Diving deeper into the recent Q1 LFFI report shows that the Index's improvement was driven primarily by the rise in the rates that law firms were able to charge their clients

The first quarter of 2023 saw a remarkable improvement in the financial performance of law firms, as evidenced by Thomson Reuters’ Law Firm Financial Index (LFFI) score, which surged by 14 points to reach 44 at the start of the year. While this score follows the all-time low score seen at the end of last year and still sits low historically, this relative growth was driven by a multitude of factors that contributed to the overall enhancement of large law firms’ business fortunes. Notably, historic rate increases were among the key drivers of this improvement.

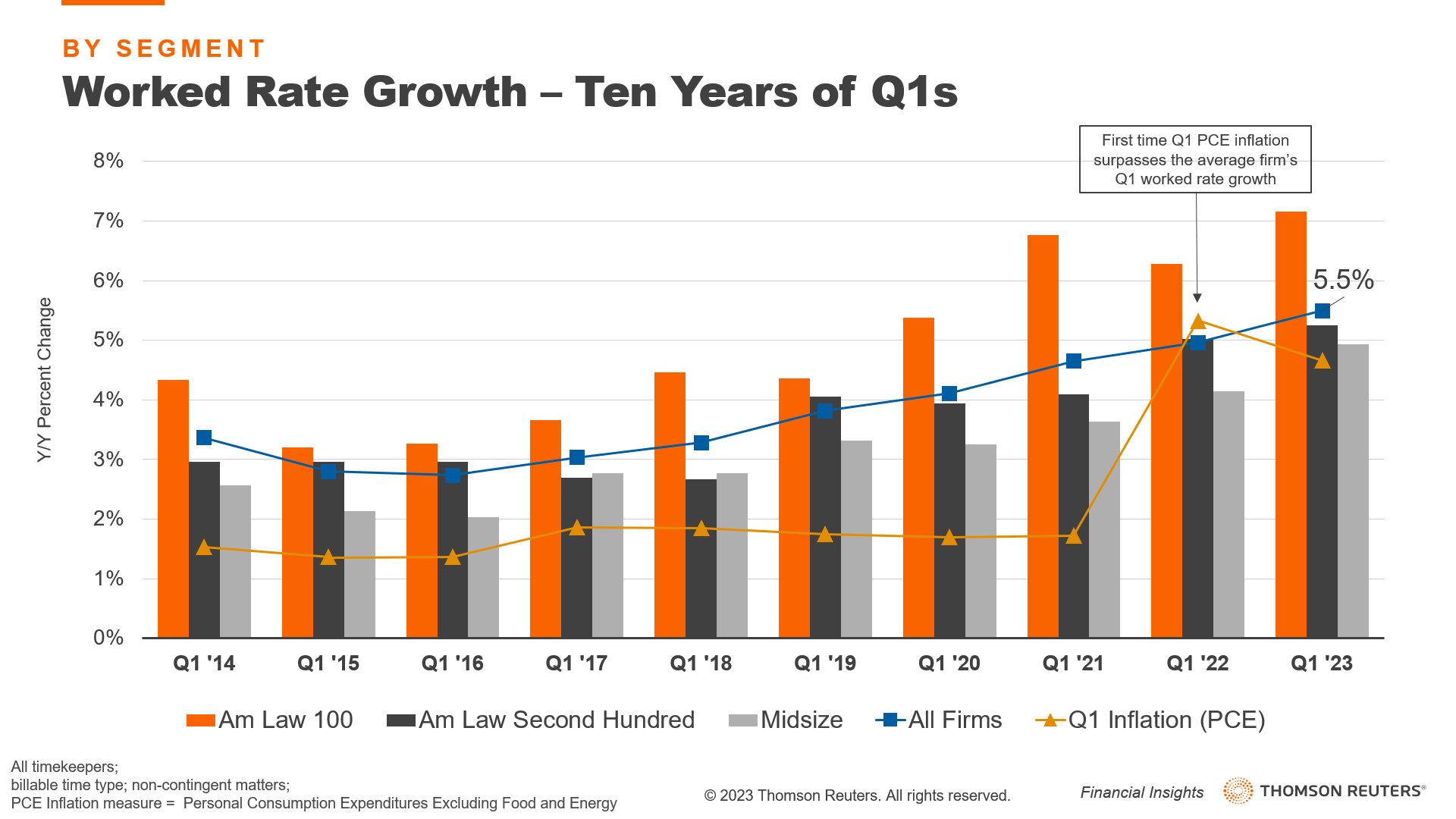

Following the aftermath of a second year of persistent inflation, many experts had anticipated a substantial surge in rate growth, with aggressive projections ranging between 7% and 8% for the first quarter. Although the actual results fell slightly short of these optimistic forecasts, the 5.5% rate growth achieved by the average law firm still stands out as the swiftest increase observed during a first quarter period since the end of the Great Financial Crisis (GFC).

These positive outcomes were observed throughout the market, with all segments exhibiting higher growth rates than their previously most significant post-GFC increases. Specifically, Midsize law firms saw rate growth of 4.9%, while Am Law Second Hundred firms saw their rates rise by 5.2%. Notably, Am Law 100 firms led the way in terms of rising rates, achieving a remarkable growth rate of 7.2%, surpassing the segment’s previous all-time record in the history of the Thomson Reuters Financial Insights program.

Navigating inflation & expense pressures

Last year marked the first time when the Q1 Core Personal Consumption Expenditures (PCE) inflation rate surpassed the average firm’s Q1 worked rate growth. This trend continued throughout the year, with rate growth consistently falling below core PCE.

In the current quarter, firms have returned to the status quo, in which worked rate growth once again outpaces inflation. While this development is encouraging, the difference between inflation and firms’ rates remains relatively small compared to historical norms, which is particularly pertinent for less assertive Midsize firms.

Although expenses are growing more slowly both in aggregate and on a per-lawyer basis, the aftermath of rapid compensation hikes — combined with inflation-driven overhead growth and return-to-office strategies — is exerting tremendous pressure on firm profitability. In light of these factors, substantial rate adjustments were not only expected but necessary to ensure that firms remain competitive and financially sustainable in the long run.

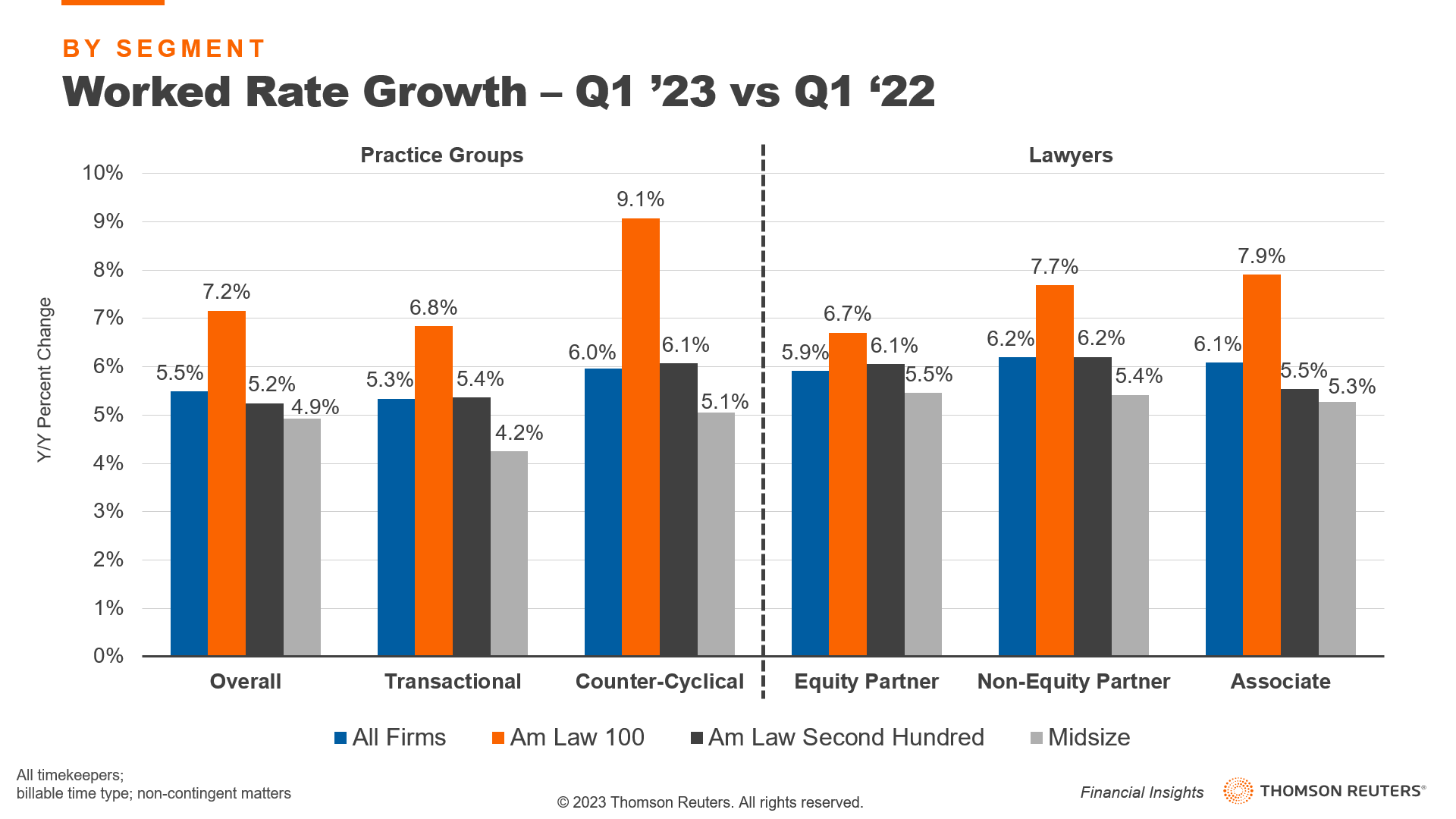

On a practice area basis, the most significant upward adjustments occurred in counter-cyclical practices — such as litigation, bankruptcy, and labor & employment practices — which also experienced the greatest surge in demand. Conversely, transactional practices suffered contractions in demand across the board, and their growth rates were comparatively lower suggesting some degree of price elasticity. Thus, the remarkable growth in counter-cyclical practice rates was able to offset the weaker rate growth observed in other areas and propelled this quarter’s overall improvements. Indeed, across all segments, counter-cyclical work commanded higher price increases than transactional work, and this behavior was most pronounced in the top end of the market, where Am Law 100 firms recorded counter-cyclical rate growth that was more than two percentage points higher than their transactional rates. Of course, this phenomenon mostly resulted from these firms experiencing the greatest declines in demand for transactional work.

Looking at rate growth from lawyer-title perspective, a familiar stair-step approach was observed among the segments, with Am Law 100 attorneys recording the highest rate growth, followed by Second Hundred and Midsize attorneys. However, a divergence in results emerged from the relative rate increases between partners and associates within each segment. The rates for associates at Am Law 100 firms were raised much more aggressively than their equity and non-equity partners. By contrast, associates at Am Law Second Hundred and Midsize firms did the opposite, with partners commanding higher rate increases than their associate counterparts.

Law firms’ Third Law of Motion

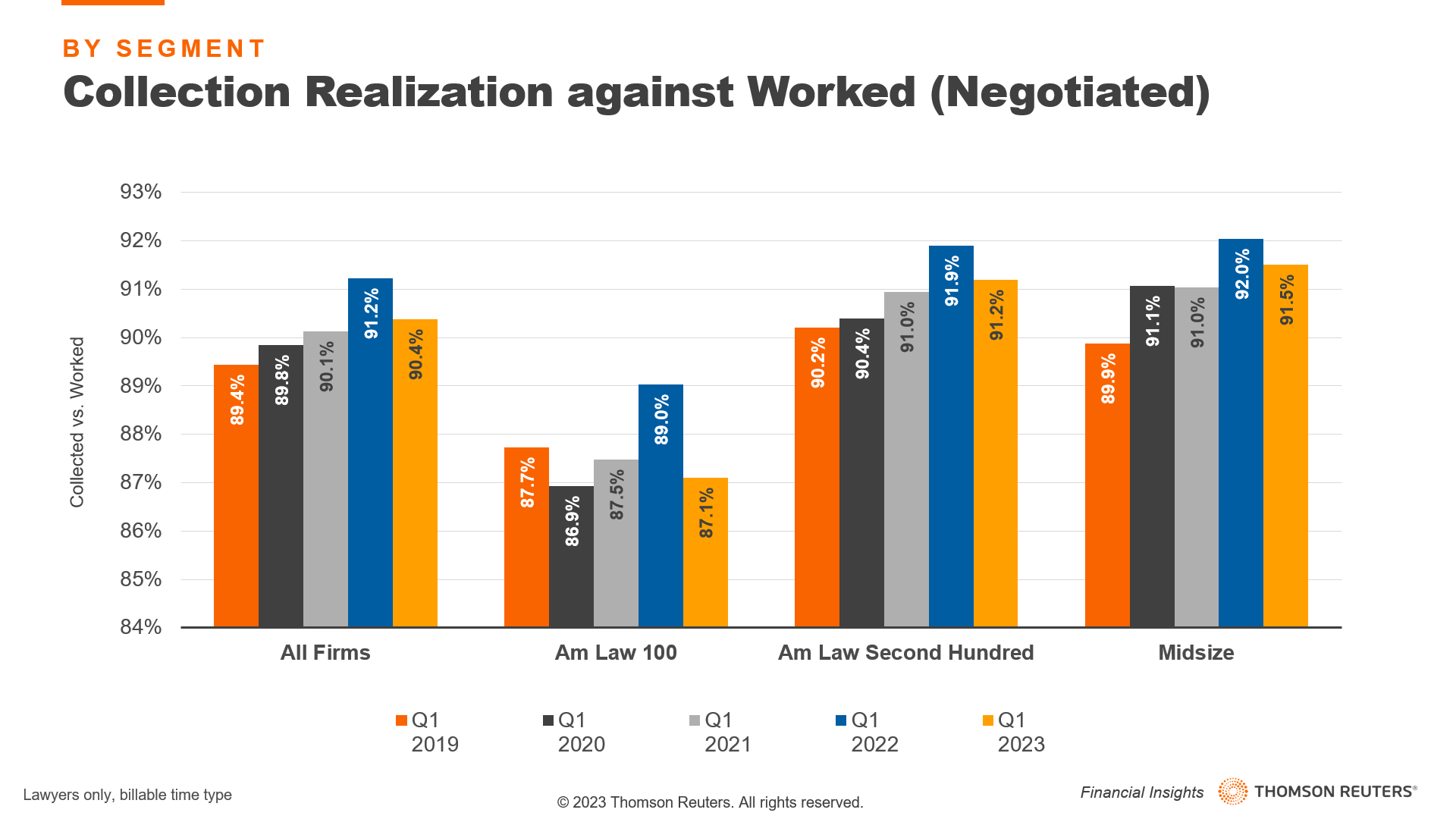

Sir Isaac Newton famously stated that for every action, there is an equal and opposite reaction. Fortunately for the legal industry, this law of physics does not apply here. While it is true that firms’ rate hikes caused collected realization to dip below the mark set at the end of last year (in Q4 collected realization for the average firm was 91.0%), this is a typical seasonal trend and is likely to be the worst realization rate of the year as clients adjust to new prices.

However, in contrast to Newton’s third law, the reaction was not equal. In fact, compared to other first quarters, Q1 2023 resulted in one of the best realization figures in recent years. There is, almost expectedly, one exception to this trend. Am Law 100 firms, which have a transactional-focused practice mix and often serve more cost-sensitive clients, pushed their rate growth at an all-time pace and potentially suffered the greatest amount of pushback. The results of the last quarter, however, tell us that the average firm is holding onto a higher percentage of their worked rates than typical first quarter results despite the significant price hikes.

In summary, the financial performance of law firms in the first quarter of 2023 showed significant improvement compared to the previous year, thanks to rate growth which acted as a catalyst for positive change, with all segments posting some of the highest growth rates seen in recent years.

Despite the external challenges and high expenses that many law firms continue to face, not only were firms able to navigate the situation, they were also able to retain a greater percentage of their worked rates than before. As we move forward, it will be interesting to see if firms can sustain this aggressive approach and continue to reap the rewards.