Will the trend of worked rate increases become a casualty of the legal industry's return to something resembling normal?

In the Q1 2021 Peer Monitor Index report, we had promising developments (like lawyer headcount that was on average only 0.1% lower than pre-pandemic levels of Q1 2020), and the current environment for law firms looks somewhat rosy just a year or so removed from where optimism in general was at its lowest level in some time.

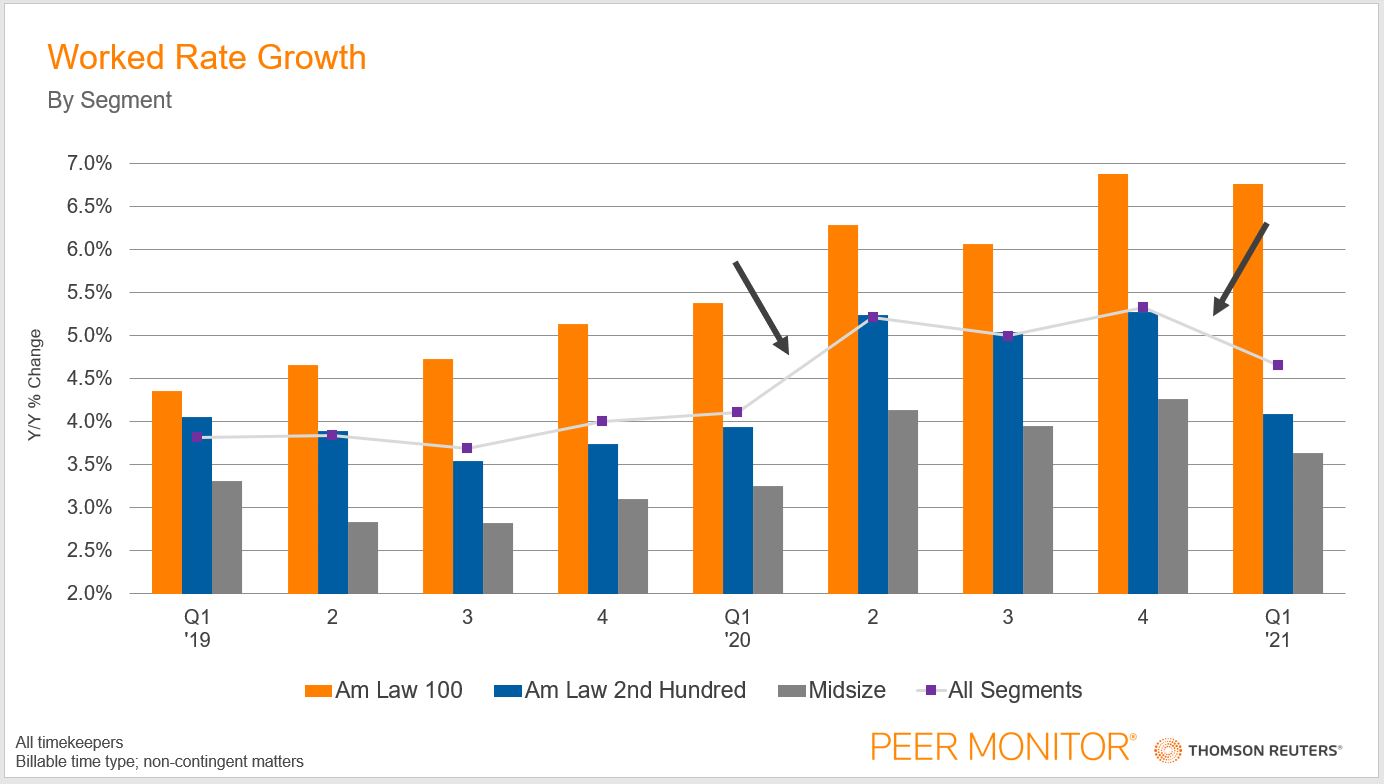

The only slightly negative key factor that can be perceived in this most recent quarter’s law firm performance is relative tick-down in the pace of worked rate growth. That said, this latest quarter’s rate of 4.7% growth is still a historically strong quarterly figure.

Indeed, the average rate growth in pre-pandemic Q1 2020 reached 4.1%, which was already the most aggressive pace seen by law firms since the financial crisis. In Q2 2020, during the doldrums of lockdowns, that figure rocketed up to 5.2% and continued to maintain that 5.0% threshold till year end. This is not a new development and has been discussed at length. In short, in the early months of the pandemic, partner work surged due to client demand for senior leadership and advice. As the work from home environment drudged into the fall and winter (Q3 & Q4 2020), partner work proportionally stayed elevated; however, allied professionals or non-lawyer full-time equivalents (as Peer Monitor database defines them), were more affected by staff reductions. As a result, there was fewer lower-priced hours and more higher-priced hours being recorded and measured off a normal year.

Now in 2021, this pandemic-altered hourly timekeeper distribution of 2020 is now our baseline against which we measure. While this brought increased rate performance during a much needed 2020 to helped offset demand shortfalls, any and all movement back toward a normal distribution of hours — such as in 2019 — among timekeepers should put some meaningful pressure on rate growth calculations.

Which brings us back to Q1 2021, you can see in the graphic above the notable easing in the pace for rate growth for all segments in Q1. Peeling back further however, you see Am Law Second Hundred and Midsize law firms are the main drivers for the lower rate performance with Am Law 100 firms maintaining their pace in Q1 with 6.8% average increases. This divergent retracement in rate performance was slightly perplexing as each segment saw about a 1% boost in rate growth during Q2 2020 as compared to Q1 2020, but the beauty of math is that often the source of the boon also provides the answer to the swoon.

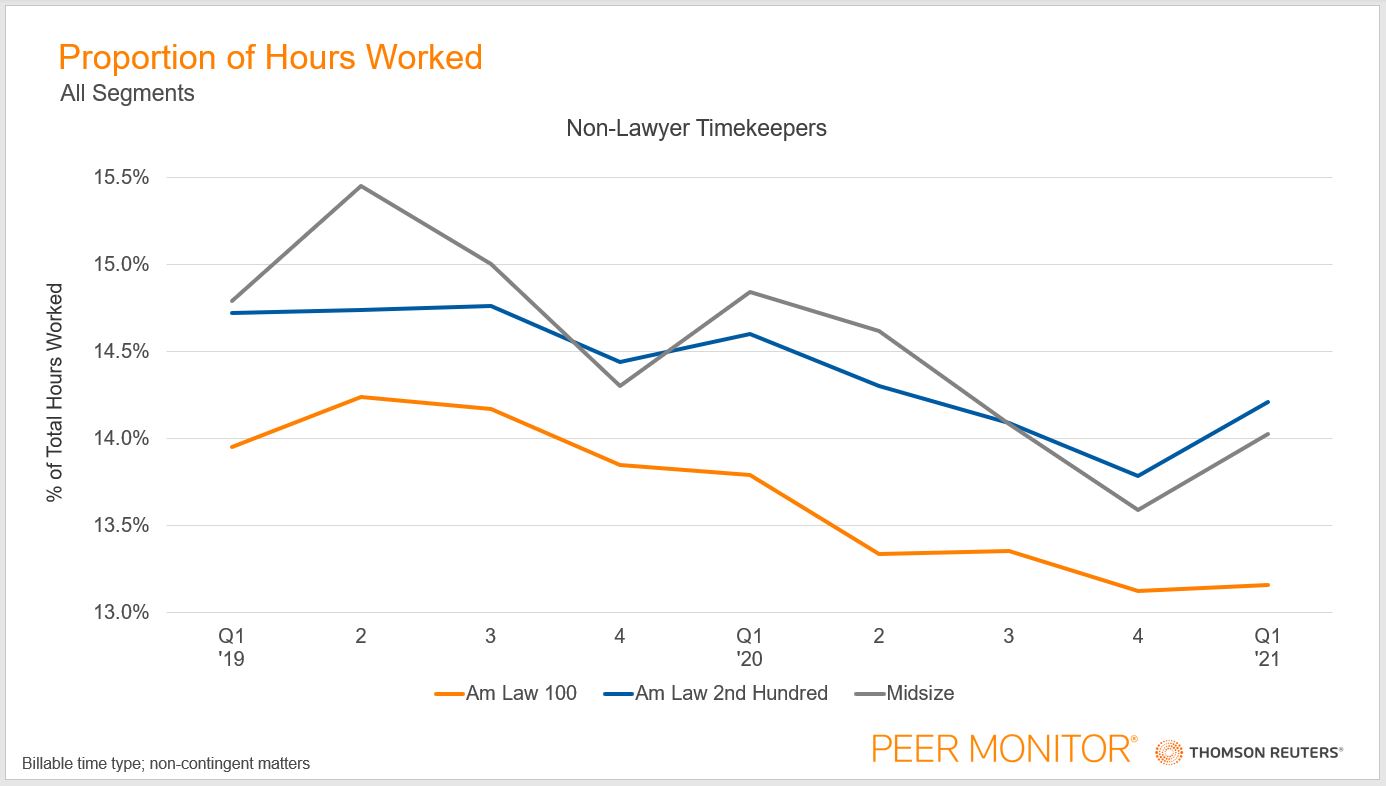

In the graphic above, we have our proportion of hours worked by allied professionals and non-lawyer timekeepers by each market segment. From the Q1 2020 until the end of the year, each segment progressively reduced the amount of hours worked firm-wide each quarter for these titles. The difference from Q1 to Q4 in 2020 was a 0.7% decline for Am Law 100 firms, a 0.8% decline for Am Law Second Hundred, and a 1.2% reduction for Midsize firms. Seemingly small figures, but extremely impactful over millions of hours worked and their associated fees. Directing focus now to the notable jump from Q4 2020 to Q1 2021 for Am Law Second Hundred and Midsize firms of a 0.4% proportional increase in hours worked by allied professionals, when juxtaposed to the Am Law 100 firms’ 0.03% increase suggests that a shift back toward a pre-pandemic distribution of hours has been slower moving for these larger organizations. None the less, this information helps us understand how the Am Law 100 can maintain its almost 7% rate growth of 2020 thus far into 2021. (As we said, whether this trend is going to last or not is something we’re keeping a close eye on as we move through 2021.)

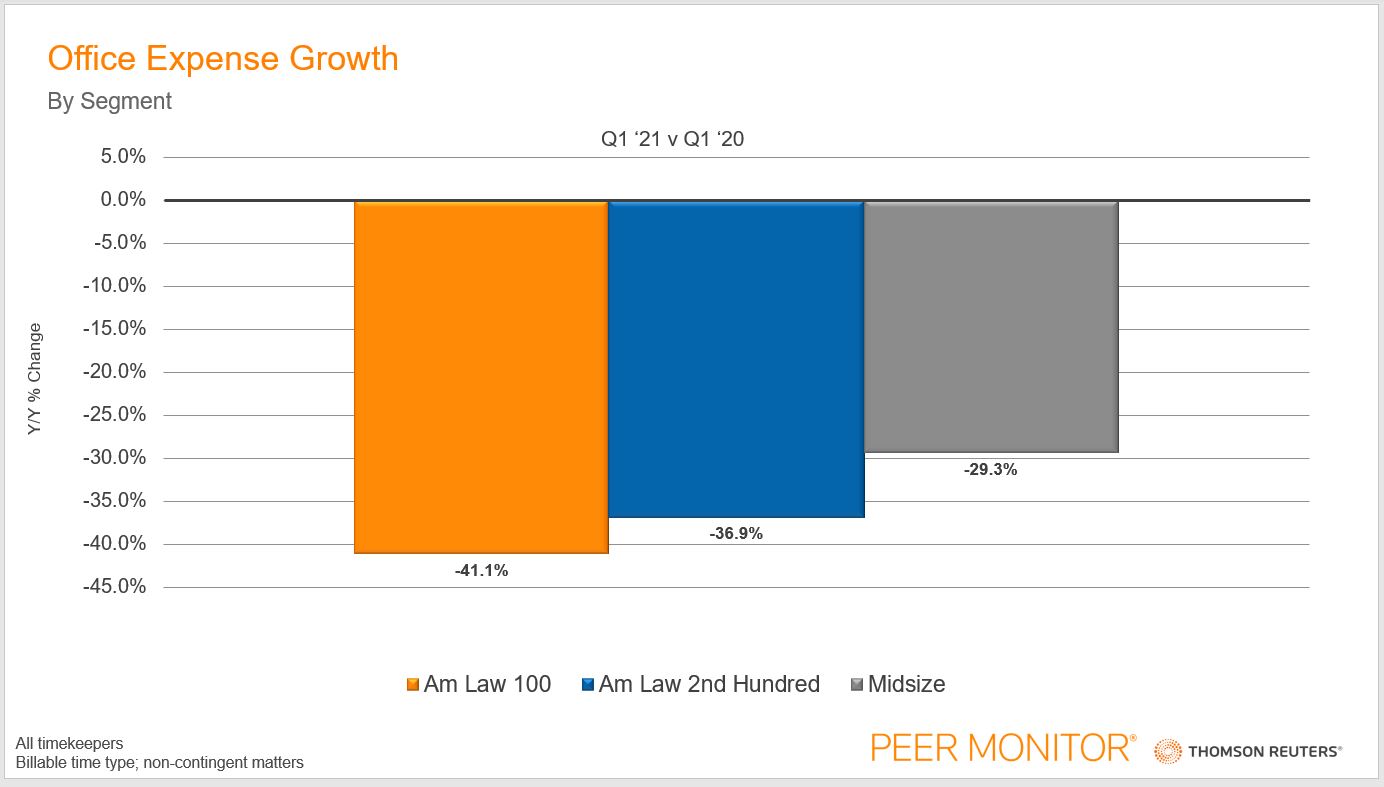

Lastly, I want to make an interesting correlation, the graphic above shows how office expenses changed between Q1 2020 and Q1 2021. Office expenses refer to office supplies like paper, furniture, meals, and more — but not rent or maintenance, which fall under occupancy. This expense line item can be seen as a proxy of sorts for the progress law firms are making in returning staff to the office. In this comparison, once again it looks as if the Am Law 100 firms have lagged behind the other segments in pursuing a return to “normal”.

For better or for worse, we have seen the pandemic force the professional services industry into a work-from-home environment. As law firms began to adapt and adjust to this new environment, non-lawyer timekeepers were not as necessary as they once were to maintain business continuity — mostly because lawyers themselves had the technological tools at their disposal and frankly, the time to bill those hours. This increased worked rates per hour for their clients, albeit somewhat unintentionally.

Remote working is not and will not be everlasting for everyone and every firm, however. On average, firms that are seeing less contraction to their office expenses compared to last year and have also returned a greater proportion of their work to non-lawyer fee earners, clearly look to me as if they are among the first-movers in returning to the office. In fact, Am Law 100 firms certainly look like there are going to be late-followers in the return-to-the-office race, if they decide to join the race at all.

These megafirms may not want to return to how business was done previously because of the double-digit profit growth of 2020, but they also could represent part of the new way in which law firms staff and manage their digital and office footprint. Which begs the question: Will the late-followers in returning to the office eventually become the new leaders in a way that other law firms try to mimic?