Law firms have discovered that they are not immune to the effects of inflation, but a deeper dive into the numbers shows that all inflation is not necessarily equal

The expensive battle for talent in which law firms engaged throughout 2021 now appears to have branched into steadily rising costs across a variety of expense types beyond talent. As reported in the recently published Q2 2023 Law Firm Financial Index (LFFI), overhead expenses for the average law firm grew 7.9% over Q2 2022 on a 12-month rolling average, on top of the double-digit growth in the year before.

Law firms are not alone in experiencing rising costs; inflation has been a general problem for the global economy for the last few years. It’s perfectly reasonable that law firm leadership may have been caught flatfooted by the impact of inflation — many economists were caught off guard as well. Strong central banks and their ability to target inflation, combined with the price-competition of globalization, meant that inflation was supposed to remain a problem only for developing countries or those which strayed from the path of economic orthodoxy. With inflation ticking up since 2021 globally, however, law firms — like most other professional services firms — have had to deal with a drumbeat of rising expenses that have hammered profits.

And while it’s one thing to say that inflation caused firm profits to drop, it’s another to understand its actual impact and how firms can counter it.

Inflation and real rates

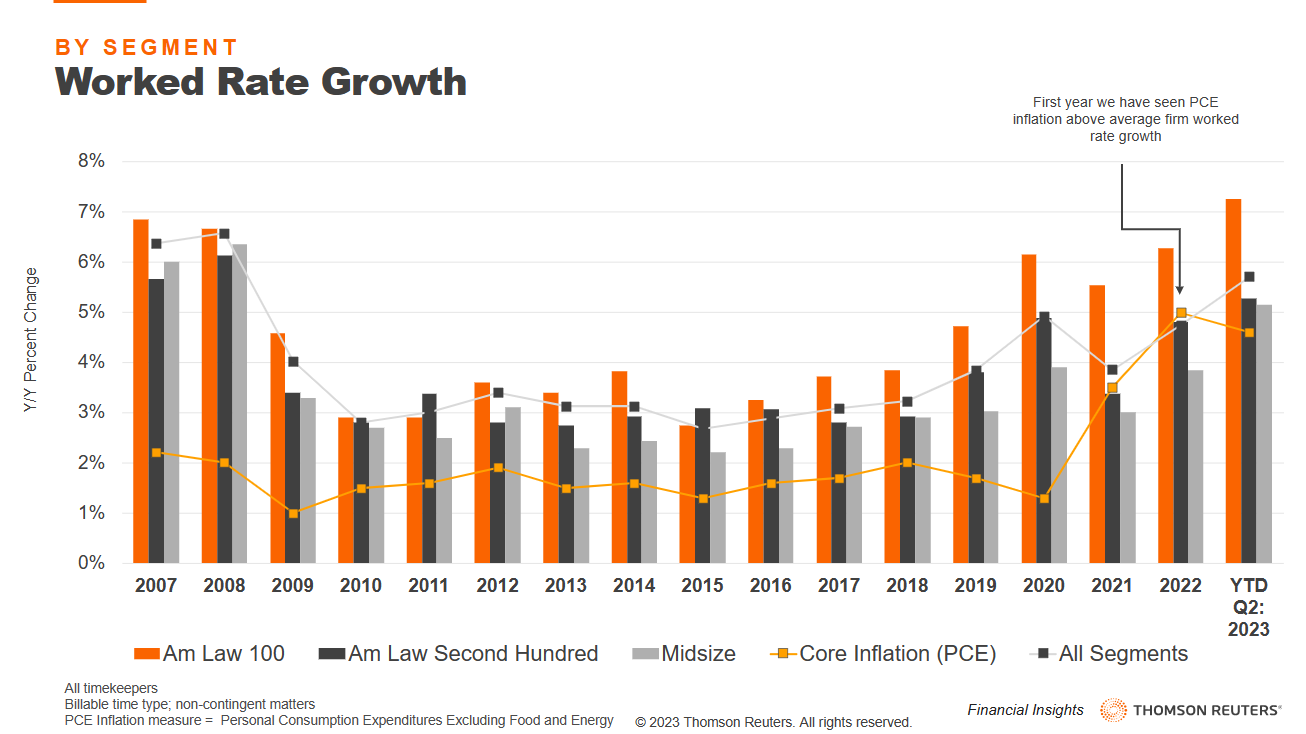

Most of the revenue growth for law firms based in the United States comes not from expanding the number of hours firm lawyers work (demand), but rather by firms’ unique ability to regularly push rate increases. The problem with inflation is that these rate increases aren’t as beneficial as they otherwise would be. Put another way, if your rates rise by 10% but all of your expenses go up by 15%, you’re still falling behind. So, if the general rise of firm expenses exceeds firms’ rate increases, then their real rate growth is actually negative, and they’ve fallen behind.

Charting inflation versus worked rates (or agreed-upon rates) is thus an easy way to measure the potential impact of inflation on rate performance, as the gap between inflation and rates signifies the real rate growth firms experience. Historically, real worked rate growth has been about 2%, but the resurgence of inflation over the last few years has resulted in worked rate growth only slightly hovering above core inflation in 2021 and actually falling behind in 2022. (Note: For these purposes, we use the PCE Core inflation measure [Personal Consumption Expenditures Excluding Food and Energy] both because it is the standard inflation measurement of the Federal Reserve and because we believe it is the most reliable indicator of the rate of inflation experienced by law firms, the reasoning for which will be expanded upon shortly.)

Thus, the average firm experienced negative real worked rate growth, or a contraction in 2022.

Inflation doesn’t necessarily appear on the revenue line in firms’ ledgers, however. Rather, it affects the expense section. The total expense per lawyer (full-time equivalent or FTE) growth of law firms in Q2 2023 showed 5.0% growth and closely tracked the 4.6% inflation experienced by the broader economy in Q2 2023. However, this is only a surface-level viewpoint of how rates and expenses interact — to get a true understanding of how inflation impacts law firms’ expenses, you have to do more digging.

Headline inflation and return-to-office

One of the most common ways of cutting apart inflation is looking at headline inflation versus core inflation. Headline inflation refers to the total inflation measured, while core inflation excludes food and energy prices, which are often notoriously volatile, obscuring the movements of more stable elements. These prices are usually split out to allow core inflation to provide a better idea of the underlying stickier inflation number.

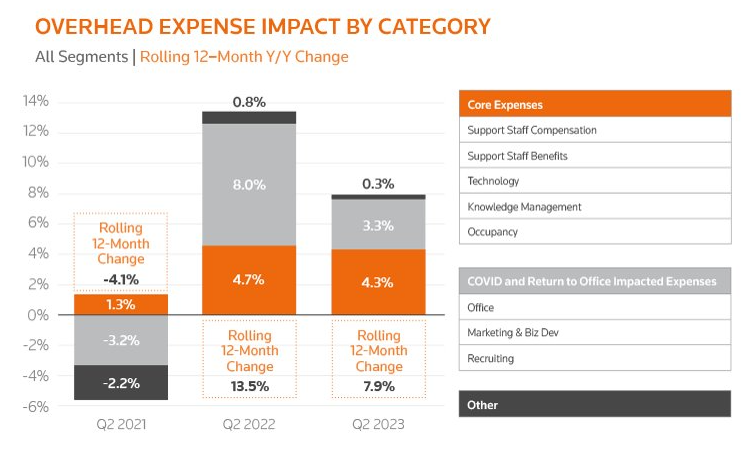

To create a similar comparison, the Q2 LFFI report broke down the percentage-point impact of different expense categories on overhead expense growth, which are those expenses not related to the direct compensation of lawyers. The analysis found that pandemic-related and return-to-office-impacted expenses displayed similarly volatile behavior to food and energy prices, causing much of the expense instability that law firms experienced over the last three years.

In 2021, firms’ bottom lines benefitted greatly from work-from-home savings as expenses contracted compared to the previous year. In Q2 2022 however, the push to bring lawyers back to the office resulted in impacted expenses contributing 8 percentage points to the average firm’s 13.5% rise in overhead expenses. Twelve months later this category cooled rapidly, dropping down to contribute only 3.3 percentage points to firms’ overall 7.9% growth in overhead expenses. The key takeaway here is that this volatile group of expenses, while prone to rapid rises, is also able to rapidly cool.

And this is where core expenses come in. Representing categories of expenses that are more central to the operation of law firms, such as technology and support staff compensation, core expenses have proven much more difficult to tamp down. Even in Q2 2021, core overhead expenses had risen enough to dampen some work-from-home savings. The next year, they had increased by 4.7% (notably not far off from the PCE Core inflation rate of 5.0% during 2022). This category of expenses is also the most challenging to firms at the current point, as this category has become the source of the bulk of operating cost growth, contributing 4.3 percentage points to the average firm’s 7.9% overhead expense growth.

What can law firms do in response?

Law firms in this situation face the same issue as central banks when it comes to inflation. Headline inflation has dramatically cooled since its heights, but the more difficult to control core inflation continues to be an impediment as it maintains steady growth over the previous year.

While firms cannot control interest rates, they have proven themselves able to increase their agreed-upon rates. Firms will need to take measures to ensure that real rate growth remains robust for the next few years. Whether this comes from more aggressive negotiations (using their own expense growth as leverage) or by using emerging technology to increase the value-per-hour of their services, firms will need to keep up the momentum.

At the same time, the challenges presented by return-to-the-office mandates may simply not be worth the risks. Reports of mandatory return-to-the-office regret are rampant across multiple industries and the ever-greater expenses required to bring employees back to the office don’t seem to be paying any premiums in productivity. Backing away and finding a more cost-effective way to bring people back to the office (or maintain a hybrid schedule) may allow the volatility of these expense categories to work in firms’ favor.

Ultimately, law firms have discovered that inflation is not picky, and it is just as willing to increase the operating expenses of a firm as it is to impact the price of a used car or a bag of groceries.