In 2018, productivity was a boon for many law firms; yet that quickly reversed in 2019 — not because legal demand changed, but because lawyer growth did

The law firm industry has grown demand consistently over the past two years, with back-to-back years of 1% growth. Indeed, the most recent fourth quarter was similar, posting a growth on average of 1.1%. Further, worked rates accelerated throughout 2019, peaking at an average of 4.0% growth in the fourth quarter, and pulling the full year’s worked rate growth up to 3.8%.

Yet, as we discussed in our last analysis, there have been factors that have negatively impacted the Thomson Reuters Peer Monitor Economic Index (PMI), which recently fell three points to 53.

These factors, primarily rising overhead and direct expense growth, have created an environment of smaller margins and dampened profits. Another aspect to the PMI, however, is productivity. In 2018, productivity was a boon for law firms; yet that quickly reversed in 2019 — not because demand changed, but because lawyer growth hit 2.0% in 2019, compared to 0.8% growth in 2018.

To find out more about what factors are influencing PMI, you can download a copy of the Q4 2019 PMI report here.

The growth in the average number of lawyers per firm has contributed negatively in all three factors — higher overhead costs, rising direct expense, and falling productivity — previously discussed in our reports. Direct expenses grow because a larger lawyer base results in rising costs; overhead expenses, which a factor to a lesser degree, are impacted because more infrastructure around a growing lawyer base is necessary; and productivity, of course, is a measure of the amount of work divided by the people doing the work — and currently, the denominator is outpacing the numerator.

As a result, we see this decline in our PMI, even against solid demand and positive worked rate data. However, digging further, what are the practices that drive this accelerating lawyer growth and it’s relative standing with demand?

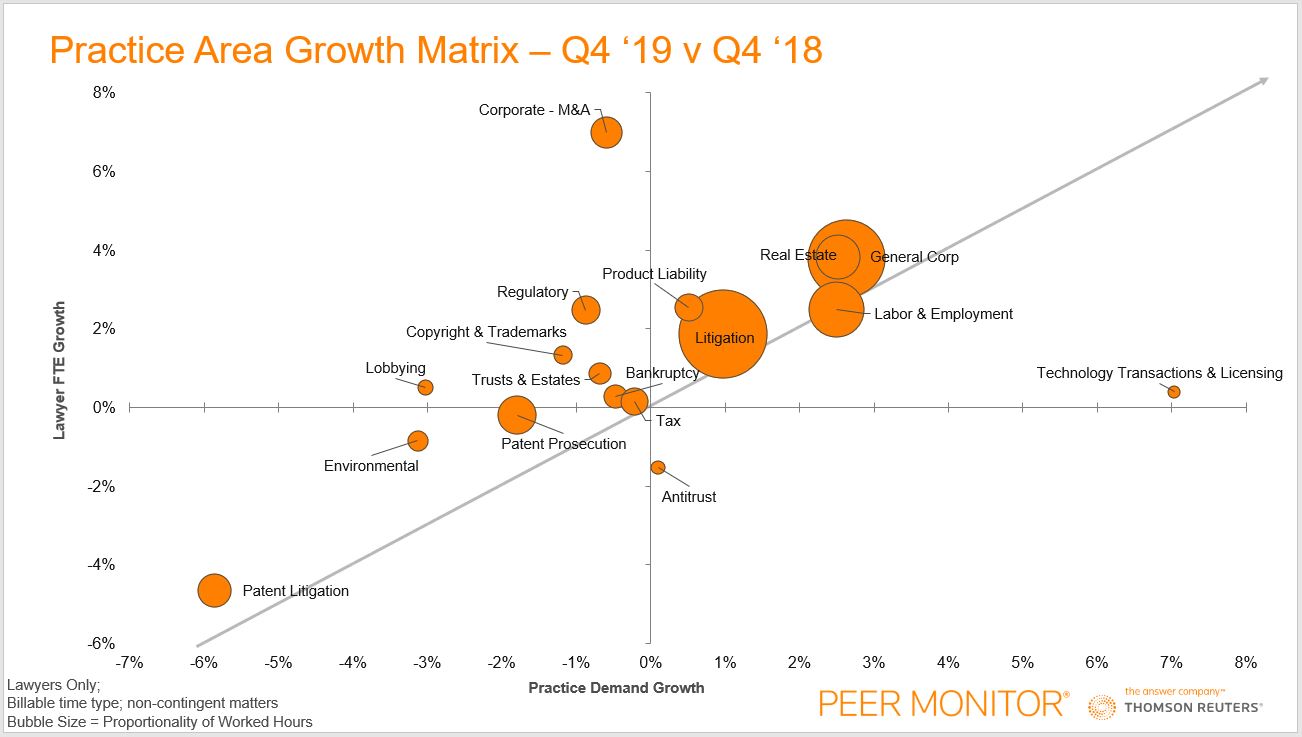

Looking at the relationship between demand growth and headcount growth for Q4 2019 in specific legal practices allows us to look at the overall productivity picture with more clarity. Practices in the top right quadrant represent practices those that have both positive demand and headcount growth, like Real Estate, for example. Whereas practices in the bottom left quadrant represent those that have contracted in both headcount and demand, like Patent Litigation.

Each practice’s “bubble” represents its proportionality of worked hours in 2019, which gives us a better context to see just how influential each practice is. For example, Litigation has our largest proportion of worked hours at 28%, making it our largest bubble; in Q4, however, Litigation saw demand grow by 1.0% and experienced lawyer growth of 1.9%, eerily similar to our overall 2019 numbers.

Further, practices above the gray line in the graph represent areas with decreasing productivity as a result of full-time equivalent (FTE) growth that is outpacing demand growth. For example, you can see this most easily with Corporate M&A work, which is showing a 0.6% contraction in demand against a 7% jump in headcount on average during Q4.

Inversely, practices that fall below the gray line are practices that have higher levels of demand growth than headcount growth, which results in productivity growth. Not only did very few practices fall into this category, those that did were some of the smallest practice areas, greatly mitigating their impact on the market.

With 15 of our 17 practices falling above the productivity line, this data highlights how widespread these productivity losses have been — and how they are not relegated to one or two major practices. The basket of smaller practices, like Lobbying or Regulatory, are seeing contraction in demand, yet headcounts are rising, making these areas some of our biggest losers in terms of productivity.

Does this mean that law firms see promise in these practices for the future and are preparing for the boom? Or is this market-wide shift an attempt to strike a better work-life balance that their workforce is pushing for?

It may be too soon to be definitive, but this dynamic is worth observing in 2020.