established industrialized nations. The purpose of IFRS is to provide financial statement users with consistent and comparable information across borders. According to the IFRS Foundation, the standards are currently legally approved for use in over 100 countries, including the European Union countries and more than two-thirds of the nations comprising the Group of Twenty (also referred to as the G20). Further, 52% of Fortune Global 500 companies use IFRS.

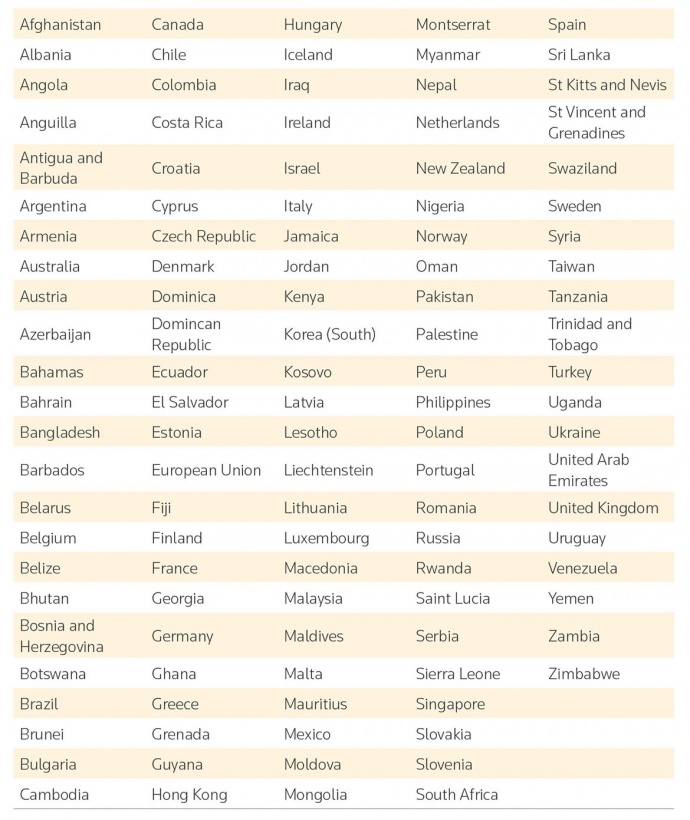

The table below shows the global jurisdictions that require IFRS for all or most publicly accountable entities, which include listed entities and financial institutions. Whether IFRS is used by non listed entities is generally determined by the respective national standard- setting bodies and, as a result, varies by jurisdiction.

Jurisdictions Requiring IFRS for All or Most Publicly Accountable Entities*

*Publicly accountable entities include listed entities and financial institutions.

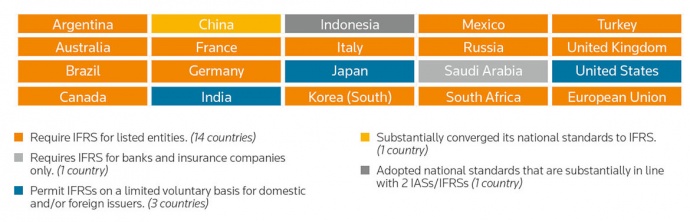

Consult the table below for the usage of IFRS in the G20, which consists of leaders of 19 countries and the European Union. The G20’s primary focus is global economic governance, and the nations represented in the G20 account for a significant portion of the world’s population, gross world product and world trade. All of the G20 have made a public commitment supporting a single set of high-quality global accounting standards and IFRS in particular.

G20 countries and IFRS

IFRS use in the United States

Currently, private entities in the US may choose to use IFRS, and the use of IFRS is becoming more popular because of the global footprint of some companies. In 2011, Ford Motor Company announced that it would be transitioning from US GAAP to IFRS in anticipation of the SEC allowing IFRS reporting in filings. In 2014, Ford began using IFRS for internal reporting purposes, even though for SEC filing purposes they are still required to use US GAAP. They have since stated that the change saves the company time and money by making information and processes more consistent across the 138 countries in which Ford operates.

Pros and cons of using IFRS

There are a number of reasons why a US company would choose to use IFRS as its accounting and financial reporting framework. But IFRS also has its detractors.

Summary of pros & cons of using IFRS in the US

| Pros | Cons |

|---|---|

| Provides a single global accounting language | Principles-based standards with a lack of industry-specific or transactional guidance may decrease the quality and consistency of reporting |

| Provides some level of financial reporting comparability across jurisdictional borders | An absence of interpretive application guidance may reduce comparability among jurisdictions |

| Regional regulatory bodies are contributing to consistency through international coordination | A lack of independent funding for the IASB |

| The US is currently well-represented in the IFRS standard-setting process with three seats on the 14-member IASB | The IFRS standard-setting process is potentially subject to influence by political forces, which could lead to conflicts and inconsistent practices between jurisdictions |

| Creates savings via standardized processes, systems and internal controls across jurisdictions |

System, process and contract changes plus training may be cost-prohibitive for some |

| Is attractive to international investors, customers, vendors, etc. | Learning curve for domestic investors and stakeholders may be steep and disruptive |

IFRS and US GAAP convergence

The IASB and the Financial Accounting Standards Board (FASB) began working toward convergence of international and US accounting standards in 2002, when the two boards jointly issued a Memorandum of Understanding (MOU) announcing their collaboration with the objective of creating a single set of high-quality global accounting standards. In 2006 and again in 2008, the boards updated the MOU, and since commencing the convergence project, the FASB and IASB have tackled a number of projects together with varying outcomes. The most notable success of the project came in May 2014 with the concurrent release of a converged revenue recognition standard. Other high-profile projects, such as lease accounting and financial instruments, have resulted in differing approaches being taken by the two boards.

Although the FASB and IASB have participated in convergence projects and collaborated in some areas, there are still many differences in the two sets of accounting standards. One of the fundamental areas of divergence between the two sets of accounting standards is the increased focus on fair value measurement of assets and liabilities in IFRS. Many have expressed concern that convergence between the FASB and IASB is essentially over, but officials with the IFRS Foundation and FASB have both expressed a continued commitment to working toward making standards more comparable.

IFRS and the SEC

Currently, only foreign private issuers may prepare financial statements using IFRS for SEC filings. Over the last five years, there has been a great deal of discussion about the extent to which publicly traded entities in the US may use IFRS. In a speech to the Financial Accounting Foundation in May 2014, Mary Jo White, SEC Chair, said, “… considering whether to further incorporate IFRS into the US financial reporting system has also been a priority for me. And, it continues to be.” In February 2016, however, James Schnurr, chief accountant of the SEC, stated in a speech at the SEC Speaks conference hosted by the Practising Law Institute that the SEC will be proposing a rule making it clear that “… for the foreseeable future, the US will not be allowing domestic issuers to file financial statements under IFRS.” The proposed rule is expected to permit US issuers to voluntarily provide IFRS information to supplement their GAAP financial statements.

International standards on auditing

ISAs are established by the International Auditing and Assurance Standards Board (IAASB). The IAASB is an independent standard-setting board overseen and supported by the International Federation of Accountants (IFAC), a global organization with 175 member entities and associates representing 130 nations and jurisdictions. IFAC member entities are nationally recognized professional accountancy organizations. The US, for example, is represented by the American Institute of Certified Public Accountants (AICPA).

In order to maintain quality, the IFAC has a compliance program in place to ensure that its member entities meet certain standards. Member entities are required to comply with the IFAC Statement of Membership Obligation, which is comprised of seven benchmarks for robust, credible and high- quality professional accountancy organizations.

ISAs are currently used in over 100 jurisdictions globally, and more than 80 of those jurisdictions also require the use of IFRS for all or most publicly accountable entities. Currently, private entities in the US may obtain audits in accordance with the ISAs if required, although the ISAs are not currently recognized by the AICPA. While international and US auditing standards are largely converged, there are some important differences. For example, one area of special consideration for auditors on an international engagement is group audit implications. ISA 600 doesn’t allow the auditor’s report on group financial statements to make reference to a component auditor unless required by law or regulation to do so, whereas US auditing standards allow such a reference.

Because of the increasing need to conduct audits under international standards, Thomson Reuters has partnered with accounting firms with clients outside the US to develop a new international audit practice aid product. These audit practice aids are for use in audits of non listed commercial entities that follow IFRS and are conducted in accordance with the ISAs. In addition, we currently are working with Thomson Reuters locations in multiple global markets to help firms address the opportunities presented by the convergence of international audit and accounting standards.

Learn more