As companies' risk profiles grow in complexity due to the demand for transparency around ESG issues, tax & accounting firms may see a big opportunity for more business

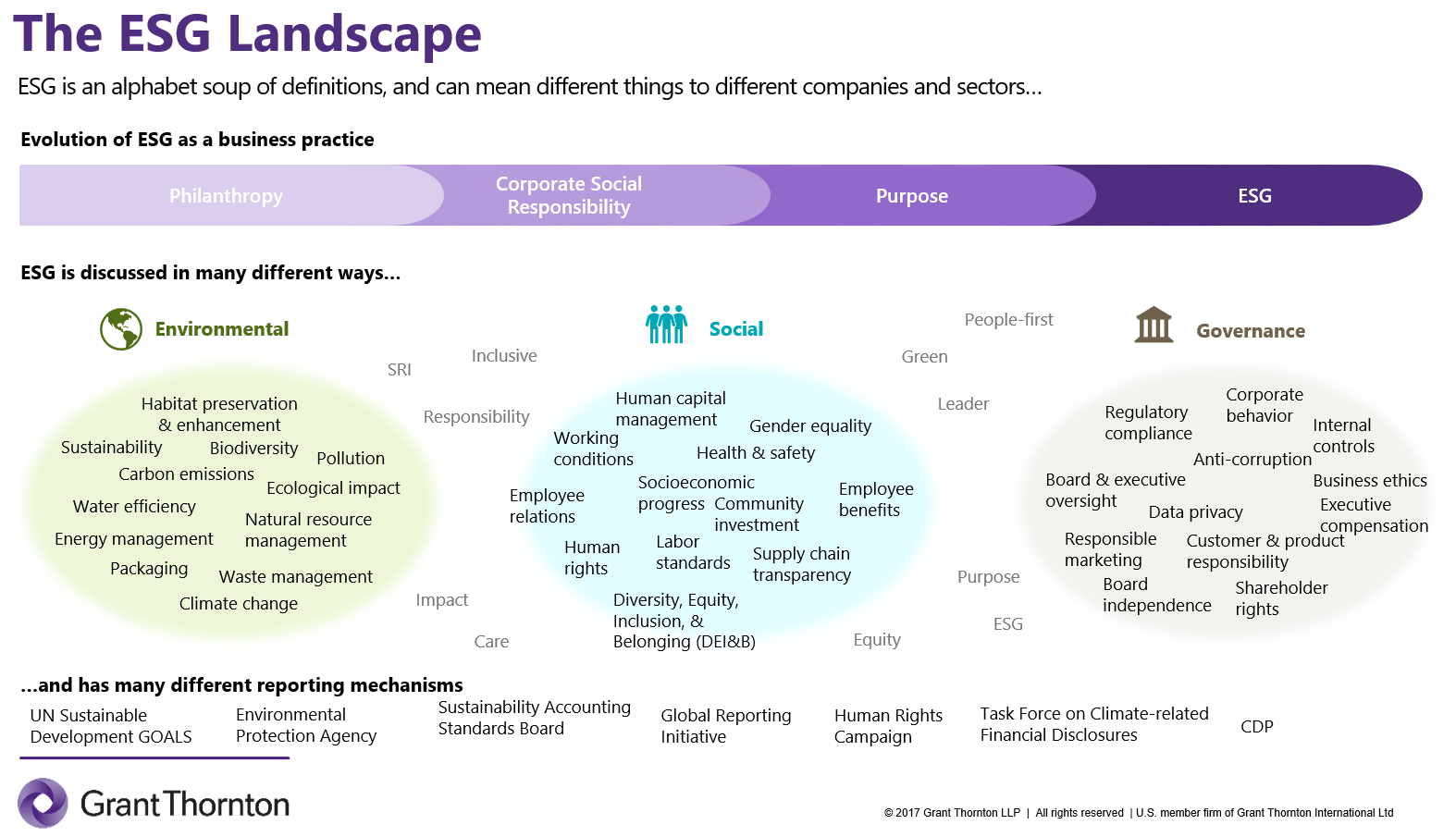

Demand for transparency in environmental, social, and governance (ESG) issues will expand in 2023, as we’ve discussed previously concerning the legal industry. Indeed, the vast range of potential topics, as illustrated below by Grant Thornton, that might come into play for a company’s risk profile is growing in complexity.

Issues on the ESG horizon

Adding to the complexity is the proposed rule by the Securities and Exchange Commission (SEC), The Enhancement and Standardization of Climate-Related Disclosures for Investors, which is likely to spur a ton of activity among public and private companies, according to April Little, Partner, Tax Risk & Advisory Services at Grant Thornton. “As we get closer to the SEC finalizing their rules, we’re going to see public companies have to start disclosing various aspects of their emissions described in three scopes,” Little explains. These scopes include:

-

-

- Scope 1 emissions — These are direct emissions from sources of operations owned or controlled by a company;

- Scope 2 emissions — These are indirect emissions from purchased utilities, such as electricity, gas, and other energy sources; and

- Scope 3 emissions — These are all other emissions associated with company activities, including those of its supply chain, which include many private small-to-medium sized enterprises (SMEs). [Note: As proposed, Scope 3 emissions disclosure is only required if material and is not required for smaller reporting companies.]

-

With the anticipated finalization of SEC rules — which is expected to be met with a lot of legal challenges — corporations need to establish appropriate processes, policies, and governance over the reporting is essential. Tax professionals, CPAs, and accountants “are in a great place to really jump into the fray on that data gathering exercise because we understand how the data fits into financial statements, where it comes from and how to make sure that it’s complete and accurate,” Little says.

When finalization of the SEC rules is completed, third-party ESG assurance is another avenue of growth for CPAs. “For companies looking to make progress on ESG to strengthen relationships with key stakeholders like customers or lenders, it’s important to consider both ESG strategy as well as ESG reporting and compliance,” says Marjorie Whittaker, Managing Director of ESG and Sustainability at Grant Thornton. “Both elements are critical to the success of an ESG program and provide meaningful opportunities for CPAs to add value.”

Whittaker explains that many of the elements of ESG transparency are similar to those found in traditional financial reporting and assurance. “For example, establishing reliable baseline performance data, making sure that reported information is fairly presented, balanced, and meets the requirements of the applicable reporting standard — all of those skillsets are resident within CPA firms,” she adds.

Business opportunities for accounting firms

In particular, reporting requirements on Scope 3 emissions in the near term will cause the most headaches for multinational corporations and their suppliers because the rules will require large companies to estimate greenhouse gas emissions from their supply chain partners, whether they are a public or private company. In addition, many of these vendors are SMEs, located across the globe. Yet, the more proactive SMEs see what is coming even in Asia, and they are preparing now to provide the necessary of information in anticipation of the finalization of the SEC rules.

This and the aforementioned growth in complexity is a huge market opportunity for tax & accounting and consulting firms. Early movers, such as public accounting firm Sensiba San Filippo (SSF), are seeing tremendous growth in their already robust multi-disciplinary ESG practices.

SSF’s sustainability practice advises SMEs on their sustainability strategy as part of the Sensiba Center for Sustainability, which launched in 2020, under the leadership of Jennifer Cantero. Before 2020, the firm’s practice was centered on consulting companies through the B Corporate certification but expanded when an audit partner approached Cantero about getting the Fundamentals of Sustainability Accounting Credential, which equips professionals with the “knowledge and skills to understand the link between financially material sustainability information and a company’s ability to drive enterprise value.” The credential is awarded by the Sustainability Accounting Standards Board (SASB), which is one of the popular ESG frameworks that sets standards for disclosing financial material sustainability by businesses.

The firm’s growth path of its sustainability practice came from already existing clients that operated in manufacturing as part of the food and beverage industry. The firm’s practice includes an assessment of their current operations based on a comparison against a standard, usually using one of the well-known frameworks, such as SASB. Within this service, there is a whole range of targeted benchmarking evaluations, which include product life cycle assessments, pay equity analysis, and information security exercises.

Another key part of their services is examining and calculating a SME’s carbon footprint with recommended options on how to reduce it. SSF analyzes collects, compiles, and analyzes raw data from the client’s records, which is essential for a rigorous review. “That’s the superpower of the accounting world is that we can go in and do a pretty good job of analyzing data to determine its quality,” Cantero notes. “We’ve been doing it for a millennia on the financial side, and now we’re just applying those principles to all the non-financial data.”

Another advantage for accounting firms in building their own sustainability practice is that they are then able to wrap in already-existing services that fall under ESG. For example, SSF already provides services related to data privacy regulation audits, such as the European Union’s General Data Protection Regulation. Firms can then conduct those audits based on recognized methodologies, such as the American Institute of Certified Public Accountants’ Service Organization Control (SoC) 1, 2, and 3, which reports on various organizational controls related to security, availability, processing integrity, confidentiality, or privacy.

Whether the proposed rules on climate disclosure are finalized next year or later really does not matter, because institutional investors’ demands around transparency and risk management will remain — as will corporations’ obligations to meet these demands. In this environment, the business opportunities for tax & accounting firms around sustainability and ESG transparency is growing and will continue to do so.