As legal demand continued to slow in the most recent quarter, law firms may have found a new pathway toward profitability in pursuing stronger rate growth and higher realization

In the second quarter, the legal industry saw overall demand for legal services contract as nearly every practice area experienced a softening of demand. With the sharp reversal in demand performance from 2021, increasing expense growth dragged the Thomson Reuters’ Law Firm Financial Index (LFFI) score to its lowest point yet recorded in this past quarter.

While the challenges facing the legal industry are numerous, many law firms maintained robust worked rate growth and saw realization rate improvements, giving them key pathways to continued profitability. If demand continues to slide further, the importance of these pathways will only continue to rise.

Prices & inflation, a long-term relationship

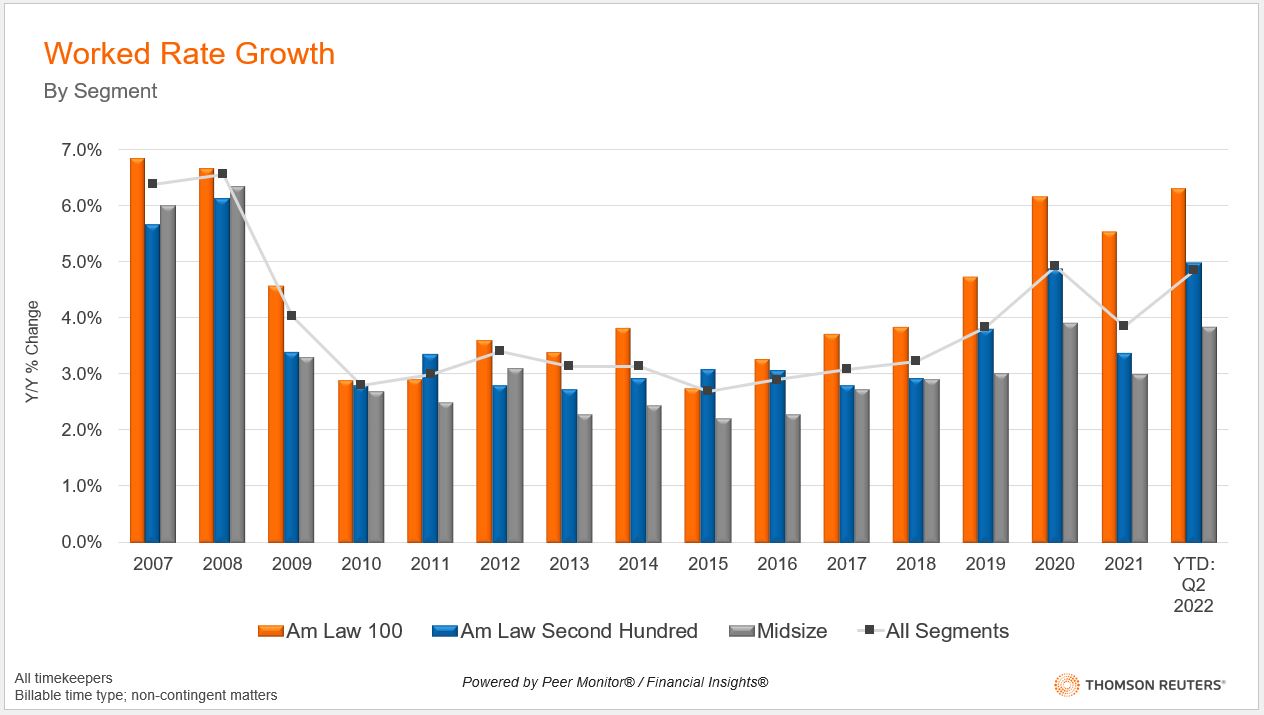

To contextualize the improvements in these areas seen in Q2, we can look at the chart below to see how worked rates have performed historically. Following the Global Financial Crisis (GFC), all segments experienced a steep drop in worked rate growth that bottomed out near or below 3% growth for much of the 2010s.

In 2020, however, the pandemic artificially inflated rates as higher-priced partners took on more work at the request of clients, which in turn triggered a whiplash effect for year-over-year calculations that artificially deflated rate growth in 2021 when those shifts reversed. This year, and particularly this quarter, law firms have distributed work more comparably to the year prior, making 2022’s rate growth thus far a much more accurate representation of current conditions. Consequently, the second quarter’s worked rate growth appears to be particularly strong.

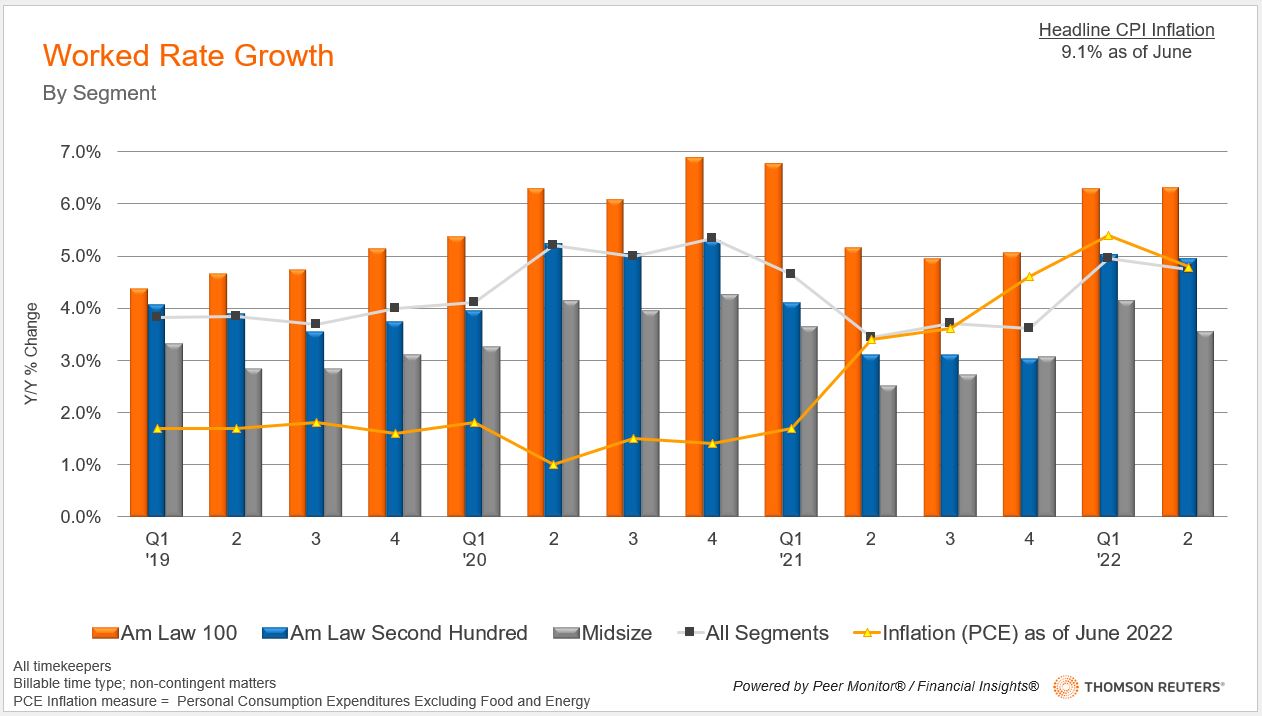

This strength is heightened further when we look at worked rate growth compared to inflation. To compare these two figures, we used an inflation measurement called core PCE (personal consumption expenditures), which removes food and energy inflation from the calculation and provides a more robust sampling than the more commonly used Consumer Price Index (CPI). We prefer using core measurements because it describes areas of inflation more likely to significantly affect overall legal industry expenses, because these areas (food and energy) of inflation do not affect overall legal industry expenses to quite the same extent as the average consumer, and thus more accurately describes how law firms are experiencing inflationary pressures.

With this understood, we can see that Q2 inflation again outpaced worked rate growth for many firms, albeit at a much smaller rate compared to recent quarters. This represents the third consecutive quarter in which worked rate growth grew at a slower pace than inflation.

However, we saw second quarter growth rates improve 1.3 percentage points on a year-over-year basis, climbing to a very healthy 4.7% in Q2 2022, from 3.4% growth in Q2 2021. Even though second quarter worked rates grew slightly slower than the values seen in Q1, inflation also slowed, allowing worked rates to close the gap from a purchasing power perspective. Further, the drop from Q1 can be attributed to slowing growth from the Midsize law firm segment as both the Am Law 100 and Am Law Second Hundred segments maintained nearly identical growth in rates from quarter to quarter.

It is important to recognize, however, that while this past quarter has seen inflation decrease, firms are uncertain how long this will last. Worked rates have historically outpaced inflation, but recent tumultuous times have flipped the table on the legal industry as we saw in Q4 of last year and then in Q1 of this year. These unusual circumstances have forced firms to consider mid-year rate increases, something that was unheard of since the GFC. If demand slows while inflation grows, the motives for a more aggressive worked rate strategy are evident.

Realization — the Missing Link

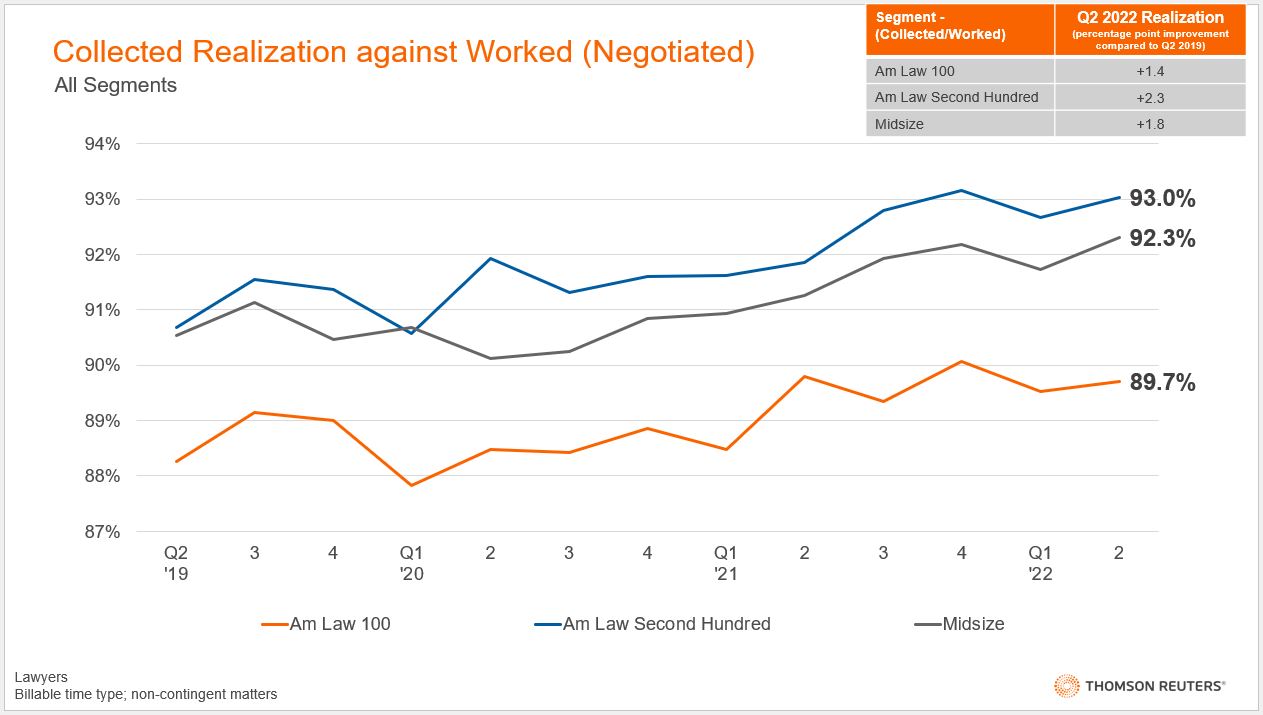

The second quarter also saw collected realization increase relative to the first quarter (a typical seasonal trend) with the industry overall seeing a 0.4 percentage-point increase. This was driven by the Midsize segment, which saw the most impressive improvement, coming in with a 0.6 percentage-point increase from the previous quarter. More importantly, we can also see that compared to 2021’s second quarter, both the Am Law Second Hundred and the Midsize segment grew collected realization by around 1 percentage point — a fantastic development.

The growth in realization seen in Q2 is even more striking when compared to Q2 2019, the last pre-pandemic second quarter. Looking at the table in the upper right corner of the chart above, we can see that all segments increased collected realization by a minimum of 1.4 percentage points. The Am Law Second Hundred saw the largest growth with growth at 2.3 percentage points, while the Am Law 100 saw the smallest growth.

It’s also worth pointing out that Am Law 100 firms already had the lowest realization rates going into the pandemic, and seemingly continue to struggle to improve to the same degree as their smaller counterparts. This may be due to the Am Law 100 experiencing the largest drop in overall demand in Q2, or posting the largest annual market-leading worked rate growth seen since 2016, which is now north of 6% in 2022.

In 2021, when demand pushed capacity to its limits, larger law firms may have had to prioritize clients who were less likely to challenge invoices. As transactional work slowed and led to the Am Law 100’s Q2 demand contraction, those tailwinds became weaker, and realization did not increase to the same degree. Additionally, it’s important to note that there were strong improvements in realization from the Am Law Second Hundred and Midsize firms. In essence, the pandemic forced lawyers to utilize increased digitalization and efficiency with their billing practices, advantages that have been retained and are enabling firms to capture the most from their lawyer’s time.

Overall, this past quarter saw worked rates and realization grow despite inflation remaining high. Firms saw revenue generation revert from enjoying increasing demand to relying on rate increases in the second quarter — returning to how firms have historically used worked rate growth to increase profitability. The pandemic created a highly anomalous setting that forced firms to capture as much demand as possible, making it a primary driver of 2021’s success. Now, as demand growth slows, many law firms are realizing that they may have to return to their tried-and-true recipe for profitability.