Transactional demand in the legal sphere may depend strongly on the future direction of interest rates and whether the U.S. economy will see more inflation

The first half of the fiscal year saw the legal industry continue its recovery from 2022 lows, with the Thomson Reuters Institute Law Firm Financial Index (LFFI) up 6 points to an index score of 50 in the second quarter.

And while much of the industry’s improving health has been the result of strong demand for counter-cyclical work — which has, thus far, been enough to compensate for weakened demand in transactional practice areas — that may be changing. Since the LFFI’s Q2 release, Thomson Reuters Financial Insights’ data has started to show signs of counter-cyclical demand growth potentially cresting, adding fuel to the already burning question of “When will transactional demand return?”

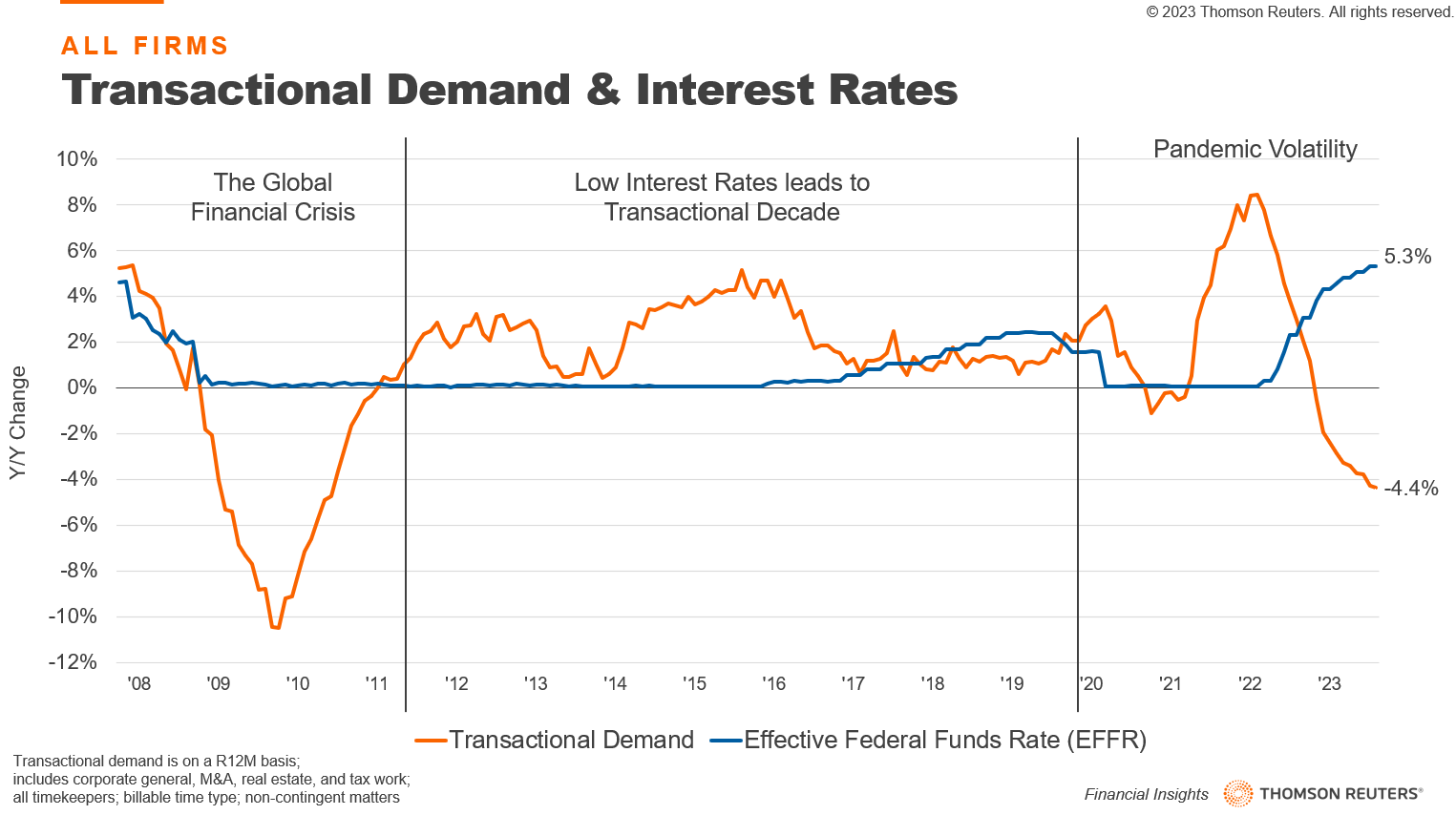

Through the first two quarters of this year, demand growth for transactional work has fallen to levels not seen since the end of the Global Financial Crisis. This is a far cry from the last decade, in which low, almost 0% interest rates were used by the Federal Reserve to stimulate economic growth and spur a recovery. This added liquidity helped corporations finance deals, and over the course of a decade we saw transactional demand drive law firm performance. Central banks continued to keep interest rates low during the COVID-19 pandemic even when governments around the world pumped historic stimulus packages into their economies.

These factors, along with others, helped accelerate transactional demand growth to the greatest pace in our data’s history, and firms reaped the rewards in 2021. These low-interest rates also contributed to what was then called transitory-inflation, which, when the Fed began realizing was not so transitory, led to a series of the fastest rate hikes in U.S. history. Over the course of the past 18 months Fed officials increased their target interest rates from nearly 0% to a band of 5.25% – 5.5%, while demand for transactional work was pushed down from over 8% growth to a contraction of more than 4% on a rolling 12-month basis.

This brings us back to the present day, in which tightened balance sheets, increased credit risk, and a still uncertain economic environment have cooled much of the current appetite for deal-making. Law firms, which in 2022 saw 37% of their billable hours come from clients’ eagerness for transactional work, are suffering. Lower demand has translated into lower productivity, which itself has resulted in some associates being let go, and partners enduring lower profits per equity partner as they wait for a return of transactional demand; a return which increasingly hinges on a return of lower interest rates.

This week, the Federal Open Market Committee (FOMC) announced that their target rate would hold steady at a band of 5.25% to 5.5%. Most of this pause was already priced into the market with a probability of 97% and the end of last week that the Fed would stay at the target rate set in July, according to the CME FedWatch Tool (which tracks Fed Funds’ futures prices). Moving forward, market expectations are more divided. Probabilities of a rate increase in November and December are currently at 28% and 46% respectively, with the market forecasting rate decreases to potentially come in no earlier than January or March 2024.

These expectations largely depend on how the Fed interprets economic indicators like the inflation index, jobs reports, and GDP growth. Last week headline inflation ticked up to 3.7% in August from 3.2% in July as consumers faced rising energy and food prices, while core CPI rose a lesser but still concerning 0.3 percentage points to 4.3% in August, compared to July. The jobs report from August showed slower hiring and posted unemployment at 3.8%, up from 3.5% in July but still well below historic norms. Current GDP forecasts also stand well above the Fed’s long-run potential growth rate of around 2%, with the Atlanta Fed’s GDPNow model estimating 4.9% growth in Q3.

However, it is the muddiness and crosscurrents of these indicators that cloud the Fed’s interest rate path and make it difficult for law firms to plan ahead for a potential resurgence of transactional demand. If the Fed interprets an uptick in unemployment as signs of a cooling economy, that may reinforce its current stance of holding rates steady and eventually lowering them. However, if inflation continues to ascend, or remain elevated, and the economy continues to run hot, the Fed may very well raise rates going into 2024 or hold the current levels for longer, further stressing transactional demand.

Personal Consumer Expenditures (PCE) inflation (the Feds preferred gage of inflation) has come down from above 5% last year, but many fear that the Feds’ 2% core inflation target will be harder to reach as elevated housing and rent costs and increased wages place upward pressure on prices.

All of this leaves the Fed with a difficult decision on how much harder and longer to squeeze monetary policy. During yesterday’s FOMC meeting, Fed chair Jerome Powell said that “the process of getting inflation sustainably down to 2% has a long way to go”, and that “stronger economic activity means we have to do more with rates.” He also added that economic lags in response to monetary tightening would be another reason for the Fed to proceed carefully, signaling to the market and legal industry that this period of uncertain transactional movement is likely to remain for the time being.

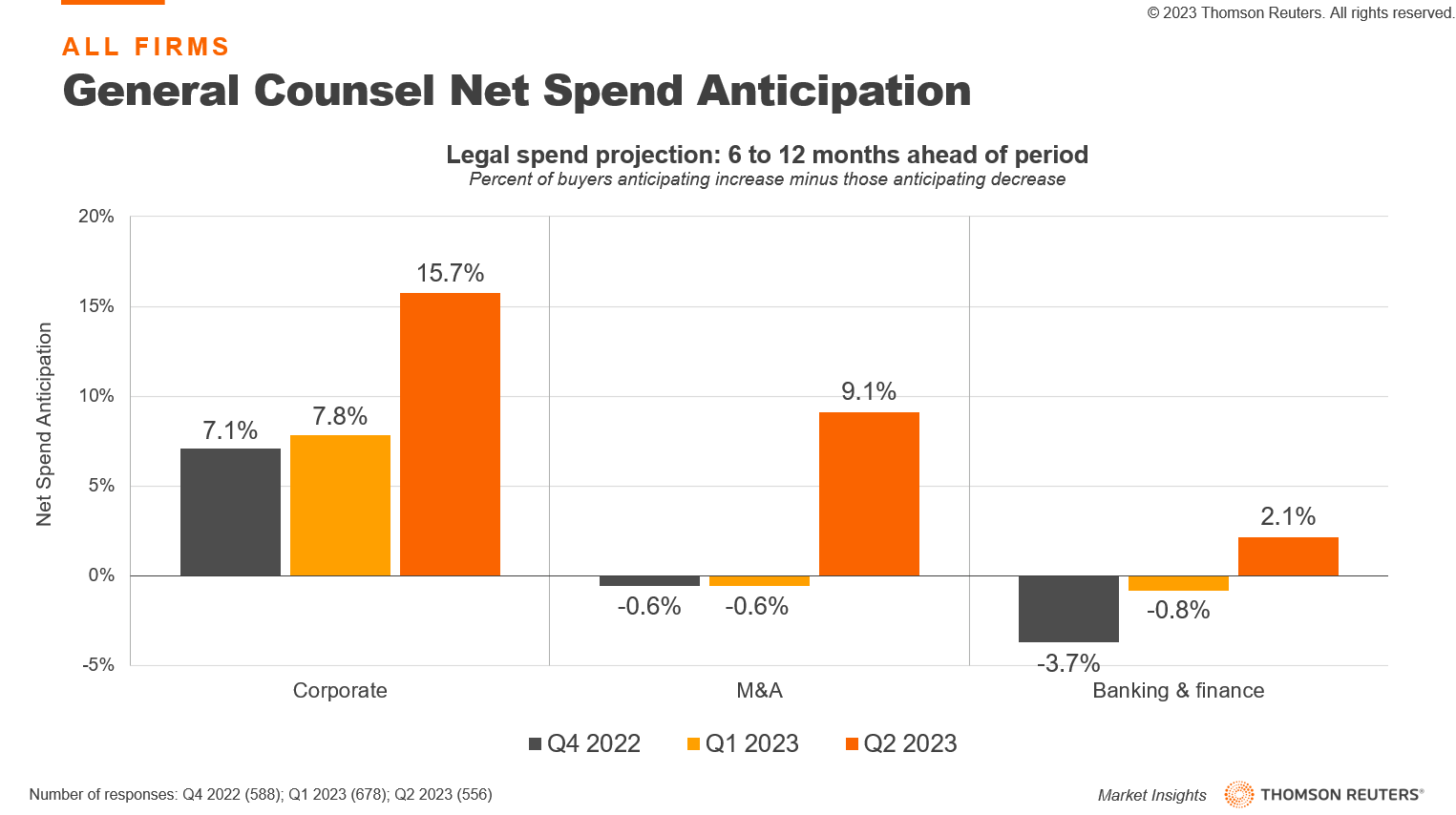

Despite the uncertainty in interest rates, it does appear that there is growing optimism from corporate General Counsel (GCs) in terms of increased transactional spend. When GCs were asked if they anticipate an increase or decrease in legal spend in specific practices in the next 6 to 12 months, the net difference between the respondents that say they expect an increase minus those that expect a decrease was, for example, 9.1 percentage points in regard to anticipated M&A spending, according to Thomson Reuters Market Insights data (This difference is referred to as net spend anticipation).

Over the course of 2023 it’s easy to see that there has been a notably positive swing, especially in M&A and corporate work. The data indicates that buyers could be anticipating their C-suite and boards will eye more deal-making, under the assumption that interest rates will start easing sometime during 2024 and that the declining demand for these practice areas may have bottomed out.

As we navigate the intricate landscape of the legal industry in 2023, however, it is evident that transactional demand is facing unprecedented challenges, reminiscent of the post-Global Financial Crisis era. The Federal Reserve’s decision to maintain interest rates at the current level has provided a momentary respite from drastic changes, yet the path forward remains shrouded in uncertainty, with economic indicators pulling in conflicting directions.

However, there are glimmers of optimism for transactional practice areas; and as we move forward, the legal industry remains poised, waiting for clearer signals from the Fed and the broader economic landscape.