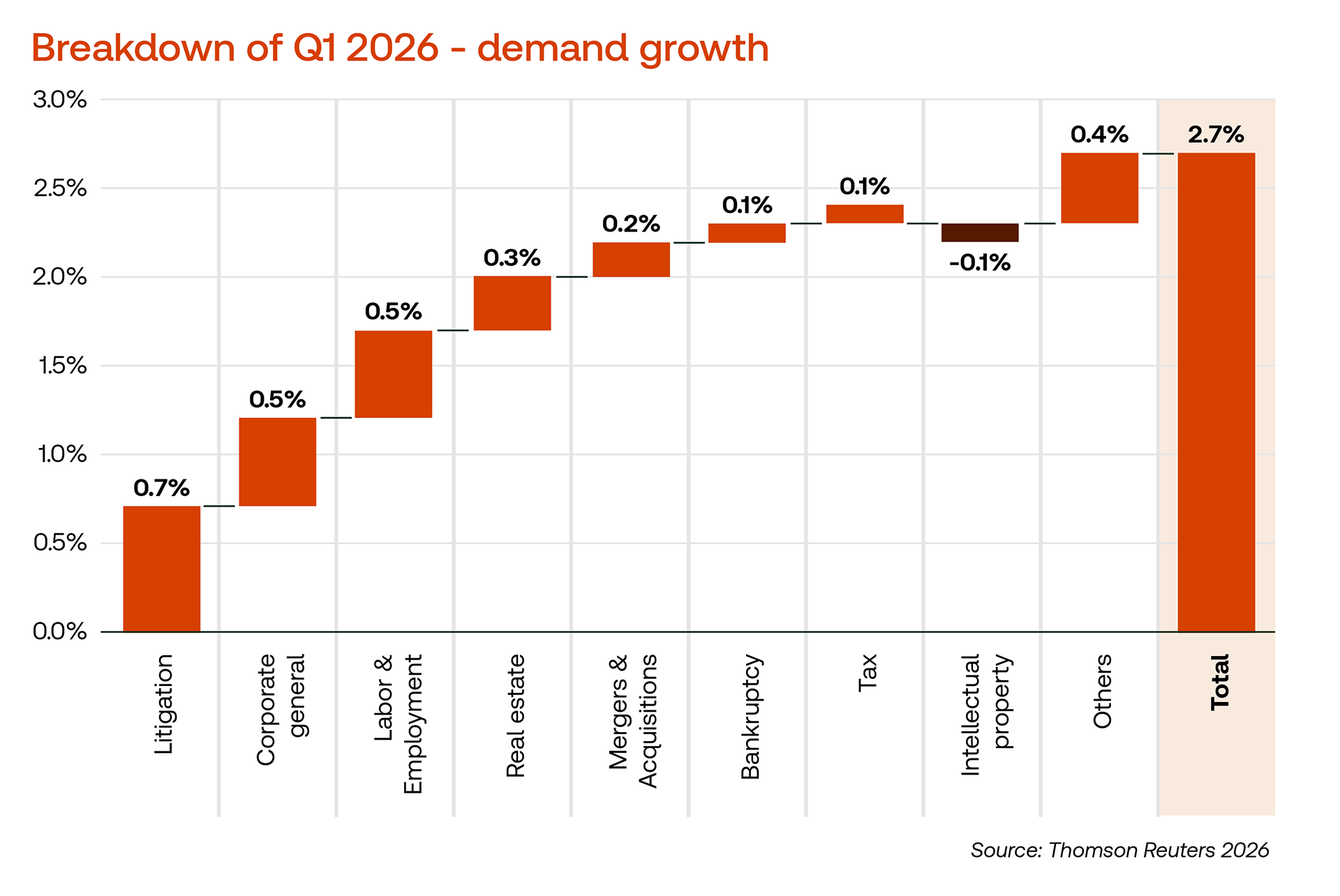

Legal demand in Q1 2026 grew 2.7% — but the more telling story lies in which practices are doing the growing, and which firms are learning to work with what the market gives them

Key insights:

-

-

-

Branches too, not just trunks, drive growth — Across firm segments and US regions, litigation and corporate work still anchor demand, but they are not always the main sources of new hours.

-

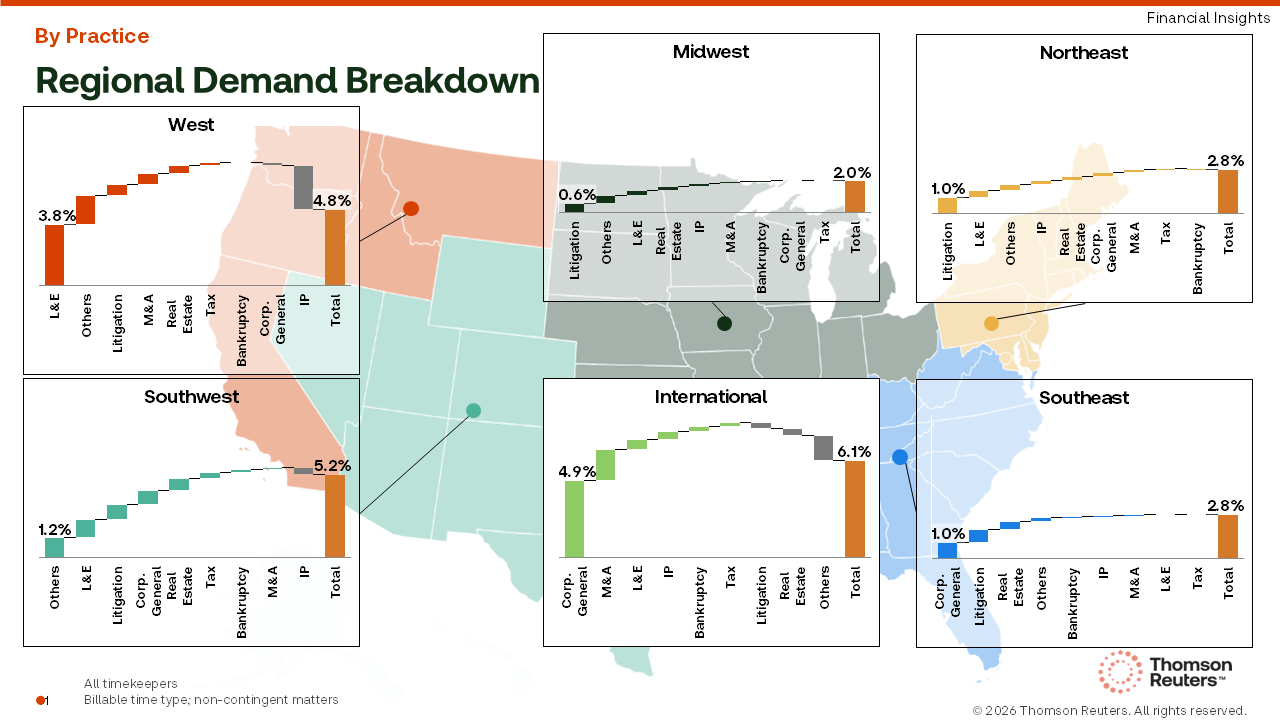

Soil conditions vary sharply by region — The Southwest US and international markets led all regions with 5.2% and 6.1% demand growth, respectively, driven by niche and transactional practices, while the Midwest and Eastern regions grew more modestly.

-

Midsize firms are growing through specialization — Struggling to compete on volume with the Am Law Second Hundred or on rates with the Am Law 100, Midsize law firms posted 2.6% demand growth powered primarily driven by smaller, specialized practices.

-

-

The first quarter of 2026 arrived with law firms still standing on solid ground, although the footing is beginning to feel a little less certain beneath the surface. As the Thomson Reuters Institute’s recent Q1 2026 Law Firm Financial Index (LFFI) reported, the score landed at 55 — exactly the historical average since 2006, which is a modest place to be when you consider that Am Law 100 firms pushed worked rate growth to nearly 10%, and overall demand came in at 2.7%, roughly triple the long-run average. Those are not average inputs. Something is absorbing the gains.

The story beneath the headlines is one of diverging strategies, uneven soils, and the quiet question of whether a tree can keep growing by strengthening only its trunk — or whether it needs to extend its branches.

Reading the soil: Regional demand across the US

Just as trees grow differently depending on the nutrients available in their soil, law firm demand across different regions of the United States reflects the distinct conditions shaping each local market.

The western half of the country set the pace. The Southwest posted the strongest domestic growth at 5.2%, driven not by the dominant practices of litigation or corporate work, but by a constellation of smaller practices (labeled “others”) that collectively delivered the largest single contribution to new hours — 12 of the 52 additional hours worked per 1,000 compared to Q1 2025. Labor & employment and litigation followed, but the headline is that niche practices — treated by many firms as secondary concern — carried the region.

The West grew at 4.8%, with labor & employment as its leading driver, although intellectual property imposed a meaningful drag: Law firms in the West are currently working 27 fewer hours per 1,000 on IP matters than they were a year ago, a loss that’s partially masking an otherwise healthy broad-based expansion.

International operations led all regions at 6.1% growth, but with an important asterisk. This region, which captures demand generated by US-headquartered firms operating abroad, was recovering from a period of contraction. The surge was powered almost entirely by corporate general and M&A, making it the most transactionally concentrated region in Q1. The flip side —real estate, litigation, and “others” practices all contracted, meaning growth here is reliant on a narrower set of practices than it may appear.

The Eastern and Central regions told a more measured but arguably more durable story. The Midwest grew just 2.0%, but with a notable quality as no practice area contracted. Every discipline contributed at least marginally to new hours worked, with litigation doing the heaviest lifting. The Northeast and Southeast each came in at 2.8%. In the Northeast, growth was similarly broad, with no practice in retreat; while the Southeast offered a small twist as corporate general led for the first time among the regions examined. Litigation followed close behind, and together the two practice areas accounted for 18 of 28 new hours worked. Those two practices — the trunk of any large firm’s business — pulled more relative weight in the Southeast than anywhere else in the country.

The story beneath the headlines is one of diverging strategies, uneven soils, and the quiet question of whether a tree can keep growing by strengthening only its trunk — or whether it needs to extend its branches.

What stands out across this regional picture is that for most of the US, the new growth is not coming just from the traditional core. Corporate general and litigation remain the largest absolute contributors to demand — the sturdy trunk — but in the West and Southwest, it is the branches that are responsible for incremental gains: labor & employment and a diverse mix of smaller practices. In US regions in which the trunk remains the engine — such as the Midwest, Southeast, and Northeast — growth is still real but narrower. The more resilient growth stories tend to be the ones in which no single branch bears all the weight.

The tree type matters too: Demand by firm segment

Regional soil explains some of the variation in Q1 demand, but not all of it. The type of firm shapes how growth is structured just as much as geography. And in Q1 2026, the three segments grew in ways that were as different from one another as oaks from aspens.

The Am Law 100 posted demand growth of 1.2%, the lowest of the three segments, but this is consistent with a strategy built primarily on rate power rather than volume. Of the 12 additional hours per 1,000 worked compared to Q1 2025, transactional practices contributed 8 hours, and counter-cyclical practices added 5 among Am Law 100 firms. The one drag came from intellectual property, which contracted by 1 hour. For the largest firms, demand is supplementary to rate growth — the trunk is wide, and thus, the tree does not need to grow tall to be profitable.

The Am Law Second Hundred grew 4.0%, the strongest demand performance of the three segments, and the composition of that growth is striking. Of 40 new hours per 1,000 worked, counter-cyclical practices — led by litigation at 15 hours and labor & employment at 7 — contributed 22 hours. Transactional practices added 9. No practice contracted. This is a segment with unusually full canopy coverage: growth is broad, and every branch is pulling upward. The Second Hundred’s continued “moat of demand” in this area remains one of the more durable stories in the legal market.

The most instructive case, however, is the Midsize segment. Midsize firms grew demand 2.6% in Q1, roughly in line with the industry average. However, the source of that growth tells a different story than the numbers suggest. Of 26 new hours per 1,000 worked, the largest contributor was “others” — a category of smaller, specialized practices — at 8 hours. Corporate general added 6, real estate and litigation 4 each. No practice contracted.

What that picture reveals is a segment finding its footing not by competing on volume — where the Second Hundred has structural advantages — or on rate increases, where the Am Law 100 holds the leverage. Midsize firms appear to be carving out a third path: specialization. The tree is not the tallest, and the trunk is not the thickest, but it is filling out its canopy with branches that larger competitors have left largely unattended.

Growth is in the canopy

As the LFFI showed, Q1 2026 produced broad-based demand growth, but the data is clear on one thing: A healthy trunk is not enough. In some regions, the incremental gains came from practices that many firms still treat as secondary — labor & employment and a rotating mix of smaller specialties. In most segments, the firms building fuller canopies are outperforming those relying on a narrower set of core practices.

Midsize firms are perhaps the most visible example of a segment adapting to its conditions. Unable to out-volume the Second Hundred or out-price the Am Law 100, they are finding ways to grow through diversification. Whether that strategy can close the widening performance gap against their larger competitors remains to be seen.

However, the Q1 data suggests that for firms at every level, the next phase of growth is likely to come not from further strengthening what is already strong, but from investing in branches that have yet to reach their full height.

You can download a full copy of the Thomson Reuters Institute’s Q1 2026 Law Firm Financial Index here